“Leadership is the capacity to translate vision into reality.”

-Warren Bennis

We held our inaugural Hedgeye Cares Charity Golf Challenge at Great River Golf Club in Milford, CT yesterday. The group of my colleagues that banded together to form the Hedgeye Cares committee did an outstanding job translating a vision into a reality.

Like most charity events, it wouldn’t have been a success without the support of myriad sponsors. On the corporate side, we were pleased to get support from The Lincoln Motor Company, Salesforce.com, Bloomberg, D.B. Root, MBIA, Better ITS, the Arizona Coyotes, and Firefly Space Systems just to name a few. In addition, many individuals like you were kind enough to lend a helping hand by either buying a foursome or providing items for the silent auction.

Aside from being a very enjoyable day, we also raised close to $100,000 for Bridgeport Caribe Youth Leaders, which is an all-volunteer program based in Bridgeport, CT that provides “children with diverse educational, sports and community awareness programs that foster physical, intellectual and social development, while instilling pride and helping them build character and self-esteem, so that they can reach their full potential and value their role in society.”

Certainly a group more than worthy of our support. Again, we thank you.

Back to the Global Macro Grind...

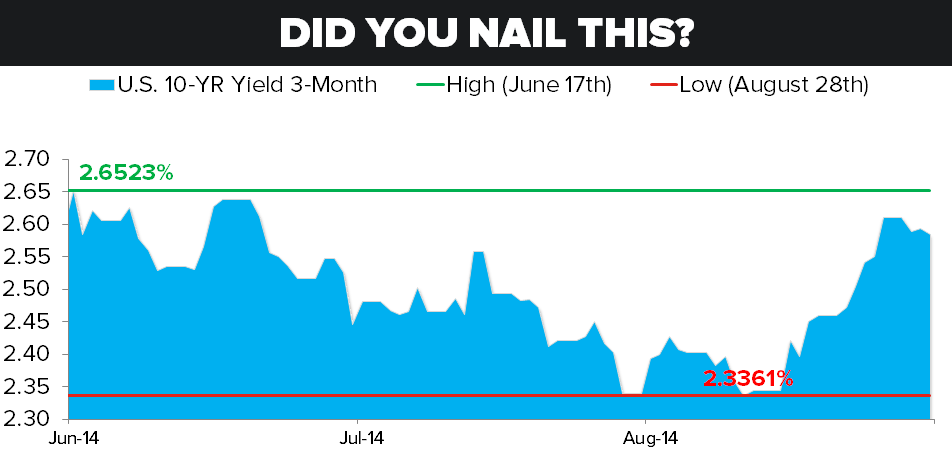

Even as many of my Hedgeye colleagues were away from their screens yesterday, the global macro news flow continued. The most relevant global market over the next 24 hours is of course likely to be the Treasury market with the Federal Reserve policy meeting occurring later today. Regardless of what the Fed says today, it is likely that very few investors have “nailed” the last month of interest rate moves, except in hindsight.

As shown in the Chart of the Day below, on August 15th, the 10-year yield hit a 2.30% low. Within a month, by September 15th, the 10-year yield had tacked on 30 basis points and reached basically a three month high. This morning the 10-year yield is trading off the recent highs from a couple of days ago, albeit only marginally. Even if you didn’t nail the move, or did so in hindsight, the fact remains having a view on rates, and thus the U.S. dollar, is critical in global macro positioning.

So, what is the Fed going to say and how are we positioned?

Despite the lack of a crystal ball, we are sticking with our house view that Fed will be more dovish than expected. With reported inflation relatively benign, the housing sector seeing some cracks (arguably a lot!), and the most recent employment data points softer than expected, there seems to be little incentive for the Fed to ramp up the hawkish rhetoric.

According to his Wall Street Journal podcast from yesterday, the mighty Fed visionary Jon Hilsenrath appears to agree with us. As he noted:

“Given the economic backdrop, they don’t want to send a signal right now that rate increases are imminent.”

Indeed Mr. Hilsenreth, indeed.

So, interestingly, as we head into the main Fed event, the 10-year yield didn’t even make it into the top three things that Keith sends out to subscribers in his “Direct from KM” email every morning at 6:00am, which were as follows (if you aren’t on "Direct" from KM please email to get details on being added) :

- ASIA – w/ the Russell 2000 -1.2% YTD, it’s been a lot easier for small/mid cap growth investors to stay with long China, India, and Indonesia – all up again overnight to +12.5%, +27.6%, and +23.5% YTD, respectively – that’s where the real perf is and also why you’ll see a higher “International Equities” allocation in our asset allocation model than USA

- USD – one of the biggest overbought exhaustion signals in 15 years remains, but you saw what a downtick in USD can do yesterday; huge 1-day move in both Oil and Energy (XLE) stocks – I still think the Fed gets easier throughout Q3/Q4 as the rate of change in US economic growth data slows – consensus is hawkish

- UTILITIES – the Down Dollar, Down Rates move yesterday paid the slow-growth #YieldChasers – that was the 1st SPX Sector we signaled buy on alongside the SPX oversold signal at 1977; XLU +1.2% on the day yesterday to +13.1% YTD – we’ve stayed with that all year and I’m not changing my mind on it into the Fed statement either

Speaking of vision, it seems the Scottish vision of independence will be tested today. According to the most recent three polls, the "No" for Independence voters are maintaining a narrow lead of some four points.

As we have often written, polls in the aggregate matter and in the aggregate the polls continue to imply that the No votes will prevail. Interestingly, as well, online betting site Betfair has already started paying out No votes as they consider the No majority win a foregone conclusion. That all said, until the mighty Jon Hilsenreth opines nothing is truly a foregone conclusion!

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.40-2.62%

SPX 1

Shanghai Comp 2

VIX 11.34-14.09

Pound 1.61-1.64

WTI Oil 91.37-95.12

Gold 1

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research