Last Friday Keith added a short signal in Italy (via the etf EWI) to our Real-Time Alerts. We were tactically afforded the opportunity to short EWI as Italian stocks have bounced to lower-highs but remain bearish TREND (21,525 in the FTSE MIB Index).

Getting Short Persistent Italian Underperformance

Our thesis on Italy is relatively simple:

- GDP Underperformance – a 2H deceleration should lead to 2014 Italian GDP flat to -0.3% versus +0.6% to +0.8% in the Eurozone.

- Sticky Unemployment – we expect the unemployment rate to be grounded at 12-13% for the remainder of the year, versus Eurozone average of low to mid 11%. Italy’s monster Youth Unemployment of 42.9% will continue to present a real drag on confidence and extend the length of a “recovery” over the medium term TREND and pose a generational drag over the long term TAIL.

- Fiscal/Budget Squabbles – we continue to get mixed signals from the Renzi government. More fiscal consolidation or less? The lack of a definitive voice should only provide further uncertainty to the populous and dampen consumer confidence around an inflection: late last week undersecretary at the economy ministry Enrico Zanetti said that Italy may seek to delay bringing its structural budget deficit into balance until 2016 (versus the previous guidance of 2015).

- ECB is No Savior – despite cutting the main interest rates to near zero and deposit rates to negative first in June, the policy move to further cut last week will not lead to increased lending to businesses that are willing to invest in and grow the European economy. We expect investment to the region, and Italy in particular, to remain severely challenged over the medium term.

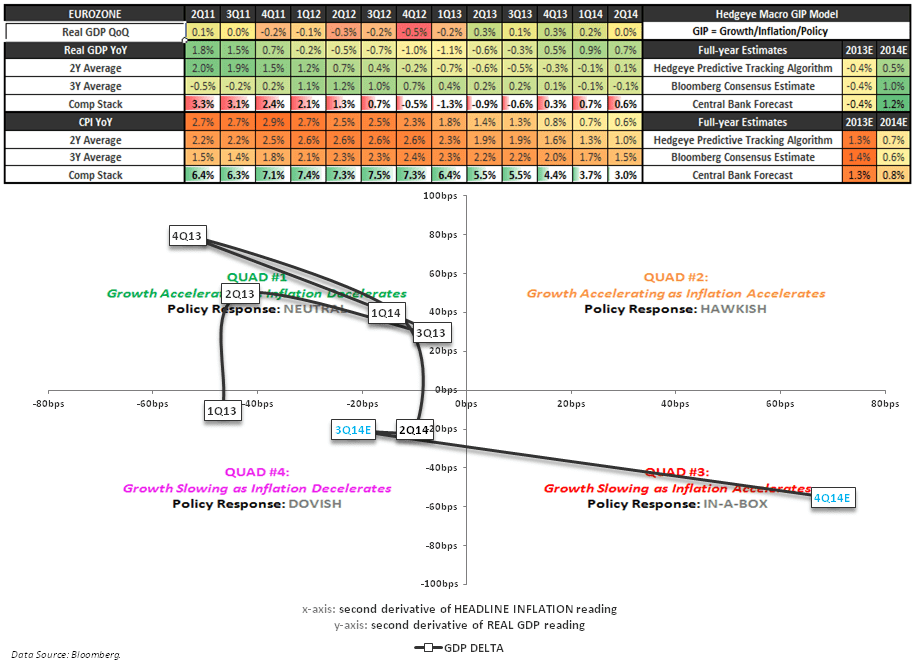

- Regional Partners Also Weak – we have monitored weeks and months of declining data across the region and our propriety GIP model (growth, inflation and policy) for assessing economies suggests the Eurozone economy will land in the ugly quads #3 and #4 in 2H, representing growth slowing as inflation decelerates/accelerates. With 54% of Italy’s exports heading to EU countries, we suspect that weaker demand from the EU in 2H will continue to put downward pressure on growth.

Just Charts

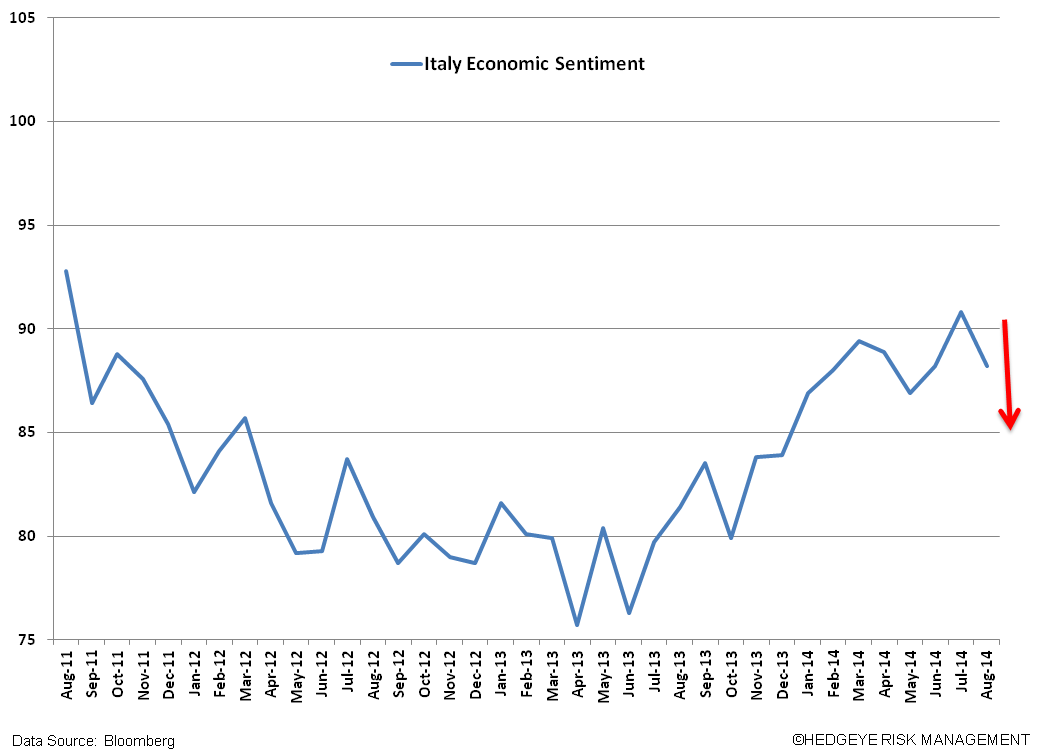

Below we show 4 charts that are representative of Italy’s underperformance.

- Italy’s PMI Services for the August reading ticked below the 50 line, indicating contraction

- Italy’s Unemployment Rate is poised to remain above the Eurozone average

- Italian Retail Sales have inflected back to the downside

- Italian Economic Sentiment inflected downward in the August reading – we expect further declines in 2H

Matthew Hedrick

Associate