INITIAL CLAIMS

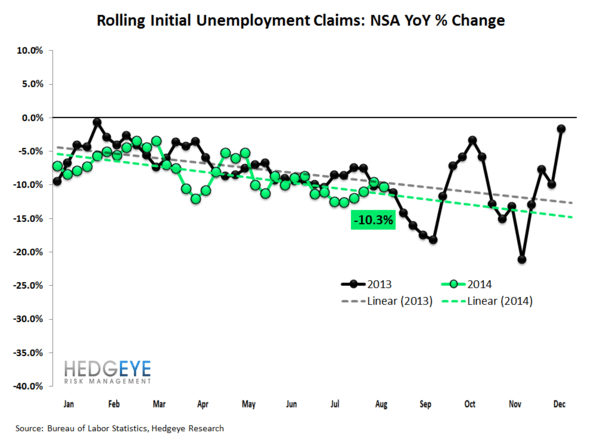

THE DATA: The high-frequency labor market data remains strong with Initial claims registering their 14th consecutive week of -10% YoY improvement on a rolling NSA basis. Headline claims declined -1K to +298K vs last week’s revised number with rolling claims falling -1.25K WoW to 299.75K.

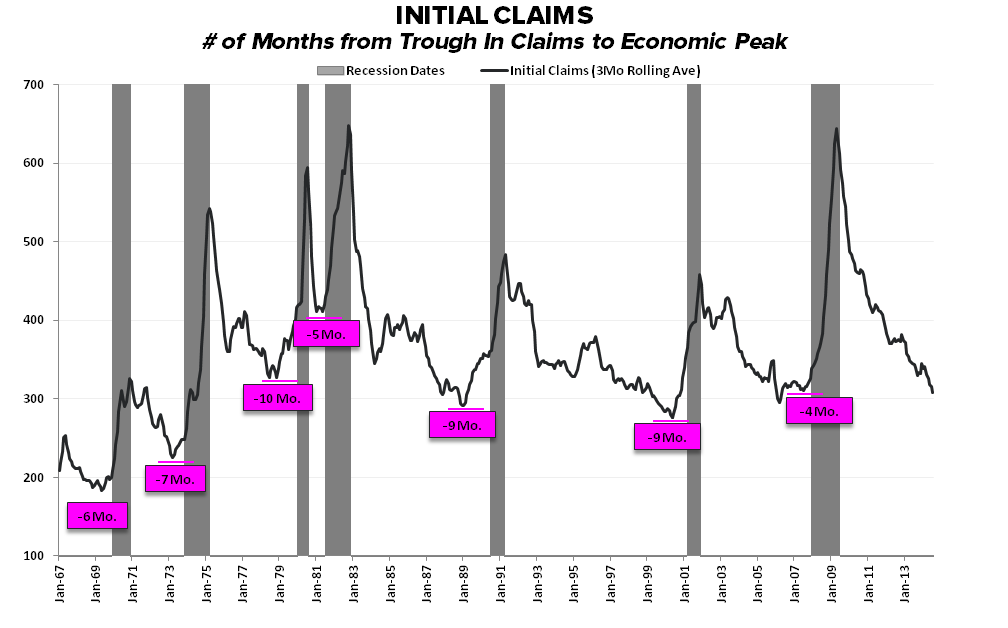

THE CYCLE: As we’ve highlighted, when initial claims (rolling, SA) have reached their current level, historically, the broader market index (S&P 500) has gone on to advance for another 12-18 months.

Further, our profiling of the last 7 economic cycles shows initial claims have served as a top leading indicator - reaching trough levels ~7 months ahead of the peak in the economic cycle. See our previous note for a more detailed discussion >> PATIENCE OR PENURY: THE JOBLESS, WAGE-LESS, INVESTMENT-LESS RECOVERY?

No cycle is the same, but historical cycle precedents and the ongoing improvement in the claims data suggests the peak in the current economic cycle is not immediately imminent.

