Is CAT the new GE?

We see CAT as caught in a multi-year downswing in resources-related capital spending. Since mid-2012, CAT shares have lagged the index by 23%, but have outperformed YTD amid large dealer inventory builds, easing comps for Resource Industries, and pre-buy activity in Energy & Transportation. In context, however, the outperformance from late 2013 to mid-May looks like a bounce within a longer-term downtrend.

CAT shares have resumed their relative underperformance since mid-year. In 2H 2014, dealer inventory drawdowns and challenging markets outside of the U.S. should pressure Construction Industries margins. At Resource Industries, price declines in key commodities signal ongoing challenges that can be worse than weak mining capital spending. Energy & Transportation may suffer in 2015, after benefiting in 2014, from new emissions standards. In many ways, what we are suggesting is that CAT may be a new GE: a large index constituent poised to underperform over a long period…occasional painful bounces aside.

Resource Industries (RI)

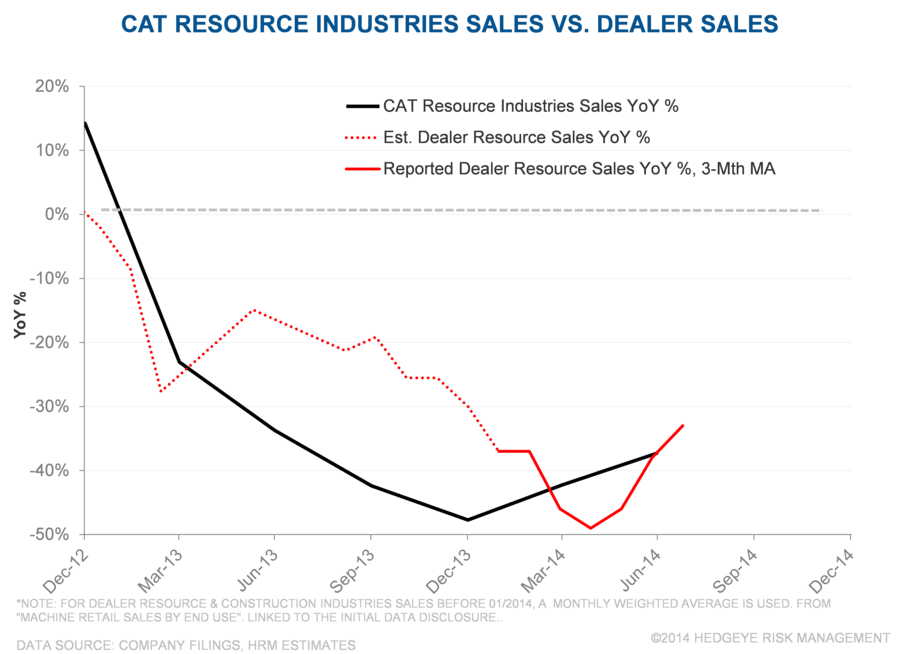

No Rebound Coming: While investors may want to write-off Resource Industries, management does not. CAT remains positioned for a mining investment rebound, with significant capacity still in place. We believe that there is no meaningful rebound pending, as declines in resources-related capital spending represent a return to normal levels, not a decline from them. Equipment pricing is likely to continue lower as better priced orders exit the backlog.

It Can Be Worse Than Lower Mining CapEx: When Phelps Dodge was struggling, their plan to manage low copper prices included: “suspended stripping in a higher cost portion of the mine and will allow for the redistribution of a variety of mining equipment…” High prices yield declining ore grades; low prices improve ore grades. Equipment from curtailed or shuttered mine sites can find its way to would-be buyers of new equipment, pushing new equipment demand well below normalized levels. That is pretty typical for a severe capital equipment downturn. Credit risk is another significant exposure.

Iron Ore, Copper , Coal: Key End-Markets Weakening

Iron Ore: With iron ore prices back on the decline amid ongoing massive supply increases, it is widely expected that higher cost iron ore mines will close. ‘Low’ prices generally result in mine closures after some pain, although it wouldn’t be shocking to see Chinese mines receive some sort of support to maintain local economic statistics. Struggling or shuttered high cost mines create challenges for CAT and other makers of mining equipment beyond weak orders and deferred maintenance. Financed equipment can lead to credit losses; does anyone really want to go pick-up a rope shovel at a bankrupt Australian mine? The iron ore downturn may well be in its early stages.

