“A government institution that is not dominated by politics is as likely as a barking cat.”

-Milton Friedman

To be balanced, I like to fact check what high profile economists have stated as fact. And while Friedman’s statement was more of a probability-based one, there’s a YouTube video (click here to watch) that shows a cat that was (allegedly) barking, but resumed meowing. There are 19,624,067 views of this thing. #Riveting

There was an article in the Wall Street Journal yesterday that suggested that the Mother of All Doves (Janet Yellen) attacks like a hawk. While everything in the Currency War is relative (when Draghi devalued the EUR/USD, she looked relatively hawkish), in the face of slowing US and European economies, Yellen raising rates is as likely as my dog purring.

Oh, and I don’t have a dog.

Back to the Global Macro Grind…

So what do you do if Janet reverts to meowing like a dove?

1. Buy the Long Bond (TLT)

2. Buy stocks that look like bonds (XLU)

3. Buy Gold (GLD)

That’s what Mr. Market told you to do yesterday. That’s what he told you to do in 2011 (when Europe slowed last time) too. Here are your timestamps in what was a big time diverging US equity tape yesterday:

1. Utilities (XLU) up +0.3%

2. US IPO Bubble (IPO) -2.1%

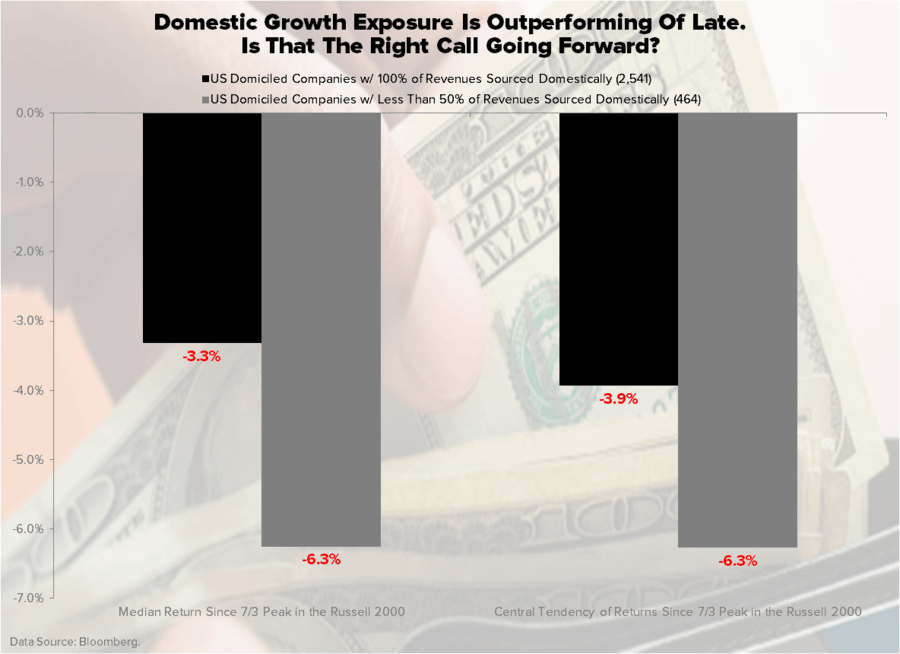

3. Russell 2000 (IWM) -1.1%

To be fair, away from the 40% of IPOs that have blown up already (-20% from peak in the last 12 months), 60% of these puppies have been barking alpha to the upside. If you’ve played lucky on that front (or are just a supreme stock picker), congrats!

The Nasdaq got tagged for a -1.1% drop yesterday too. The beta-chasing there (and in small/mid cap stocks) has been epic this year, if only because you could have been neutered (dogs don’t like that either) on the long side 40-50% of the time.

Pardon? Mucker, I thought the “market doesn’t go down.” If you call the SP500 (+7% YTD) or the long end of the Bond market (TLT is +12% YTD), the “market”, I guess that is accurate. Unfortunately, most of us don’t get paid to buy the index.

Here are some more US stock market #bubble stats for you:

1. 47% of stocks in the Nasdaq are crashing from their 12-month peak

2. 41% of stocks in the Russell 2000 are crashing from their 12-month peak

3. 6% of stocks in the SP500 are crashing from their 12 month-peak

*note: crash = a decline in price of -20% or more

That’s why I am overly comfortable calling the momentum and small cap side of the US stock market a #bubble these days – it’s easier to do when they are already popping!

It’s also why this year you will see who can really pick stocks. There’s a huge difference between a PM who is up +10-15% YTD with 5-10 positions that have been really right than ones who are -10% to +5%, with 50-100 positions that are trying to not blow up.

As all of you who run money and/or manage your own know, the key to compounding your net wealth is not losing money. Warren Buffett called it rule #1. Believe him. He’ll do anything these days to make his preferred investment a guaranteed win.

In other IPO #bubble news (in both market cap and names that have come public, we are beyond 1 now):

1. The Ali-bubble (BABA) has raised the top-end of its IPO price range to $68

2. Dave and Buster’s is trying to come back from the dead with a $100M IPO

3. Freshpet is going to try to get $100M of other people’s money through GS and Credit Suisse

Don’t get me wrong. If you are long all of this stuff at a lower-cost basis (pre-IPO) before the Old Wall jams it into the indexes, you are crushing it. That is capitalism and I am a big fan of your being early.

But as I watch this damn Freshpet website shuffle between slides this morning (“Healthy meals, so tasty, dogs and cats might just beg for more!” – is that a CS line for eat this IPO and I’ll give you more BABA?), I can’t say I support coming to this IPO bubble late.

While I am sure there’s another dog you can find purring somewhere on YouTube, I’m not in the risk management business of telling you that everything I learned during the 2000 and 2007 stock market bubbles is different this time.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.34-2.62%

SPX 1

RUT 1144-1161

VIX 12.86-14.69

EUR/USD 1.28-1.30

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer