A big currency move meeting a shift in forward-looking supply/demand expectations continue to put downward pressure on oil prices.

From a quantitative perspective, our intermediate-term TREND set-ups in Oil vs. the USD have reversed from their 1H14 TRENDS:

USD = BULLISH TREND

BRENT = BEARISH TREND

WTI = BEARISH TREND

Below we outline two major factors contributing to the oil and gas disinflation over the summer with a view on the potential price risk into next week’s FOMC statement….

1. DRAGHI TRUMPS YELLEN: USD MOVES STEADILY OFF 2014 LOWS:

Moving into 2014 we positioned for a slowdown in U.S. growth and acceleration in inflation perpetuating an easier Fed-putting pressure on the dollar.

Through May 6th, 2014:

- USD debauchery: -1.18%

- domestic growth DECELERATION (this view is still FIRMLY intact)

- domestic inflation ACCELERATION

- CRB Commodity Index: +9.7%

- 10-Year yield: -44 bps (-14.4%) against the largest short position in U.S. treasuries we have seen since. See below for an outline of the risk with one-way, leveraged consensus macro positions

Adding to the pressure on the USD was the sustained strength in most Eurozone economies through the first half of the year. Once this relative strength began missing expectations with inflation missing estimates, Draghi moved to talking down the Euro with every opportunity.

On May 6th he hinted at a rate cut and asset purchase program by stating, “There is consensus [among the ECB Committee] about being dissatisfied with the potential path of inflation.”

May 6th also happened to be the YTD high in the EUR/USD: +1%. Since the May 6th highs, the USD has run +5.6%.

The relationship here is self-evident. At two points over the summer, Draghi took deliberate policy steps to devalue the EURO and plant the QE seed (WHICH HE DOES NOT HAVE THE POWER TO IMPLEMENT RIGHT NOW).

While the USD continues its steady move off its 2014 lows, Oil has sold off sharply from the June highs in WTI and BRENT:

WTI:

- -12% from June highs

- -6% YTD

- -2.8% WTD

BRENT:

- -15% From June highs

- -11.7% YTD

- -3.7% WTD

------

Refreshed daily, our real-time view on both Q3 and full year 2014 growth estimates remain meaningfully divergent from consensus (the Fed, sell-side/buy-side macro):

We expect incremental divergence in this view to warrant an easier Fed. With consensus leaning 1) short the Euro, 2) short of treasuries; And 3) longer of U.S. growth (THAN US)…

YTD highs in the negative correlations between gold and oil vs. the USD present the volatility and macro correlation risk Keith outlined in this morning’s Early Look:

The chart above shows the dislocation of correlation risk relative to historical averages which are more or less insignificant.

KM’s EL commentary:

“Again, this is where the Hydra-headed monster of market expectations really matters – it’s called correlation risk:

- When Fed heads use communication tools to talk up rate hikes (like Bernanke just did) USD and rates rise

- When USD and rates are rising, at the same time, commodities, oil, Gold, etc. go down

- The machines (quants) then chase macro correlations, and macro markets get overbought/oversold”

Point three addresses the immediate, real-time risk that can smack you in the face. When those looking to minimize large currency and rate exposure anchor on macro correlations for hedge-sizing considerations one-way, large positions create the execution risk block traders love to hate:

- Anchoring: Tighter the correlation requires a bigger hedge

- Volume: Larger positions create large capitulation risk

- Sentiment: The “Commitments of Traders Report” from the CFTC shows a consensus position that is short the Euro, short long-duration treasuries, and longer (Than US) on U.S. growth.

- Volatility: If a leveraged consensus trade is wrong, the volatility risk is greater in the FX, Gold, and Oil markets as robots and scalpers chase the large trades.

- Risk: What is the probability of price moving to a certain level? We model it higher with this correlation risk. From an immediate-term TRADE duration perspective the bands/levels for identifying overbought/oversold exhaustion signals widen.

2. U.S. SUPPLY FLOOD AND GENERAL GEOPOLITICAL EASE:

- On Tuesday the Energy Information Administration (EIA) increased its expectation for U.S. oil production for the full year 2014 and 2015

- On Wednesday the International Energy Agency (IEA) decreased its estimate for global oil demand for 2015

In The EIA’s monthly release of its “Short-Term Energy Outlook” on Tuesday, the administration raised its estimate of 2015 U.S. Crude Production to 9.53M/BD (highest level in 45 years)

The report included the following data points and revisions:

- Increased full year 2014 U.S. production estimate to 8.53M/BD vs. 7.45M/BD 2013

- Production levels for August reach 8.6M/BD (highest since July 1986)

- Also in the report, the EIA estimates GLOBAL oil supplies will increase by 1.3M/BD in 2015 (U.S. accounting for 91% of the increase)

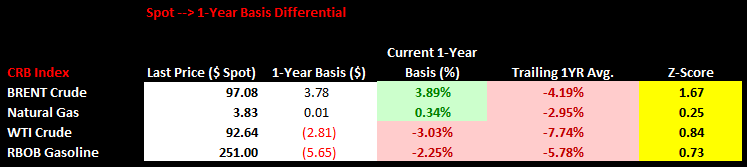

The increase in expected U.S. production can be seen in a widening of the Spot-1YR basis between WTI and BRENT:

This summer’s decline in petroleum prices is finally flowing through to the pump….

The average gallon of gas in the U.S. is $3.433/gallon which is down -6% from Memorial Day. This summer’s decline is the largest since 2008.

Following the EIA’s Tuesday report, the IEA released its downward predictions for global energy demand in 2015:

- Demand to expand +1.2M/BD (+1.3% in aggregate) 2015 vs. August estimate (-165K/BD less) m/m

- Saudi Arabia exported the least in 3-years in August

As a result OPEC has now cut its estimates for the amount of petroleum it needs to produce for the full year 2014 by 200K/BD to 29.2M/BD on average.

The two reports induced selling pressure and volatility to WTI and BRENT markets. The move in BRENT is a great indication on how quickly the bid for volatility can change with a catalyst:

The move was confirmed with heavy VOLUME Tuesday and Wednesday in BRENT-WTI:

- Tuesday: BRENT-WTI +10-25% 1/3/6-month averages

- Wednesday: BRENT +56/34/48% above 1/3/6-month averages

- Wednesday: WTI +18/11/16% above 1/3/6-month averages

Also adding to the pressure is an overall ease in the geopolitical catalysts threatening supply disruptions

IRAQ

The U.S., Canada, and Iraq are expected to experience the largest increases in global oil production over the next five years, so protecting Iraq’s oil reserves remains a priority for production sustainability into the future. OPEC estimates Iraq will peak at 40% of OPEC’s total production in the future, a fourfold increase from ~9% currently. The ISIS advance is undoubtedly a real threat, and our involvement in the conflict is timely. We outlined the ISIS threat to Iraq’s production capacity in a recent note. So far it’s minimal.

Russia/Ukraine (add link to Note):

Energy encompasses 70% of Russia’s annual exports. Russia’s dependency on demand from the rest of Europe as a driver for the rest of Europe is outline in a recent note we published last week:

Why Vladimir Putin is More Judo Master Than Chess Player

As always, please feel free to reach out with any comments or questions. Have a great weekend.

Ben Ryan

Analyst