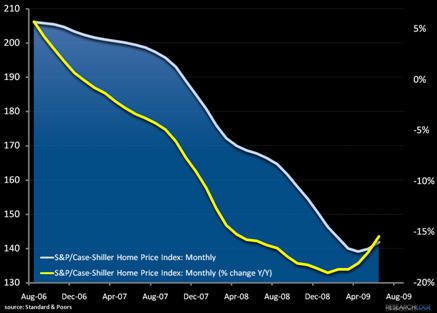

The S&P/Case-Shiller Home Price Indices are calculated monthly and published with a two month lag. It was reported today that the Standard & Poor's/Case-Shiller's U.S. National Home Price Index rose nearly 3% in 2Q from 1Q. In January we predicted that the housing market will improve in 2Q. It has.

Home prices are still down 15% year-over-year in June (better than the expected consensus decline of 16.4) and down 30% from the peak in the second quarter of 2006. The housing market is bottoming, but there is clearly a long way to go to get back to the peak.

Last week, the NAR reported that existing home sales jumped 7.2% to an annual rate of 5.24 million homes, the highest since August 2007. With the S&P/Case-Shiller housing numbers now showing sequential improvement for the last two months, we would expect the existing home sales numbers to continue to get better in the short run. If house prices have stopped going down and the free money policies persist, it makes sense to think that consumers will have an increased propensity to buy new homes, helping to gradually push market prices for homes higher (with “dark pools” of inventory overhang waiting in the wings to keep a ceiling on any substantial rally) .

As we head into 4Q09, however, we are likely to see the best data points in housing in the rear view mirror as a result of the following three points (reiterated from last week):

(1) THE PEAK SEASON - For those consumers with “need based” moves, it’s August and the kids will be back in school soon, if they aren’t already.

(2) INTEREST RATES - Interest rates are headed higher in Q4. See Keith McCullough’s note on “Bernanke Pandering” and you will get the picture.

(3) THE GOVERNMENT - The Government home buyer stimulant is going to end. The deadline to close a home purchase is November 30, 2009. The process of buying a new home is not quick and easy - finding a home, lining up financing and getting inspections and closing, all takes time to accomplish.

Howard W. Penney

Managing Director