On August 21st we hosted an expert call with Judith Gaines of J. Gaines Consulting featuring her fundamental, non-consensus call that the outlook for Brazil’s crop into 2015-16 is much worse than expected. Coffee has remained in a BULLISH @Hedgeye TREND set-up for all of 2014 and spot prices have increased +8% since we hosted the call less than two weeks ago (+80% YTD).

Spot Arabica finished +4.4% yesterday after The International Coffee Organization (ICO) reported that cash market prices have been markedly-higher in recent days by Brazilian and Colombian farmers:

- Brazil: $1.9050/lb.

- Columbia: $2.2150/lb.

Most importantly we will continue to watch the change in cash prices from farmers over the next several weeks for a read-through on the severity of the tree damage as an indicator for the health of next year’s crop.

Here are a few of the key catalysts- which we expect to continue playing out over the next several weeks:

- For the first time we are looking at a two-year production deficit vs. a normalized year-on, year-off production cycle:

- Late winter frost last year: Brazilian November-December mild frost lowered crop quality

- Severe Drought: Drought and lack of moisture in tree root system from January-March during the vegetative period

- Heavy Rainfall: Late timing of heavy rainfall knocked flowers off trees, reducing the available volume for harvest (CURRENT CATALYST)

- Brazil WILL NOT produce enough volume in 2015-2016 to meet the global market demand for Arabica coffee

- End-User Risk: Possible to hedge price risk but a shortage in coffee to cover all deliverables is an un-hedgeable risk in 2015-16

- Aggregate demand next year is expected to be around 34 million bags. However due to a current stock deficit and severe crop damage, Brazil’s production yield will be just 27 million bags in 2015

- Not enough capacity from other countries to cover the expected crop shortage of Arabica coffee in Brazil

- How High Can Prices Go? $2.75-$4.00/LB. There will likely be a spike in prices for Arabica and a higher basis for other grades of coffee.

- Outlook in Vietnam and Indonesia looks worse year-over-year with Columbia picking up part of the slack

Over the next several weeks we expect a continuation in analysts pointing to irrelevant catalysts including current weather patterns…

One of the key differentiators for Judy’s argument vs. consensus reasoning as to why prices will increase is that the damage from poor weather has already been done. Here were some of the headlines yesterday after the ICO reported higher cash market prices:

- “Less rainfall during the flowering period” (which is happening right now)

- “Rains needed to aid coffee crop development seen delayed by two weeks”

- “Weather affecting near-term Brazilian coffee outlook”

Why we will certainly be watching the change in expectations for the supply/demand outlook in the coming weeks, market activity has supported the move higher:

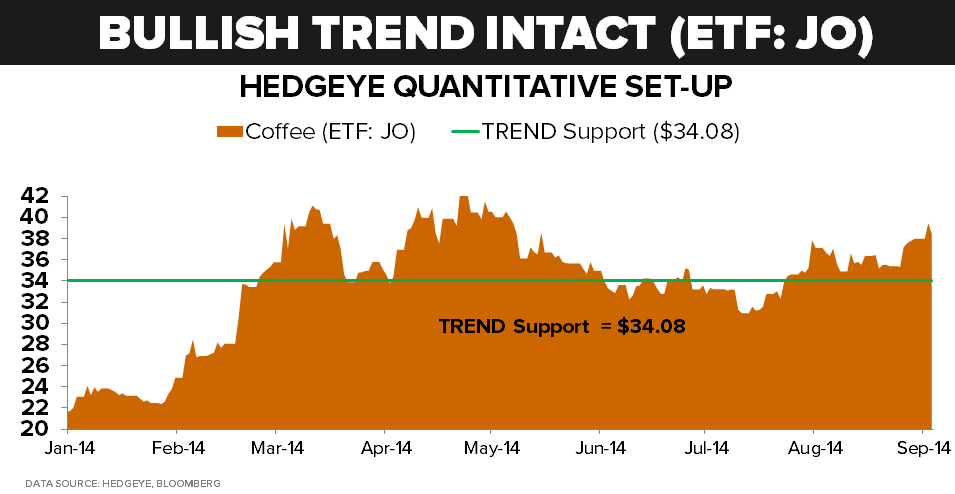

- QUANT: Coffee remains BULLISH from a TREND Perspective with support at $34.08

- QUANT: is the most bullish commodity in our TACRM model aside from the base metal complex which continues to ride the strength in China

- VOLATILITY: Coffee was up +7.8% last week with volatility bid near YTD averages on the move. The adjustment for implied volatilities suggests the market believes in the move:

Note: The adjustment in upside skew (difference in implied volatility between at the money calls and out of the money upside calls) to the average relative implied volatilities despite the +7.8% move suggests the market is willing to pay the same value for the same relative upside price risk after a significant run.

- VOLUME: Aggregate volume last week on the move ~75% of 1/3/6-month averages which was consistent with summer-end volume trends in other commodity markets

- VOLUME: +4.4% yesterday on healthy volumes:

- +21% vs. 5-day avg.

- -12% vs. 1m avg.

- -2% vs. 3m avg.

- -8% vs. 6m avg.

- SENTIMENT: Forward Curve in Futures Market positioned for higher prices:

- Sep-Dec. basis = +2.23%

- 1-yr basis= +~6%

- 2-yr basis=+~7%

- SENTIMENT: CFTC data shows the market is moving to position itself behind this bull story which is the common herding mentality when a market runs. Sentiment gets more bullish on the run. We view this as contrary indicator, so it’s something we’ll watch. The data is based off of the net length of futures and options contracts:

- +3.4% longer week-over-week

- Market long +46K contracts or approximately 2x 6-month aggregate daily futures volume

- Market long +1.48 standard deviations vs. trailing 12-month average contract length

Despite a market that is positioned for higher prices into next summer, Judy’s price estimate in the $2.75-$4.00/lb. range remains well above current consensus positioning. We expect more color on the potential crop devastation into October and November.

As always, please ping us with any comments or questions.

Ben Ryan

Analyst