Conclusion: We think that people are missing the magnitude of earnings growth at RH, the sustainability of that trajectory over a long period of time, and ultimately the degree to which that will accrue to equity holders. The question is not whether the stock will go to $90 vs $100 (where we see most price targets), but whether it will get to $200 vs $300. Even the best stories, however, are not linear. There will be bumps along the road. But this print should not be one of them. We’re well above the Street in Sales, Margins and EPS, and we flush out in this note where we could be wrong.

DETAILS

We still think that RH is the best idea in Retail today. We think that most parts of the thesis are at least acknowledged by the market (category growth, real estate expansion), but people are absolutely missing how all the pieces are coming together to drive such outsized earnings growth over an extremely long duration. The consensus is looking for long-term earnings growth of 28% -- we’re at 45%. That equates to $11 in earnings power by 2018. At a 45% earnings CAGR, what kind of multiple does this kind of earnings growth deserve? 25x? 30x? 40x? UnderArmour has a 30% CAGR and it trades at 65x earnings. Our point here is that if the consensus is as wrong as we think it is on the earnings trajectory, then it will be equally wrong on the multiple. 25x = $275. 30x = $330. 40x (which seems like a stretch) = $440. Yes, that’s 4.5 yrs out, but even discounted [30x $11 = $330) back by 15% over 4-years and you get about $190 today. You want to use an earnings number closer in? We’re at $6.25 in 2016. The Street is at $3.76. Let’s keep the current 30x multiple, though we’d argue that we’ll see multiple expansion if numbers are going up that high. That suggests a $188 price in about a year and a half. This stock is headed a lot higher.

All of that said, we fully acknowledge that the slope of a multi-year earnings growth story is not linear – especially for an early-cycle transformational story like this. There will definitely be some bumps in the road along the way, but we simply don’t think that the quarter to be reported after the close on September 10 will be one of those bumps. The way we see it, RH is in an enviable position in that it could print a number as high as $0.77 if it so chooses (compared to the Street at $0.64) without borrowing from investment dollars that should otherwise be spent to fuel the long-term plan.

Here’s a look at some key line items – and a little stress-test on where we could be wrong.

Revenue: We are at $468 for the quarter, ~3.5% above the top end of guidance and consensus. There’s a few important factors to consider here.

1) First off, remember that two points of growth were pulled forward into 1Q. That’s in our estimates.

2) This is the first full quarter where the Flatiron store in NYC will be pulled out of the comp base. That’s meaningless as it relates to Sales contribution. In fact, the store is a positive for the top line because the newly renovated store can begin to boost revenue. But it is the most productive store in the whole fleet (we think it accounts for 5-7% of sales) and it will no longer be part of the reported ‘comp’. We think we have this accounted for properly, but if our 21% comp proves wrong, we think this is the most likely factor.

3) The late source book launch this year, shallow inventory buy to support the product refresh, and extended fulfillment windows could push revenue for orders booked in 2Q into 3Q. Similar to last year where the 2Q brand comp of 29% was bookended by a 40% brand comp in 1Q and 38% brand comp in 3Q. We think we have this factored into our model appropriately, but it is a part of the model where we could revenue shift between 2Q and 3Q.

