DETAILS

We like LULU, but it is not for the typical reasons we traditionally look for in a long. We added the name to our best ideas list on June 15 because of our view that things were so pathetically bad at LULU, that it would lead to positive change. Add on what we thought was capitulation by the sell-side (LULU currently has its lowest Buy ratio in history), and very defendable downside in the low-mid $30s due to attractive LBO/acquisition math, we think that this is ripe for a restructuring. Even most LULU bears would probably admit that this is a very strong brand in a superior category with global appeal – they’ll probably just argue that the competition is too fierce and LULU is ill equipped to face it head-on. We actually agree with that logic. That’s why it needs to be changed radically from what we see today. Yeah, John Currie is on his way out as CFO – that’s a plus. Also, Chip Wilson sold half his stake to Advent, and we think that the rest of his stake is on the way out. But, we think the change we’ll see will be a lot bigger than that. The problem is that this is a global mid-cycle growth company approaching $2bn in sales, but it has a management team that is appropriate for a sub-$500mm localized brand.

As for what’s next on the ‘change agenda’, we think that the speed of change depends on the company’s own financial results. If the next couple of quarters pan out as we think – which is not very good – then we think the most probable outcome is that the Board fires Laurent Potdevin – the CEO it hired just 8 months ago. He’s simply not the right guy for the job. Never was, and never will be. He’s only led small brands like Toms and Burton, but he simply does not have the skill set to make LULU a great global brand with efficient operations across multiple distribution channels. Our view is that the only reason the Board approved Laurent is because Chip simultaneously agreed to give up his Chairman title if Potdevin was named CEO. That move left Wilson powerless (no Chair, no CEO, no majority, NO power), which led to him unwinding his stock. It also suggests that the Board is not married to Potdevin, and we think it will make the right call in replacing him if need be. We think that there’s an 80% chance that Potdevin is gone in a year’s time.

There are a lot of other changes as well beyond human resource management. Other changes should be made regardless of who is at the helm – like developing a competitive pricing process. LULU is the worst company that we’ve seen in many years when it comes to appropriately changing the prices on its product as the selling season progresses. It needs the information systems, potentially physical outlets, and definitely a more sophisticated system to sell aged inventory online and ship directly from stores. And yes, it might even need a wholesale model. These are all decisions that should be vetted by the management team LULU deserves – but does not have.

So basically, if trends weaken further and it is clear that this management team cannot create value and grow this business profitably, then we think we’ll see a completely new executive team put in place to make it happen. Advent did not buy back 14.8% of LULU for $845mm after all these years to passively watch it die on the vine. So in this case, we think Bad News = Good News. If by chance (and we think it would be sheer luck) that this management team gets this engine running, then that’s probably good for the stock as well. Good News = Good News.

We’re very careful about these ‘things are so bad that it’s good’ calls, because they usually have a way of missing even lowered expectations and destroying value. But that mattered to us when the stock was near $70, and even earlier this year when it was in the $50s. But with the stock in the high $30s, sentiment worse than it has ever been (EVER is a long time), and value investors increasingly coming out of the woodwork exploring with us what the trough earnings number is for LULU (it’s $1.50, by the way), we’re simply not as concerned at current levels. Could it trade down on horrible print? Yes, but we think things are bad, not horrible. In a perverse way, we’d like to see LULU faceplant this quarter. Because we don’t think the equity market would punish it commensurately to the economic impact of the miss itself, but it would be an event that would likely cause the Board to shake things up. Ultimately, there is $4bn in revenue to be realized here – likely at a high-teens margin. That’s $3-$3.50 in EPS power. At $38, that’s 11.6x earnings, and 7.5x EBITDA. Sounds pretty defendable to us. We just need a team in place that can deliver.

THINGS TO CONSIDER FOR THE QUARTER

- In LULU’s 28 quarters as a public company it has beat estimates 27 times by an average of 16.5%. Over the past 8 quarters the average beat was 7%. There have been pre-announcements and guide downs along the way, especially over the past 12 months, but in general LULU doesn’t miss.

