We’re seeing 3Q growth estimates come down today (again) alongside soft consumer spending data in July.

Real consumer spending declined the most in 6 months to start 3Q, decelerating on both a 1Y and 2Y basis with softness ubiquitous across Services, Durables and Nondurables. Notably, the savings rate ticked up to 5.7% - the highest level in 18 months.

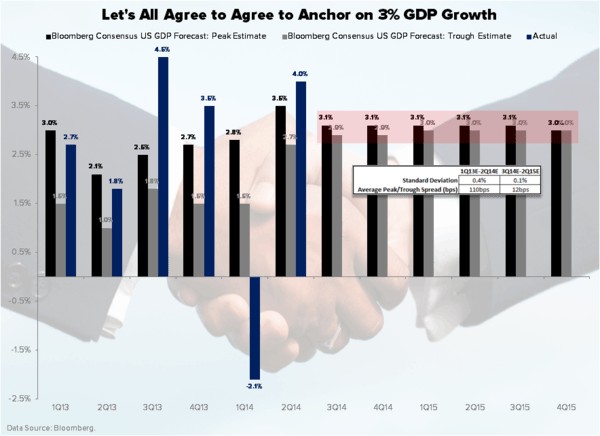

In short, while the income-savings dynamics are shifting favorably for forward consumption, in the immediate/intermediate term (& inclusive of today’s negative growth revision), we think consensus estimates - which remain laughably linear – need to come in further.

Christian B. Drake

@HedgeyeUSA