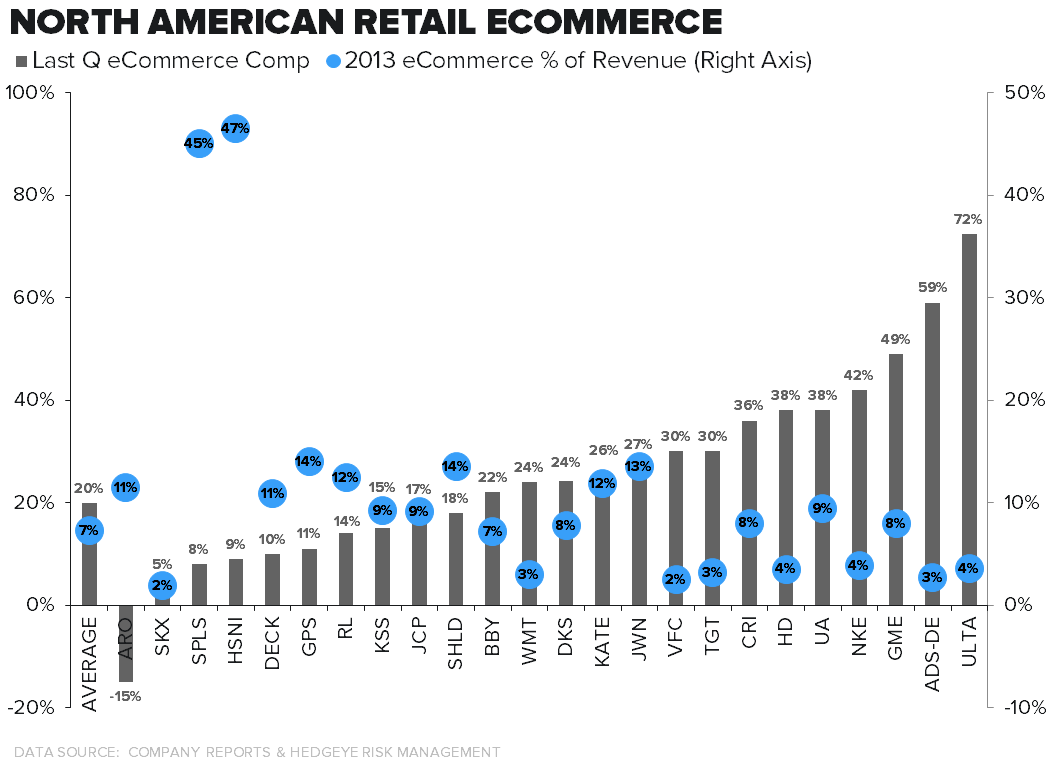

Listening to a full quarter’s worth of conference calls might lead one to think that e-commerce is the savior to everyone’s business. It’s not. Here’s a visual that might help contextualize e-commerce trends by retailer. On the left axis we show e-commerce comp by retailer (columns). There all on there – except those that don’t disclose data (i.e. Macy’s). The right axis shows e-commerce sales as a percent of total for each company (represented as circles). A few takeaways…

1) E-commerce represents about 7% of sales for retailers in aggregate, and the group put up a collective 20% dot.com comp this quarter – or about 140bp in total growth. This accounts for about half of the 2.6% average revenue growth for the group.

2) It’s impossible to miss that 3 of the top 5 growth rates are Athletic brands. Yes, Nike and Adidas have an embarrassingly low e-commerce penetration rate of 3-4%, which is a third of what we see at brands like KATE and RL. But there’s no denying that these brands are stepping up efforts to go direct to consumer. Can’t be bullish for Foot Locker.

3) Who would have thunk that the highest e-commerce penetration rates among the more traditional retailers is GPS and SHLD, which are topping out at 14%. They also have among the lower dot.com growth rates in the quarter. GPS is particularly noteworthy at 11%.

4) Rounding out the bottom with e-commerce penetration – i.e. worst execution but biggest opportunity – are SKX, VFC, WMT and TGT.