Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume

*Note - to maintain cross-metric comparability, the purchase applications index shown in the table below represents the monthly average as opposed to the most recent weekly data point

Today's Focus: MBA Mortgage Applications

The Mortgage Bankers Association today released its weekly mortgage applications survey data for the week ended August 22nd.

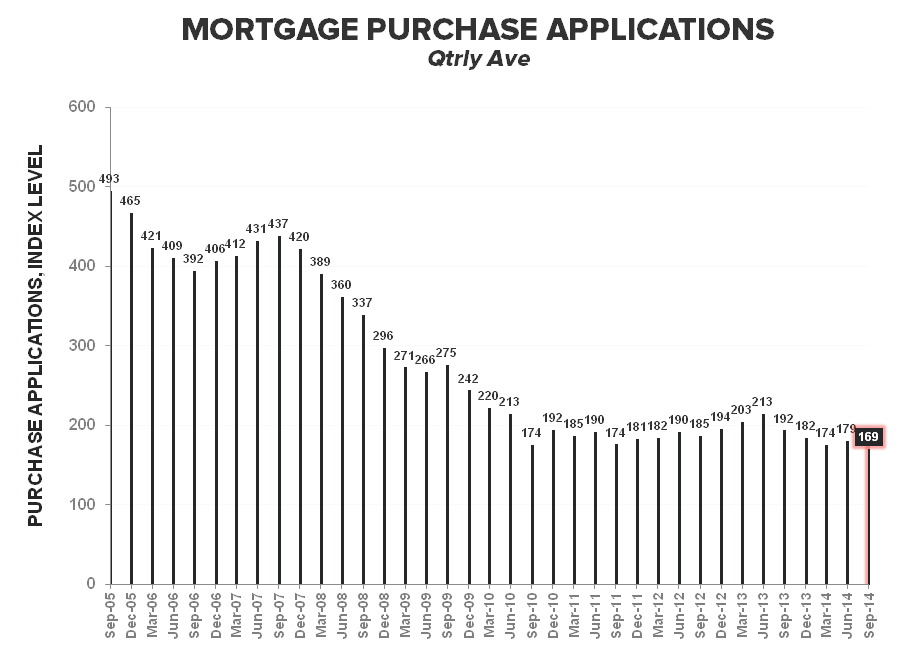

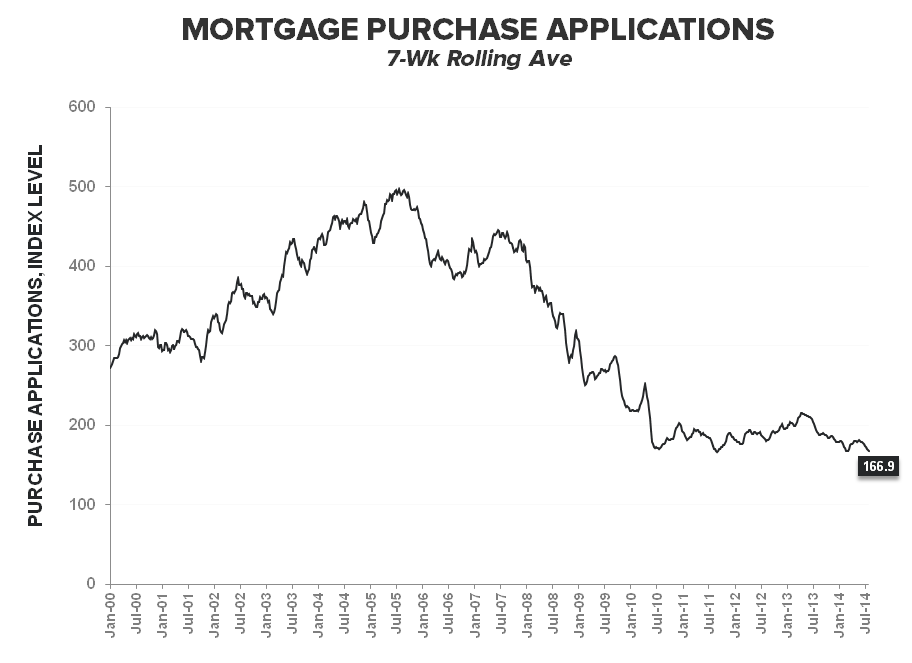

A 2.6% increase in purchase activity supported the rise in the composite index in the latest week but the gain was largely hollow with the purchase index holding below the 170-level for a 7th consecutive week – the 1st such occurrence since April of 1995