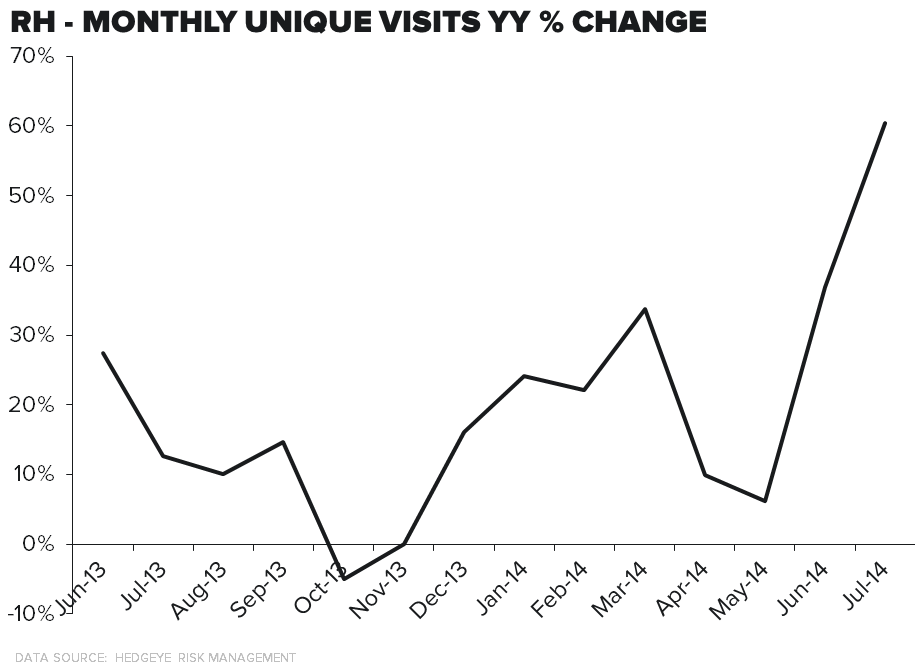

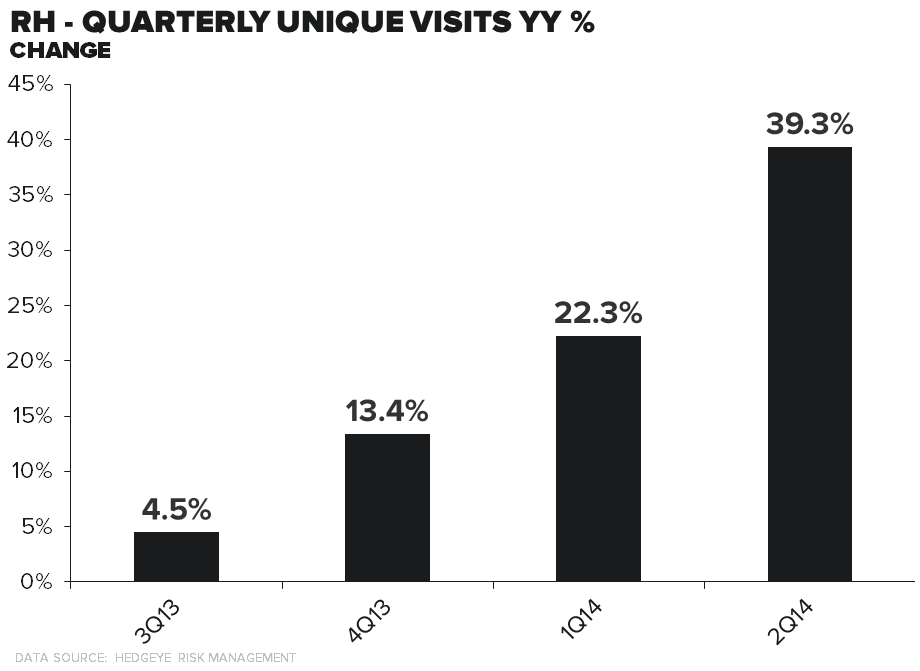

4) We think that the on-line business looks solid. Based on the strength we’ve seen in our e-commerce index over the past few months, it is clear that RH is drawing a lot of incremental interest to its web site. This synchs with the timing of its sourcebook, so it is to be expected from where we sit. But the company is clearly executing well in driving its online strategy in conjunction with selling product in physical stores.

Gross Margin: This is the area where we’re probably the most aggressive in our model, with a 200bp improvement vs last year. A couple points…

1) Last year margins were down 250bp due to significant pricing actions, and we don’t think RH is anywhere near as aggressive this year.

2) A quick point on Order Fulfilment: RH does not get paid by customers until the product is delivered. As such, Fulfillment is the key to revenue recognition. We think the company is in a much better position this year to fulfill orders than LY for two reasons. a) Inventories are in a much better position to meet demand headed in to 2Q. The sales to inventory spread (sales growth – inventory growth) was -11% in 1Q14 compared to +3% in 1Q13. b) The company has added over 1.2mm sq. ft. in DC square footage, an increase of over 30% since 2Q13. That should help alleviate some of the shipping bottlenecks attributed to the once per year product refresh.

3) Dead Rent will start to be an issue. It should not start to deleverage occupancy until 3Q, but these deals are definitely in constant flux. We wouldn’t be shocked in the least to see it opportunistically take control of certain properties earlier than expected to give it room with construction. This shows up entirely in COGS. But to illustrate, a property line Denver/Cherry Creek will be about $2mm in rent per year. An extra quarter is $500k, or about a penny a share.

SG&A: Not a ton of moving parts here. We have SG&A growing at 20% this quarter, a rate that we have accelerating throughout the year as the real estate plan plays out and the company laps its change in Source Book strategy. Our math suggests that RH will spend an extra $52mm this year on its 3,200 page Source Book, but that will be amortized over a 12-month time period. Most of the year-over-year increase will be recognized in the back half of the year. One thing that’s worth noting is that we’re only modeling 54bps of SG&A leverage. That’s the smallest SG&A leverage rate RH will have achieved since 3Q11. In other words, we think our estimate is on the conservative side.

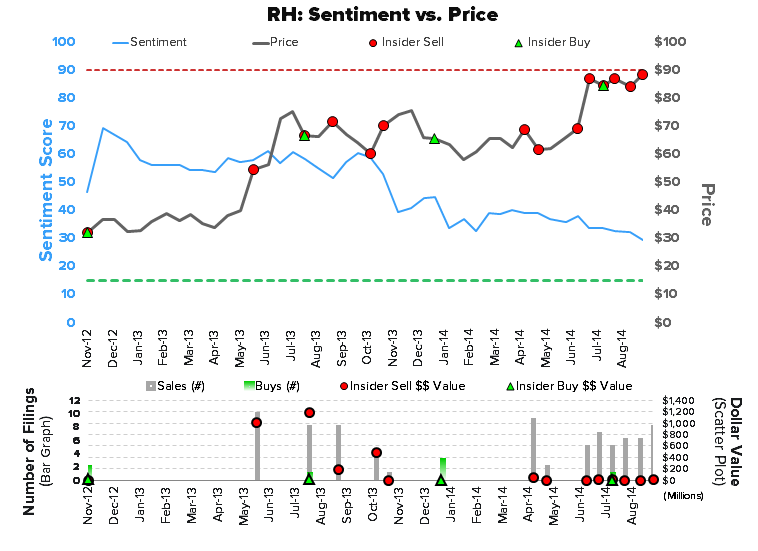

Sentiment Considerations

We think that sentiment factors are checking out for RH. Consider that the stock popped on the last earnings print but has actually traded down 12.2% since the June 30 peak, compared to a 2.4% gain for the S&P. In fact, our Sentiment Monitor looks abysmal for RH. This combines both sell side ratings and short interest, and the simple fact is that Sentiment for RH has never been worse. It is almost entirely driven by elevated short interest, which stands at 7.4mm shares – an all-time high. It’s up modestly since RH priced its convert, which makes sense as people buy the convertible and simultaneously short the equity. But the fact remains that 20.7% of the float is currently short. We’ll take the other side of that. In addition…

- When Williams-Sonoma guided down for 2H, it definitely sucked some of the air out of the momentum sail for RH. RH lost 6.8% since the WSM miss – even though most of the factors were WSM-specific.

- Though not a traditional peer, RH traded down when Kate Spade put up an otherwise spectacular quarter, but the stock was crushed due to a poorly communicated message regarding long-term outlook. Our sense is that from a PM’s perspective, these names are pretty much in the same bucket. Consumer discretionary, momentum, significant operational leverage, high multiple. We had several calls that week from people afraid that RH was going to be the next KATE.