The idea that iron ore prices are ‘low’ is also a bit fanciful. Less than a decade ago, iron ore sold below $20/ton and often below $15/ton. Our read is that the marginal cash costs for 2015 production, a level at which prices would be ‘low’ or near a ‘bottom’, are well below current spot prices.

Copper: We reviewed the long-term dynamics of copper in our Mining & Construction Black Book last year. Copper supply growth is, by our estimates, set to expand rapidly in 2015 and 2016. Prices have weakened from $3.73/lb at the beginning of the year to $3.07/lb. While not as serious as iron ore, supply growth may further pressure prices.

Coal: U.S. coal and natural gas prices received a boost from last winter’s ‘polar vortex’. Prices for both have since weakened. With the EPA’s MATS rules set to take effect in April 2015, the outlook for U.S. demand appears negative. Coal companies have already shown some credit issues (JRCC, for example). The EIA expects coal consumption “to fall by 2.6% in 2015, as retirements of coal power plants rise in response to the implementation of the Mercury and Air Toxics Standards[MATS]…”. Continued pressure on coal mine investment seems likely.

RI Dealer Inventory: Declines in dealer inventory were a major headwind in 2013, adding to the broader collapse in mining equipment demand. Recent dealer sales have been slightly less terrible, likely due to easing comps and a brief period of higher coal prices. CAT’s North American Resource Industries dealer sales popped up as US coal prices increased following the ‘polar vortex’ last winter. We expect dealer inventories to decline in 2H 2014, but at a slower rate than 2H 2013.

Construction Industries (CI)

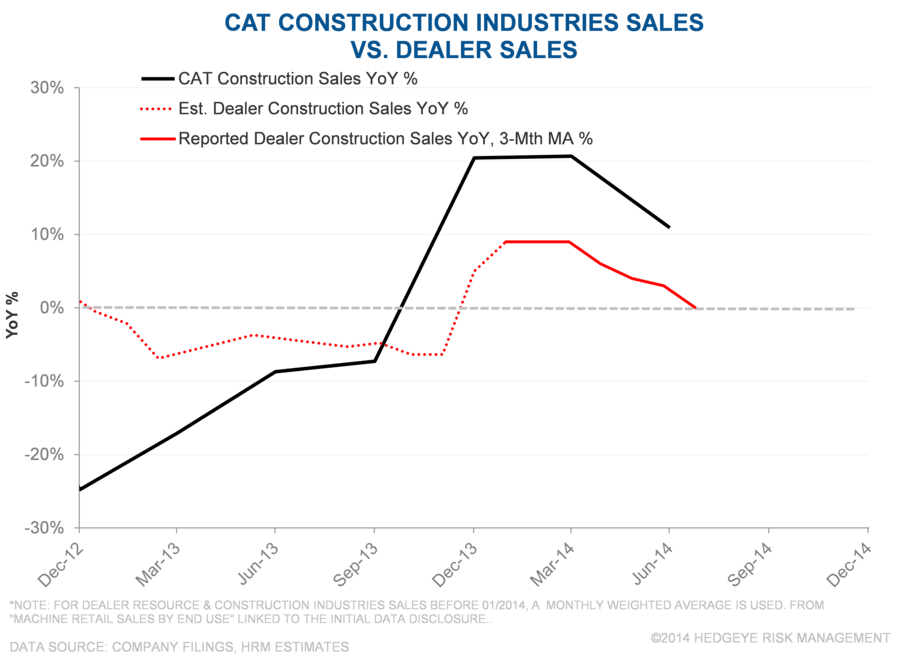

Dealer inventory builds combined with stronger end markets helped Construction Industries report record 1H 2014 margins. However, CI dealer sales growth slowed noticeably in recent months. Slowing demand and dealer inventory reductions in the back half of the year should depress margins from recent highs.

1H 2014 Context and Estimates: To give some context to the dealer inventory builds in 1H 2014 and the drawdowns expected for 2H 2014, we’ll throw out some of our guestimates and understandings. CAT has previously indicated that “Dealer inventory, by and large, they have somewhere … around 3.25-3.5 months of inventory”. (DeWalt, 11/22/12) Excluding parts, this suggests CI dealer inventory of roughly $4-$5 billion. If that estimate is accurate, the 1H 2013 to 1H 2014 change in dealer inventories was a surprisingly large 20%-25%, or ~10%-11% of the segment’s 1H sales (dealer inventory drawdown of ~$400 million in 1H 2013 vs. build of ~$700 million in 1H 2014). The gap between dealer sales growth and CAT Construction Industries sales growth matches the ~10%-11% estimate reasonably well in the chart below.