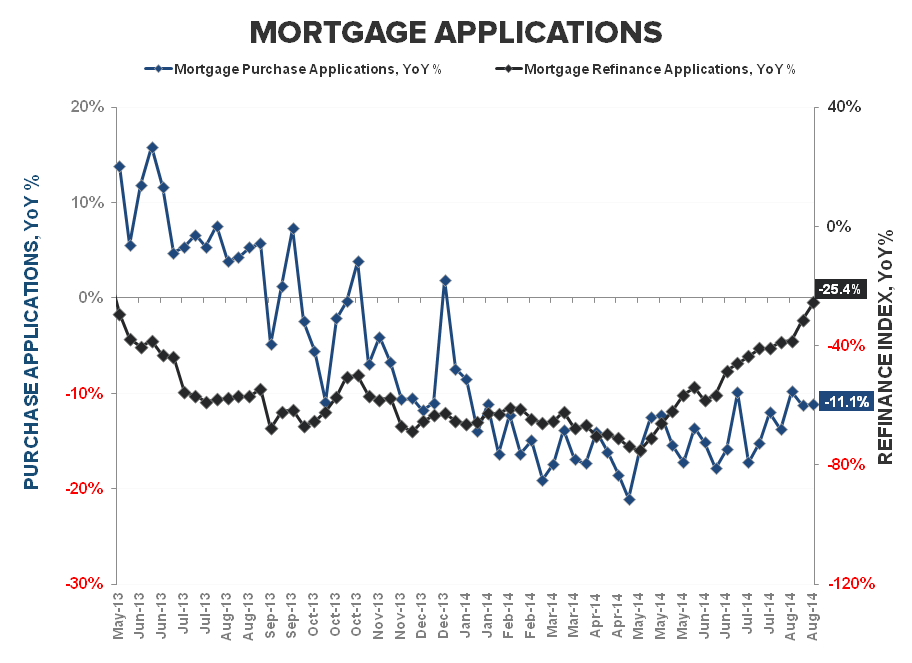

- 7 Week Slump: After 3 weeks of decline, Purchase demand rose +2.6% in the latest week, taking the index to 168.4. This marks the 7th consecutive week below the 170-level on the index – the longest such soft streak since April ’95. Purchase demand is currently running -5.8% QoQ and tracking at its lowest level since 2Q95.

- Refi & Rates: Refinance activity increased for a 2nd straight week, rising +2.8% sequentially alongside another tick lower in the 30Y FRM contract to 4.28%. Rates have declined -8bps in the last two weeks and currently sit just north of the lowest level since May of last year. Refi activity remains down -25% YoY (vs -31% last week) but continues to improve as we traverse through the easiest 2013 comps.

Cash sales remain elevated and the regulation-catalyzed shift in the origination channel may be a challenge to intertemporal reliability and dampening reported demand as measured by the MBA survey, but the broader takeaway remains unchanged:

Multi-decade lows in purchase demand (modestly distorted or not) is not the stuff accelerating housing recoveries are made of. We remain inclined to maintain our bearish view on the housing complex until the slope of HPI deceleration inflects.

About MBA Mortgage Applications:

The Mortgage Bankers’ Association’s mortgage applications index covers more than 75% of mortgage applications originated through retail and consumer direct channels. It does not include loans delivered through wholesale broker and correspondent channels. The MBA mortgage purchase applications index is considered a leading indicator of single-family home sales and construction. Moreover, it is the only housing index that is released on a weekly basis.

Frequency:

The MBA Purchase Apps index is released every Wednesday morning at 7 am EST.

Joshua Steiner, CFA

Christian B. Drake