This note was originally published at 8am on August 28, 2014 for Hedgeye subscribers.

“Have no fear of perfection, you’ll never reach it.”

-Salvador Dali

Last night I enjoyed my first major league baseball game of the summer. It couldn’t have been a more perfect night. I had cute Southern gal on my arm and the weather was almost perfect. Sadly, the hometown New York Mets lost in a 3 -2 heartbreaker.

Of course, perfect evenings, days, and stock market runs never last forever. As sad as that is, in life, business, and as stock market operators our luck and performance will always ebb and flow and perfection, should it occur, happens oh so rarely.

In baseball perfection is often epitomized by the so called “perfect game”. A perfect game occurs when the pitcher (or a combination of pitchers) retires 27 batters in a row through nine innings. The pitcher cannot allow any hits, walks, hit basemen, or any opposing player to reach base for any other reason.

Perfection in this sense is extremely rare. In fact, the feat has only been achieved 23 times in major league baseball history and only 21 times since the modern era began in 1900. The last time a perfect game was pitched occurred on August 15, 2012 by Felix Hernandez of the Seattle Mariners.

According to Wikipedia, the first known use in print of the term perfect game occurred in 1908 in the Chicago Tribune. Report I.E. Sanborn wrote the following about Addie Joss’s performance against the White Sox:

“. . . it was an absolutely perfect game without run, without hit, and without letting an opponent reach first base by hook or crook, on hit, walk, or error, in nine innings.”

As it relates to global markets, what is perfection? Is it the SP500 at all-time highs? Is it German bund yields at all-time lows? Is it corporate debt issuance at generational highs and terms at generational lows? Is it car loans at zero percent interest for a 9-year term? Or is it an all-time high in the number of uniformed market mavens appearing on T.V.?

Back to the Global Macro Grind…

Those long of European equities this morning are not dealing with perfect portfolio performance. Led by Russia down just under 200 basis points, European equities are red across the board this morning.

Even as bottoms-up stock pickers in Europe continue to have edge, the U.S. based macro asset allocators seems increasingly concerned about European growth, which was the original reason for being long Europe coming into the year. Clearly, eight months and a life time ago now!

