This note was originally published at 8am on September 02, 2014 for Hedgeye subscribers.

“There is an ongoing conversation among the different factions in your brain…”

-Dr. David Eagleman

That’s an important quote from neuroscientist , David Eagleman, that was cited by Brene Brown in a new #behavioral book I finished this long weekend called Daring Greatly. If you’re looking for some introspection into both your investment process and life, this one will make you think.

Thinking is good. So is reading/writing. These basic brain exercises help you debate yourself in that ongoing conversation “among the different factions in your brain, each competing to control the single output channel of your behavior.” (Daring Greatly, pg 76)

Eagleman calls your brain a “team of rivals” within the two-party system of “reason and emotion.” Brown contextualizes the back and forth conversations you have with yourself with feelings like vulnerability and shame. These are perfect things to read about right before you take your kids to a pancake breakfast!

Back to the Global Macro Grind …

The market is at its 2014 highs, baby! How does that make you feel? Oh, and what “market” are you thinking about when you read the word market? The long end of the US bond market has had a much better year than the US stock market (TLT = +19%, with dividends).

While it didn’t shame me to see the broad measure of US growth expectations (Russell 2000) rise +1.2% on no volume last week, it certainly didn’t please me to see consensus chasing a misplaced expectation that it’s had all year (for US GDP to be +3-4% and bonds to fall).

It evidently didn’t shame the European growth bulls to beg for a new round of Quantitative Pleasing either. If being long European stocks was always based on Europe slowing to the point that it needed moarrr money printing, my hat is off to whoever nailed that.

For equities-only fans, in addition to European stocks (Europe’s Stoxx 600) and the Russell 2000 being +1.2% last week, here’s what else happened:

- US Industrial Stocks (XLI) were down -0.2% to +3.4% YTD

- Emerging Markets (MSCI) were down -1.4% to -1.0% YTD

- US Utilities (XLU) were +2.0% to +14%YTD

- Russian stocks were -5.5% to -17.5% YTD

- Argentine stocks were +7% to +82.1% YTD

In other words:

- Slow-growth #YieldChasing (long XLU vs XLI) remains alive and well as a US Equity Sector strategy

- Emerging Market equities still do not like a stronger Dollar

- The more screwed up your country gets, the higher the stock market goes?

Oh, yeah. Definitely.

Doesn’t this all make you feel good? Like this time is different or something? With Japanese, European, and American central planning committees going all in on Policies To Inflate, even that crazy critter called commodity #InflationAccelerating came back online last week:

- CRB Commodities Index +1.4% on the week to +4.5% YTD

- Coffee prices up another +7.4% on the week to +67.5% YTD

- Cattle prices up another +3.5% on the week to +28.0% YTD

I know. Eat a hot dog or something. Steak is overrated. Ask the government people about the “substitution effect” on your barbeques, eh! (PS: if you bought the sausage instead of the ribeye, hog prices were up another +5.7% last week too = +17.2% YTD).

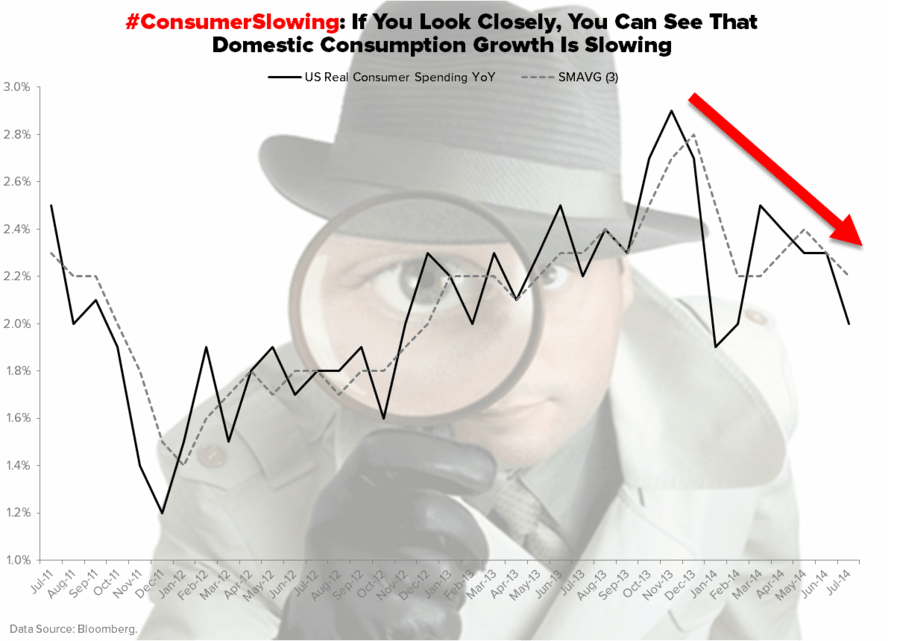

Now the reasoning side of the veggies and water brain couldn’t care less about this stuff. It’s we emotional guys pounding the caffeine and burgers who need to deal with ourselves. Because the US equity consumption growth bulls don’t want to talk about real things, like inflation.

To be clear, even the CRB Index is beating both the Russell 2000 and Euro Stoxx 600 by +360 basis points for 2014 YTD (both the Russell and Euro Stoxx 600 moved back into the black to +0.9% for 2014 last week – raging bull in emotions there!).

In other news, what real cost of living ripping to all-time highs in the US does is slows real growth – so last week you also saw:

- Goldman cut its Q3 US Growth estimates for the 2nd time in 2 months

- US 10yr Treasury Yield drop another 6 basis points on the week to 2.34%

- US Treasury Yield Spread (10yr minus 2yr) continue to compress, -79 basis points YTD

Net of all my own performance issues, emotions, and reasoning, this is where I stand on September 2nd:

- Wanting to buy more long-dated bonds (High-grade Corporates or Treasuries) on dips

- Wanting to be longer of our two favorite Emerging Markets (China and India) on pullbacks

- Wanting to avoid anything US growth equity bubble like the bubonic plague

Plague? Yep. I really do not like to buy the all-time-bubble highs in anything. But that’s just me. For better or worse (we’ll see), these factions of 1999 and 2007 in my brain just won’t go away.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.33-2.43%

SPX 1980-2009

RUT 1151-1179

Shanghai Comp 2199-2278

EUR/USD 1.31-1.33

Pound 1.65-1.67

Gold 1271-1299

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer