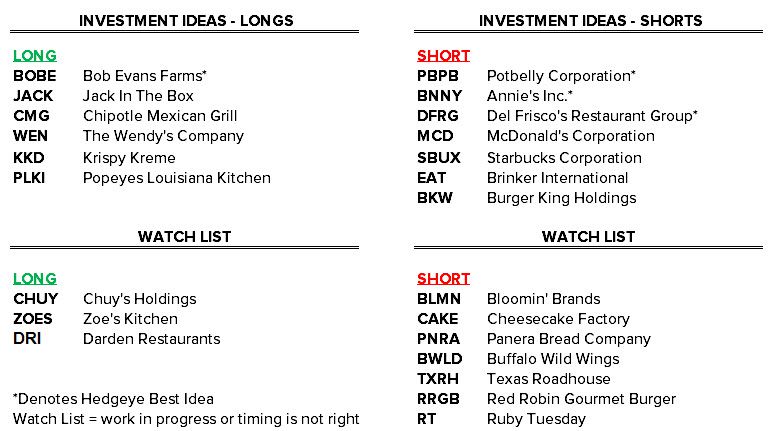

We are adding BKW to our Investment Ideas list as a short.

The surge in BKW's stock following the deal to buy THI makes the stock safe to short for many reasons. Additionally, we see significant risks to the combined company once the deal is completed. To be fair, Warren Buffett's halo is on the deal, but we have reason to believe this halo will tarnish.

We have several concerns with the deal, including:

- Levering up to pay a premium for a slow growth CDA company

- The lack of synergies with the transaction; in fact, costs will accelerate to jumpstart unit growth

- We doubt the merger will accelerate the growth of THI globally

- The two companies have fundamentally different views on franchising

- The Burger King franchisee base is weak and getting weaker by the day

- BKW is likely to miss 3Q14 estimates, including USA and CDA comp expectations

- The social media backlash, on both ends of the spectrum, to this transaction cannot be underestimated

- The conference call announcing the deal was far from impressive; in fact, it was rather discouraging

- The transaction is dilutive to current shareholders

- Current valuation is unwarranted

Our thoughts about the conference call Q&A:

Q: How much overlap is there between these two companies?

- Planning on managing the two brands independently of one another

- No plans to mix products or do co-branding

- The real driver is growth -- the potential to take THI global

Hedgeye -- On the surface this appears to be a positive, but we're not buying it. It's a matter of time before they try to combine products, especially coffee. Remember, Seattle's Best has failed to help BKW's breakfast business. In addition, we fail to see how merging two companies that have distinctly different views on franchising will help accelerate growth. The fact remains that Tim Hortons hardly has any brand awareness outside Canada and select parts of the U.S.

Q: Tax rate of the effective company?

- Don't expect the tax rate to change materially

Hedgeye -- Then why do the deal? At best this statement from management is disingenuous. In Canada, the corporate rate is about 15% compared with 35% in the U.S. More importantly, Canadian citizenship will allow the new company more opportunities to use various accounting and business “schemes” to shift profits north of the border and out of the reach of the IRS.

Q: What are the synergies between the two companies? Are they quantifiable? Timing?

- Transaction is not about synergies, it is about growth

- The priority is how quickly they can enter new markets and win in the U.S.

- They will be able to leverage BKW's infrastructure in the U.S.

Hedgeye -- Again, why do the deal? What BKW infrastructure are they referring to? The BKW franchisee base is suffering financially and doesn't quite mesh with THI's "mom and pop" franchise model.

Q: Any immediate feedback from franchisees on either side?

- Franchisees understand the purpose of the deal

Hedgeye -- The franchisees don't have a say in the deal!

Call or email with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst