TODAY’S S&P 500 SET-UP – September 5, 2014

As we look at today's setup for the S&P 500, the range is 29 points or 1.03% downside to 1977 and 0.42% upside to 2006.

SECTOR PERFORMANCE

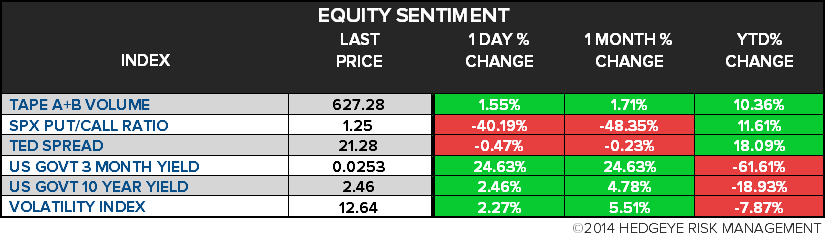

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.91 from 1.92

- VIX closed at 12.64 1 day percent change of 2.27%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Change in Nonfarm Payrolls, Aug., est. 230k (pr 209k)

- Unemployment Rate, Aug., est. 6.1% (prior 6.2%)

- 1pm: Baker Hughes rig count

- 3:45pm: Fed’s Rosengren speaks in Boston

GOVERNMENT:

- Senate, House out on final week of summer recess

- President Obama views fly-over ceremony, attends NATO summit in Wales, holds press conference, returns to Washington

- 10am: Nebraska Supreme Court hears constitutionality arguments on Keystone XL pipeline route through state

- U.S. ELECTION WRAP: Kansas Senate Race; Koch-Backed Ads

WHAT TO WATCH:

- Jobs-Day guide: U.S. payrolls, participation, wages and hours

- Barclays, Citigroup accused in suit of manipulating ISDAfix

- Apple plans new security features after hack of celebrity photos

- Ukraine ready for truce as NATO cautions on Russian peace offer

- Gap falls as August same-store sales trail analysts’ estimates

- Keryx has 82% chance of winning FDA Zerenex approval: analysts

- Nvidia sues Samsung, Qualcomm after patent deal talks fail

- German industrial production expands in sign of eco. rebound

- Eurozone GDP stagnates in 2Q; flash reading unchanged q/q

- Median incomes fell for all but richest in 2010-13, Fed says

- Swaps rule requires $644b in collateral, regulator says

- Autonomy CFO told Lynch of "imaginary deals’’ before HP sale

- Dollar General’s Family Dollar bid may not be enough: Reuters

- Bain Capital’s Atento may start U.S. IPO next week: Reuters

- Apple files reality navigation patents: AppleInsider

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Long-Term Oil Demand to Slow Even With Higher China Consumption

- Copper Rises in London Before U.S. Jobs as Surplus Seen Elusive

- Chemical Boom at Risk as U.S. Ethane Heads Abroad: Commodities

- WTI Heads for Weekly Drop as Refiners Slow Rates; Brent Steady

- Raw Sugar Extends Drop to 7-Month Low While Arabica Coffee Falls

- Gold Is Little Changed Near 12-Week Low Before U.S. Jobs Data

- Sugar Output in India’s Biggest Producer Seen at Three-Year High

- Corn Rebounds as Cooler U.S. Temperatures Raise Frost Concern

- Russia Reports Outbreak of Classical Swine Fever in Southwest

- Rebar Posts Biggest Weekly Loss in 15 Months as Demand Wanes

- Palm Trims Biggest Weekly Gain Since November as Reserves Climb

- Pears Rot in Europe as Putin’s Retaliation Pushes Price Down 70%

- Copper Traders Most Bearish in Month as Demand Seen Stalling

- One Putin Ally Sells Stake in Chemical Maker to Son of Another

CURRENCIES

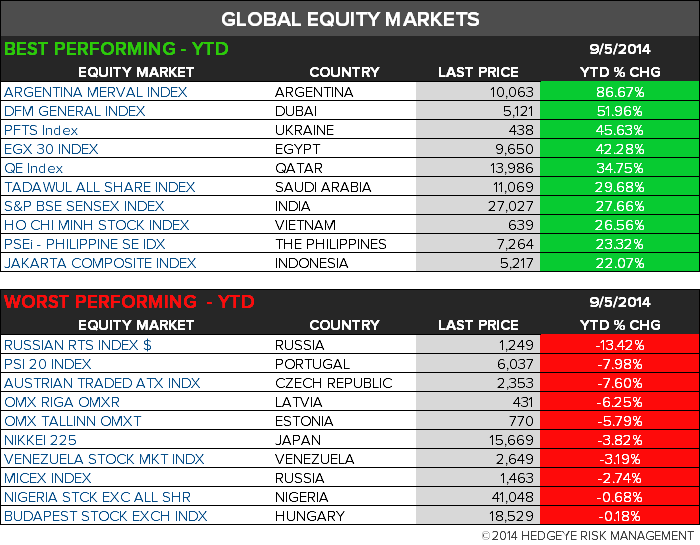

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team