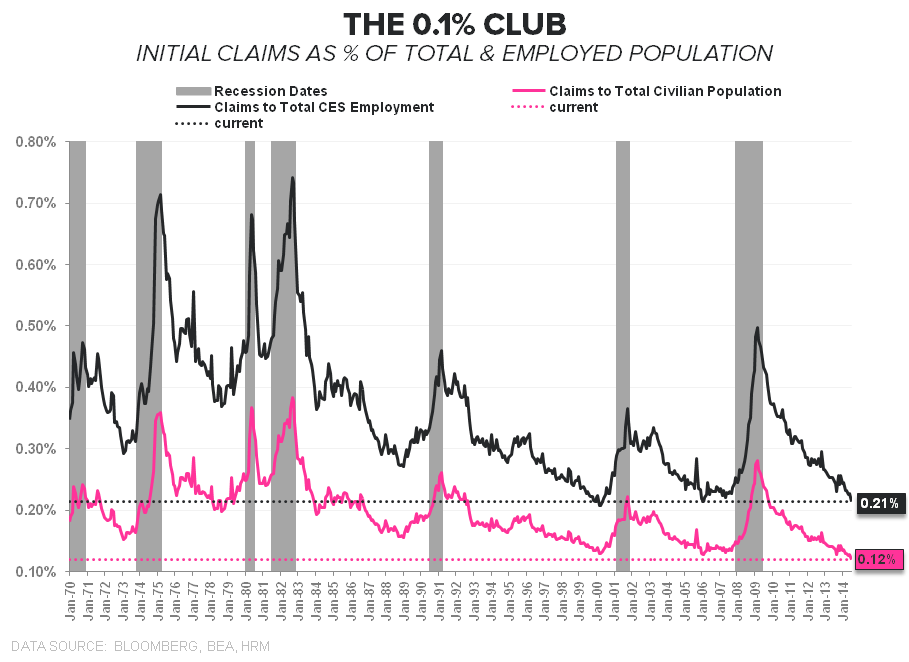

THE UNFORTUNATE FEW: Meanwhile, the unfortunate fraction that is the recently fired as a percent of both the total and employed populations continues to make lower lows. At present just 0.12% of the civilian population is recently unemployed – an all-time low.

In isolation, the claims data remains supportive of a positive NFP number. Of course, there’s two inputs into the net Hires equation (hirings less firings) and with employment still middling at the ~200K/mo level in the face of ongoing improvement in the claims data, we continue to largely fire on one labor market cylinder.

source: Hedgeye Financials

2Q14 GDP (1st Revision): Net Exports Drive the Non-Event 1st Revision

The positive revision to the trade balance drove the bulk of the upside revision to 2Q GDP. No big surprises or much in terms of investible takeaways from this morning’s release - below we summarily highlight the preliminary data. The impact of the 1st revision can be seen on the far right column in the table.

Headline: Positive +0.2% revision, taking real GDP to 4.2% QoQ SAAR from 4.0%. The inflation estimate ticked higher by 0.1%, so the revision was a function of higher ‘growth’ estimates – principally, a positive revision to NX.

C + I + G + NX: The positive revision to net exports supported most of the upside in the headline increase. The GDP contribution from NX was revised higher by 0.18 with “G” down small, “I” up modestly, and “C” unchanged.

- Consumption: Aggregate “C” was unrevised with a downward revision to Nondurables balancing modest positive revisions to Durables and Services.

- Investment: Downward revision to inventories offset by a sizeable positive revision to Nonresidential Investment

- Trade Balance: the confluence of a 0.6% revision to Export growth and a -0.7% revision to Import growth drove the positive revision to NX

Real Final Sales (GDP less Inventory Change): grew +2.8% QoQ….revised +0.5%

Real Final Sales to Domestic Purchasers (GDP less exports less inventory change): This is arguably the best read on overall domestic, private sector demand: grew +3.1% QoQ …revised +1.0%

Christian B. Drake

@HedgeyeUSA