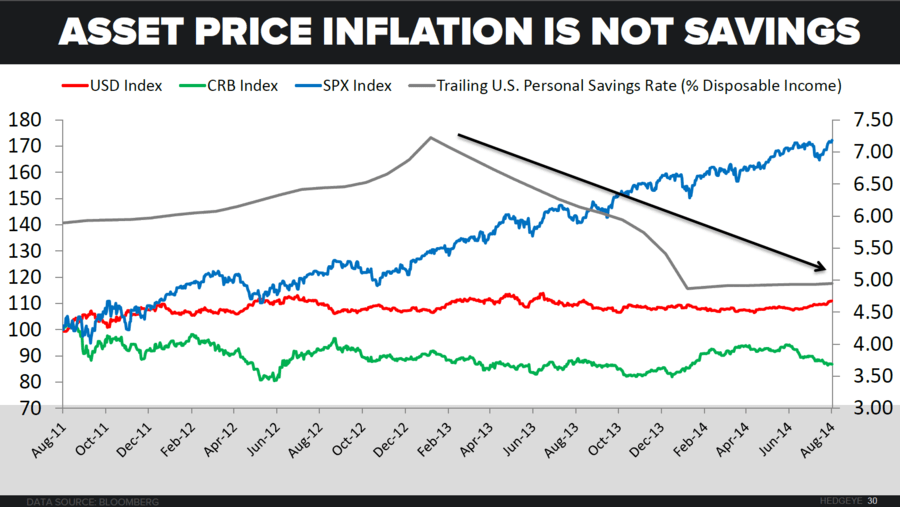

As you can see in the Chart of The Day (pg 30 in our current Macro Themes slide deck – if you’d like a copy, ping sales@Hedgeye.com), the US Personal Savings Rate (% of Disposable Income) has been falling for the past 3 years (as the stock market makes new highs).