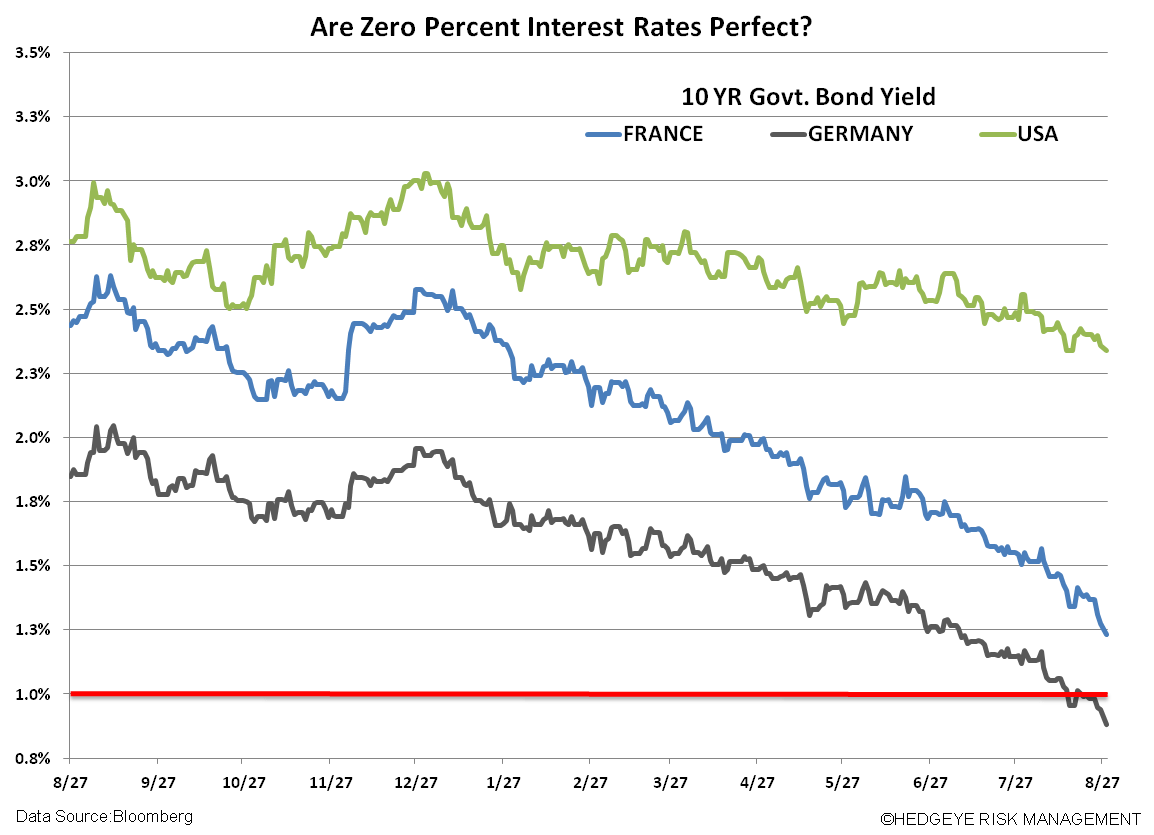

In the Chart of the Day, we compare the interest rates of France to Germany and to the U.S. As you can see, interest rates in these two key European markets have been falling off a cliff versus the U.S. This is probably the best real time market indicator of future economic growth that we know of but, as the Europe bulls would also argue, decelerating growth leaves the door open for more

aggressive easing by the European Central Bank.

This, then, is the new, new bull thesis for European equities. Specifically, that by burning the Euro, Draghi will be able to inflate European equities. But with German 10-year yields below 1.0% and France not far behind, how much incremental easing is already priced in?

As the Wall Street Journal writes this morning, “some sell-side economists, including JPMorgan, Deutsche Bank and Nomura are now pricing in policy easing next week.” Expectations will always be the root of all heartache, won’t they?

One of our favorite sovereigns on the short side continues to be France. As my colleague Matt Hedrick noted yesterday:

“Just two weeks ago France’s government cut its GDP forecast in half (again) to 0.5% (from 1.0%) for 2014 and it will likely miss its FY deficit target of 4%. News this week of President Hollande reshuffling his government (after Economy Minister Arnaud Montebourg stepped down on Monday), is confirming evidence to us that the policies of Hollande’s government are not on track to return growth to the economy over the medium term. That Hollande himself is wildly unpopular, with a paltry approval rating of 17%, furthers the outlook that the government’s pledge that the “recovery is there” is grossly disingenuous.”

Political upheaval and growth getting cut in half are as good a reason as we know to, at a minimum, invest elsewhere if not to get outright short.

Speaking of short ideas (one of Hedgeye’s favorite investment topics) our firebrand energy analyst Kevin Kaiser is adding a new short to the firm’s Best Ideas list this morning and will be hosting a call to discuss his thesis on September 3rd. As Kaiser writes:

“VNR is a serial-acquisition / roll-up story that now sports a $2.5 billion market cap and $4.0 billion enterprise value after 22 separate acquisitions since 2008. It is owned primarily by retail investors for its outsized distribution yield (8.5%) and monthly distribution payments. VNR has actually trademarked the slogan, "The Monthly Distribution MLP.

But what unwitting investors don't realize is that VNR finances its distribution payments with capital raises - call that what you want to call it. In our view, VNR's "game" is at the beginning of its end. When VNR's distribution is ultimately cut, investors will discover that the Fair Value of VNR is substantially below the current market price.”

Vanguard is a whole lot of yield, with very minimal cash flow. Usually a toxic mix!

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.32-2.41%

SPX 1985-2013

CAC 4152-4439

USD 81.91-82.78

EUR/USD 1.31-1.33

NatGas 3.85-4.06

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research