Although our short thesis is complicated, it can effectively be boiled down to one chart.

MCD plans to release August sales numbers on September 9th and we have a sneaking suspicion it will be a negative event. In all likelihood, it will lead the street to revise down its full-year sales and earnings estimates.

Recall that McDonald's global same-store sales declined -2.5% in July and we'd expect August to yield similar results.

In July, performance by segment was:

- U.S. -3.2%

- Europe +0.5%

- APMEA -7.3%

Currently, 3Q14 consensus estimates by segment are:

- U.S. -2.0%

- Europe -0.7%

- APMEA -5.8%

EPS Estimates are too Aggressive

Consensus currently expects MCD to report flat sales and earnings growth in 3Q14. This looks aggressive, however, considering system-wide sales declined -0.5% in July and are likely to be down again in August. Flat sales growth is too optimistic and, given the negative leverage inherent in the business model, reporting a flat EPS number is also unlikely.

The street expects MCD to post $1.52 in earnings in 3Q14 after posting the same number last year. It also expects MCD to post 1.4% EPS growth in 4Q14. Both of these numbers are, in our view, aggressive.

With a recovery, albeit minor, built into 4Q14 estimates, the trend line is expected to accelerate to 8% EPS growth by 1Q15 and stay at that run-rate for the remainder of 2015. We often hear the bulls cite easy comparisons to defend their optimism, but the reality is we've been hearing that for several years. 2014 was a time of easy comparisons for the company and it isn't close to hitting estimates published at the beginning of the year.

From our perspective, management isn't willing to take the necessary steps to fix the business and, until this happens, we expect MCD to consistently underperform expectations.

Risk/Reward Setup Suggests the Stock Is a Short

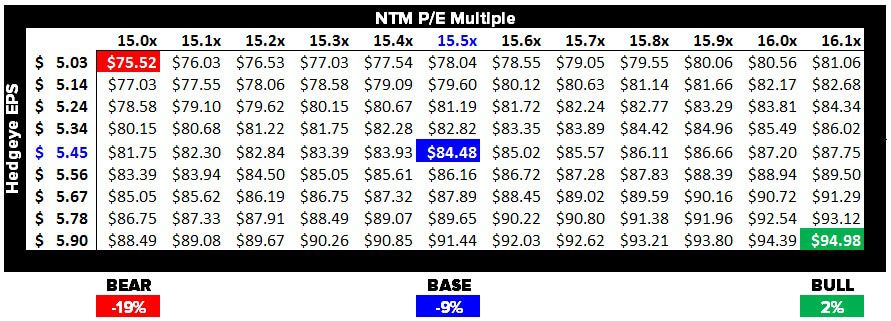

MCD is currently trading at 15.9x the NTM EPS of $5.87, but looks substantially more expensive when assuming that $5.87 is far too aggressive. Barring some unexpected event, the odds that MCD delivers 8% EPS growth in FY15 are slim-to-none.

We believe that in 2014 MCD could report its first down year in EPS growth since 2002, as we expect full-year EPS to come in between $5.40-5.45 or 2-3% below the current consensus estimate. More importantly, we suspect McDonald's will even struggle to grow EPS off of this lower $5.40-5.45 base. As a result, our 2015 EPS estimate of $5.45 is nearly 10% below the current consensus estimate of $6.02.

Looking out over the next six months, assuming a constant multiple of 15.9x on our NTM EPS estimate of $5.40 gives us an $85 stock representing approximately 9-10% downside from current levels. We understand this is not a "major blow-up," but if the stock saw a little multiple compression (down to the 14-15x range) we're talking about 15-20% downside or about a $12-20 billion decline in market cap.

Feel free to email or call with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst