Tickers: LVS, MGM, MAR

EVENTS

- Sept 15-19: CLSA Investor Forum (MGM, Genting S'pore, WYNN, LVS, SJM, Bloomberry,

- Sept 16: Trump Plaza closes

- Sept 16: FCH investor meetings in Canada

- Sept 17: Massachusetts Gaming Commission: Boston Decision by Wednesday

- Sept 17: PENN at Credit Suisse Small & Mid Cap Conference

- Sept 17-18: Hedgeye Cruise Pricing Survey mid-Sept

- Sept 18: Imperial Capital Global Opportunities Conference

- BYD, PENN, GLPI

- Sept 18: WYN & VAC at MKM Entertainment, Leisure Conference

COMPANY NEWS

880:HK SJM – (Macau Business) Employees of SJM have threatened to go on strike during the golden week of holidays beginning on October 1. The secretary-general of the trade union Forefront of Macao Gaming, Cloee Chao, said the workers would strike if their employer and the government failed to sit down with them to discuss their demand for better pay and benefits. This past Saturday, hundreds of SJM employees marched from Sintra Square to the company’s Grand Lisboa and Hotel Lisboa casinos to demonstrate their dissatisfaction with their pay and opportunities for promotion.

Takeaway: SJM facing increased labor actions which may disrupt the vital Golden Week holiday - Labor woes is becoming another negative headline for Macau stocks.

GENM:MK – BB Entertainment Ltd, a unit of Genting Malaysia Bhd, is paying US$24.6 million to RAV Bahamas Ltd for 16.2 acres (6.6 hectares) of land adjacent to Resorts World Bimini on the Bimini Islands, Bahamas. BB Entertainment owns and operates the casino in the property.

Takeaway: If you can't build a casino in South Florida, build it 50 miles due east of Miami in a lower tax jurisdiction -- the official opening of the first phase of the new Port at ResortsWorld Bimini occurs on Thursday, September 18th with Bahamas Prime Minister, the Rt. Hon. Perry Christie and Executive Chairman of Genting Group, Tan Sri KT Lim attending.

LVS & 1928:HK – (GGRAsia) International ad agency Saatchi and Saatchi announced it was appointed by Macau-based casino operator Sands China Ltd to serve as the firm’s creative agency for the mainland China, Hong Kong and Macau markets. One of Saatchi and Saatchi’s main tasks will be to help promote the US$2.7 billion Parisian Macao casino resort.

Takeaway: The retention of a strong marketing and advertising firm to help drive gaming and non-gaming visits to the Macau and Cotai.

MAR – announced the appointment of Toni Stoeckl to Vice President of Lifestyle Brands including global responsibility for Renaissance Hotels, AC Hotels by Marriott and Moxy Hotels. Mr. Stoeckl previously served as vice president for the Renaissance Hotels brand. In his newly expanded role, his leadership will drive, define and execute global brand strategies and signature programming for more than 225 hotels around the world.

Takeaway: Efforts to appeal to a younger generation of traveler and hotel guest.

MAR – encourages guests to tip to housekeepers as part of new tipping initiative called "The Envelope Please"

Takeaway: A blatant push for guests to pay more…and avoid potential labor relations issues with housekeepers.

HOTEL TRANSACTIONS:

Connecticut-based Starwood Capital Group, is part of a group that purchased Jim Korroch’s SpringHill Suites by Marriott and his Residence Inn by Marriott, both of which are at the Plazzio development at 13th and Greenwich. Also included in the deal is the Hampton Inn & Suites at Regency Lakes at 21st and Greenwich and the Hilton Garden Inn Wichita at Bradley Fair. The total value of the four asset portfolio was greater than $50 million.

Takeaway: It would seem private equity is moving into second and third tier markets in an attempt to achieve higher returns than might be achieved in core, first tier markets.

INDUSTRY NEWS

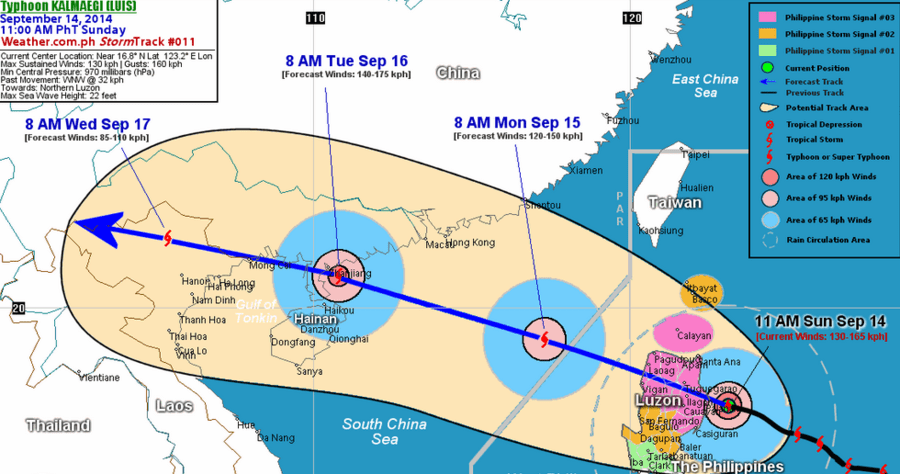

Typhoon Kalmaegi – Typhoon Kalmaegi, known as Typhoon Luis in the Philippines, zipped west across the northern part of Luzon, the northern of the three largest islands in the Philippines, on Sunday. Kalmaegi will then approach southern China's Leizhou Peninsula and Hainan Island Tuesday morning as a category 1 equivalent typhoon and northern Vietnam by Tuesday evening local time, bringing the potential for flooding and some wind damage. The center will stay south of Hong Kong. However, at least some outer rain bands and tropical storm-force gusts appear possible in Hong Kong during that time.

Takeaway: The immediate Hong Kong and Macau areas are expected to experience a typhoon Signal 8 by midnight local time, up from current singal number 3 and could result in a modest impact to Macau gaming due to rough seas impacting ferry traffic.

MACRO

Singapore Macro:

- Retail sales +5.5% in July, mainly due to strong vehicle sales. Ex auto, sales fell 0.4%.

- Excluding executive condominiums (ECs), developers sold 432 new units in August, down from the 509 units sold in July, data from the Urban Redevelopment Authority showed

China Macro:

- Aug Industrial production +6.9% year-over-year vs +8.7% consensus and +9.0% in July, the slowest increase since 2008

- Aug Retail sales +11.9% year-over-year vs +12.1% consensus and +12.2% in July

Takeaway: Disappointing 3Q data from two Asian tigers

Hedgeye remains negative on consumer spending and believes in more inflation. Following a great call on rising housing prices, the Hedgeye

Macro/Financials team is turning decidedly less positive.

Takeaway: We’ve found housing prices to be the single most significant factor in driving gaming revenues over the past 20 years in virtually all gaming markets across the US.