We've made several changes to our bench of longs and shorts on the Consumer Staples Ideas list.

Current longs are WWAV, DEO and THS

Current shorts are BNNY, K and HAIN

Changes to the long and short bench include:

- Adding MO and PM to the short bench

- Adding STZ to the long bench

- Removing RAI from the long bench

- Adding WFM, TFM and BDBD to the long bench

- Adding MON to the short bench

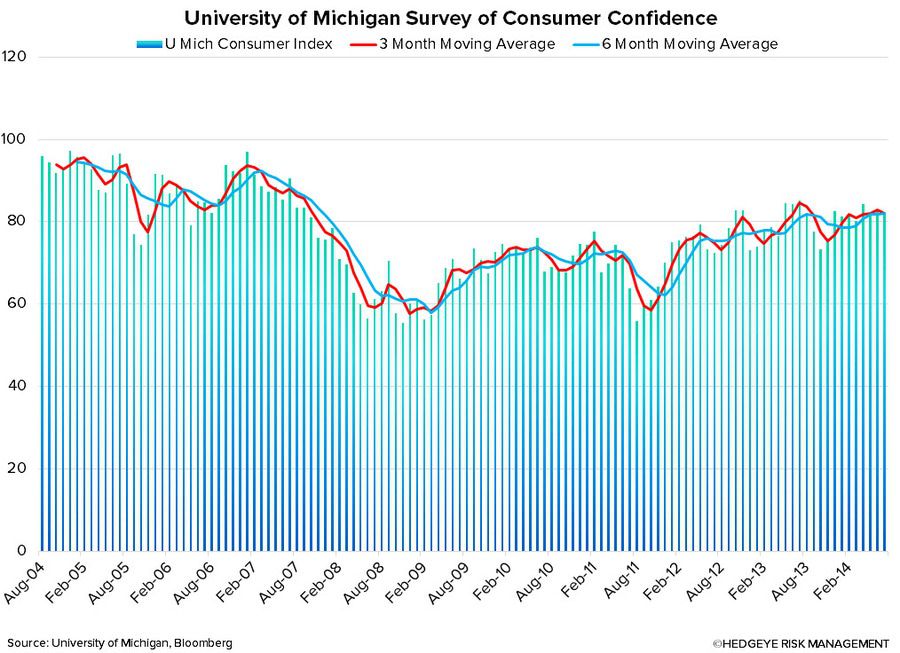

Mixed Consumer Picture

Today Bloomberg reported that the Consumer Comfort Index climbed to a five-week high on the back of an improving labor market. Two days ago the Conference Board reported that their sentiment gauge registered a seven-year high, saying that “Americans are finding more reasons to be upbeat about their prospects for the rest of the year as recent reports pointed to a pickup in the job market and stock prices advanced to records.”

There are no major changes in recent trends across the consumer staples space:

- U.S. packaged food sales were relatively flat in early August with salty snacks and chocolate leading the way, according to IRI data. On the downside, cold cereal and soup continue to lead the category losers. (short K)

- Carbonated beverages are lagging spirits trends.

- M&A is driving valuations in the food and beverage space to unwarranted levels. When will the contagion spread to the household product space? (long DEO)

- Private label is taking incremental share in household products.

- Organic continues to be a category of significant growth. Private label also continues to make inroads into the organic space. (long WWAV, THS)

Feel free to email or call with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst