Investment Ideas

The table below lists our Investment Ideas as well as our Bench -- a list of potential ideas we are watching closely. We intend to update this table regularly and will provide detail on any material changes.

Notable Callouts

- We removed short BNNY from our Investment Ideas list after the GIS bid.

- Our short call on SBUX was featured in Barron's this weekend in a column titled "The Problem With Starbucks."

- We are hosting a Best Idea call this Thursday, September 18, 2014 at 11am EST to run through our short thesis on SBUX and field questions.

Recent Notes

09/08/14 Monday Mashup: BLMN, PLKI and More

09/11/14 New Best Idea: Short SBUX

Events This Week

Monday, September 15th

- YUM Investor & Analyst Conference Day 1

Tuesday, September 16th

- YUM Investor & Analyst Conference Day 2

Wednesday, September 17th

- DNKN Investor & Analyst Day

- CBRL earnings call 11:00am EST

Chart of the Day

Coffee prices are up +52.5% YTD and +39.5% YoY.

Recent News Flow

Monday, September 8th

- BAGL appointed Frank G. Paci as President and Chief Executive Officer. Interim CEO Michael Arthur will continue to serve on the company's Board of Directors. Mr. Paci most recently served as President and CEO at McAlister's Deli and has held prior roles at The Pantry, Pizza Hut and Burger King.

- RRGB announced it will open its newest restaurant in New York state (Horseheads, NY) on September 22nd.

Tuesday, September 9th

- DIN introduced its new "Waffullicious Waffles" which will be available for a limited time.

- MCD reported disappointing August comps as global same-store sales fell -3.7%, led by -4% and -14.3% declines in the U.S. and APMEA regions, respectively.

- BJRI increased its existing unsecured revolving line of credit to $150 million from $75 million and announced the opening of its newest restaurant in Denton, TX.

- KKD announced a greater Maryland and Washington DC area development agreement with Monument Restaurant VII for the development of 20 new Krispy Kreme shops over the next several years.

Wednesday, September 10th

- YUM increased its quarterly dividend by 10.8% to $0.41.

Friday, September 12th

- DRI Starboard released its transformation plan for Darden Restaurants in a 294 page slide deck. If enacted, the activist believes its plan could unlock $19-38/sh in value. This excludes the potential value that could be unlocked through an Olive Garden turnaround.

- SBUX 6.2 million share block trade was priced at $75.15 through BoA.

- LOCO celebrated the grand opening of its newest restaurant in Sacramento, CA.

Sector Performance

The SPX (-1.1%) outperformed the XLY (-1.3%) last week. In aggregate, casual dining and quick service stocks outperformed the SPX.

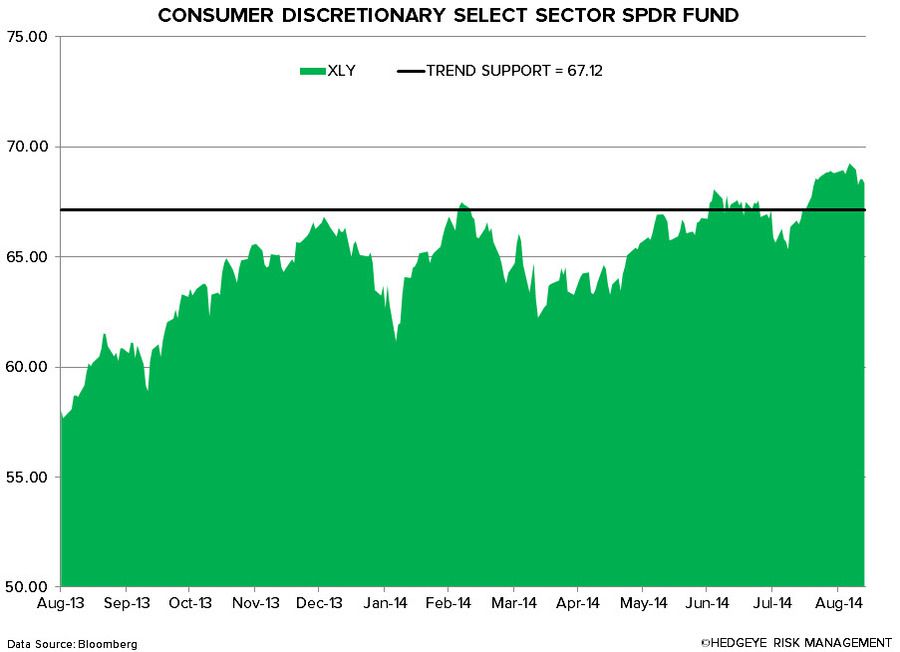

XLY Quantitative Setup

From a quantitative perspective, the sector remains bullish on an intermediate-term TREND duration.

Casual Dining Restaurants

Quick Service Restaurants

Howard Penney

Managing Director

Fred Masotta

Analyst