2H 2014 Tougher Comps: In addition to slowing dealer sales, the inventory drawdown guided for 2H 2014 looks set to create difficult comparisons to 2H 2013. We estimate inventory reductions in both periods, but 2H 2014 looks set to be about $1 billion larger. Given the high incremental margins that CAT has been reporting for CI, it seems likely that margins will decline meaningfully. If CAT reports the flattish CI revenue growth and significantly lower segment operating margins, as we expect, it seems likely that the recent CI optimism would fade.

Energy & Transportation (E&T)

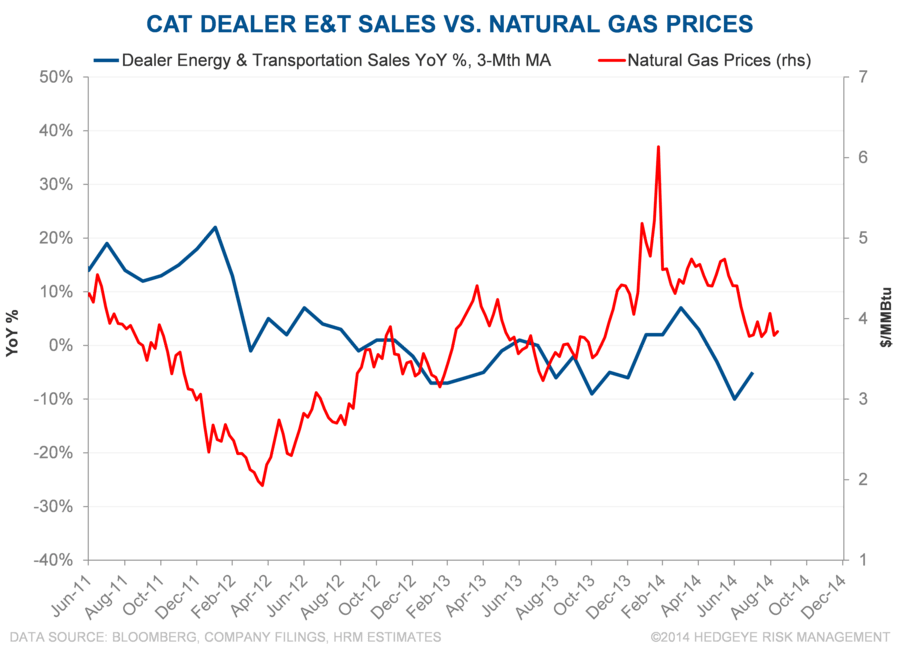

2014 Prebuy Ahead of Big Engine Tier IV Final: In 2H 2014, E&T may well continue to perform well. 2015 looks like a different story, however. CAT has many strong attributes as a company, with its huge engines for gensets, mining/heavy construction equipment, and locomotives being among its most dominant. Tier IV Final U.S. emissions standards go into effect for these large engines in 2015. While a pre-buy is evident in locomotives, it is also a likely significant factor in certain other large engine markets. Cummins noted the following on power generation equipment:

“Quarter-over-quarter increases were driven largely by increased power generation demand in North America and strong truck and construction demand in Europe ahead of the Tier IV Final and Euro VI emissions regulations.” – CMI Investor Presentation 2/6/14

Recent declines in natural gas/oil prices may prove an additional headwind. Better orders from oil and gas end-markets helped in 1H 2014, partly due to an abnormally cold winter. The disclosed dealer sales miss large parts of the E&T product portfolio, but a rough correlation to natural gas/oil prices seems likely (with a slight lag).

Dealer sales growth has slowed in the last few months, which has corresponded to declining E&T segment topline growth. It will be interesting to see how much E&T revenues and margins are impacted by Tier IV in 2015. We think it may prove an underappreciated risk.

Upshot

It seems the combination of dealer inventory builds, higher N.A. coal demand, and a Tier IV Final pre-buy drove a sharp bounce in shares of CAT relative to the sector. We did not anticipate those events effectively, but continue to improve our process and communication. Nonetheless, it appears to us that CAT’s bounce is over and longer-term underperformance has resumed. In the long-term, we think CAT may look like GE a decade ago: a large index constituent to underweight or short pair against better positioned machinery names.