- Luon Recall was 3/18/13 and Luon was back on shelves 6/4/13 about a month into the 2nd quarter last year

- Chip comments on Bloomberg fell at the start of the 4th quarter (11/5/13)

Revenue

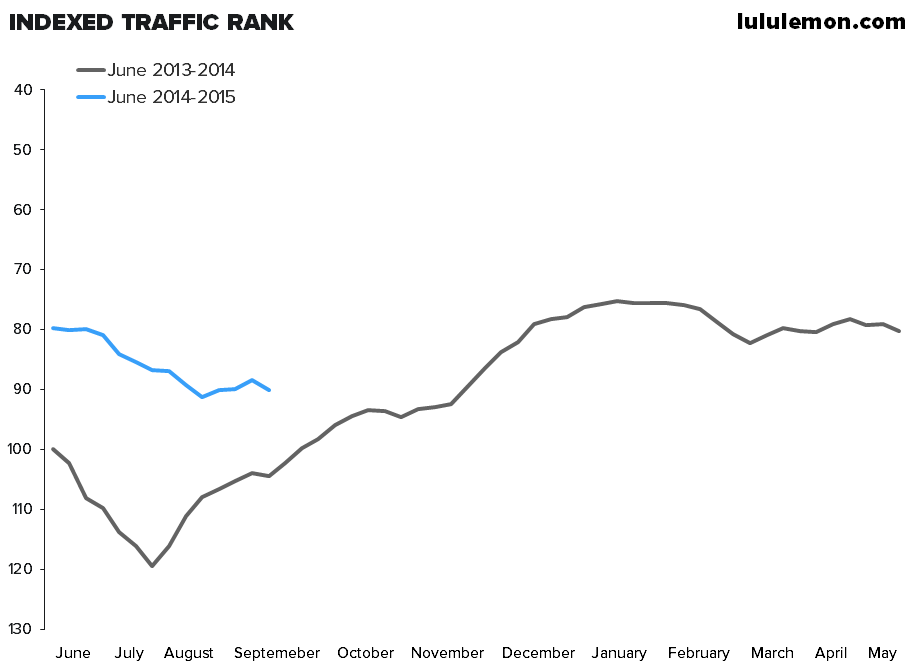

- Internet traffic rank which takes into account organic visits and page views per visit was up 25% relative to all other sites on the internet.

- Monthly traffic improved sequentially in June and July from trough levels in May and was up 68% in the quarter. A 2000bps improvement sequentially from 1Q14. The improvement could be driven by LULU jamming more inventory through the e-pipe. That could have negative margin implications, or if it does not result in better e-comm sales it could simply mean that the company did a lousy job converting. But the trends initially look decent.

Gross margin – key negative driver here are product margins

- Over the past 5 quarters (1Q13 -1Q14) product margins have been down by 90bps, 220bps, 220bps, 270bps, and 310 bps respectively. Two year comp in 1Q, -200bps. Management guided margins down another 300bps for the upcoming quarter that would assume product margins down 200bps, 50bps from fx, 30 – 40bps hit from new Ohio DC. Much of deleverage comes from mix away from core to seasonal which has lower IMU due in part to inefficient supply chain and inventory chase.

SG&A

- Investments listed below and 14 pop-up shops adding an incremental $10mm in SG&A

Revenue Drivers

Near term stop gap measures intended to drive ‘traffic and sales’. These all seem weak at best. But it’s what LULU has called out.

1) Allocating additional floor space to men’s at store locations in Santa Monica, Vancouver, and Miami

2) London – on track to do in excess of $2,200 per square foot in year one

3) A social media platform focused on Brand Ambassadors

4) In-store tablets allowing guests to shop online inventory

5) Paid search advertisement

6) 14 pop up shops across the US and Canada open from April through September

Long term (these make more sense to us, but only partially address LULU’s problems)

1) Additional 120 stores to be added across North America

2) 40 international stores (20 Europe, 20 Asia) by the end of 2017 in addition to anything added on top of 30 store base in Australia and NZ

3) Go to market calendar – Spring/Fall 2015

4) Rebalance of core and seasonal product – Starts in 2H14 but won’t be fully implemented until 2Q15

5) Revamped product engine – 1Q16

Guidance Considerations

Getting within spitting distance of management guidance for the quarter is not terribly heroic. To get to the mid-point of guidance and in line with consensus for the quarter calling for revenue of $375mm - $380mm and EPS of $0.28-$0.30 we need to assume the following…

1) Revenue growth of 9.6%. Square footage growth of 20% YY, -4.3% consolidated comp (-9% store and +22% DTC).

2) Gross margins down 300bps and flat sequentially from the first quarter on the 2yr trend line

3) SG&A up 25%, implying 440bps of deleverage

4) EBIT margins down 738bps YY.

5) EPS growth of -26%

A little tougher to get to annual guidance. To get to the mid-point of guidance and in line with consensus for the full year calling for revenue of $1.77bil - $1.80bil and EPS in the range of $1.71-$1.76 we need to assume the following…

1) Revenue growth of 12%. Square footage growth of 18%. Flat consolidated comps (-5% store and +24% DTC).

2) Gross margins down 170bps to 51%.

3) SG&A up 24%, implying 300bps of deleverage

4) EBIT margins down 465bps

5) EPS growth = -10%