NOTE SUMMARY

- Hedgeye Pandora User Survey: We surveyed 20,000 people in the US to determine Pandora’s user penetration and runway. We filtered the data down to roughly 14,000 users where demographic data was available. The most surprising takeaway is the number of P's duplicate accounts, which we estimate at over 50% of its total registered accounts.

- The User Growth Runway is Shorter Than We Thought: After backing out duplicate accounts, we estimate that P has penetrated 53% of the US adult internet population. More importantly, the majority of its unpenetrated TAM are adults over 45 year old, which will be tougher to penetrate and monetize. Further, we estimate the teenage cohort is over 70% penetrated.

- Declining Users/Hours in the Intermediate Future?: P has historical retention issues; more so than its duplicate accounts could explain. P's limited runway for new user growth may not be able to compensate for its churn much longer. Declining users is a very real possibility, and may occur as early as 2015.

- Sell-Through is the Bigger Question: Even if users/hours decline, P can still generate revenue growth by improving sell-through rates of its ad inventory. The question is how much of this opportunity lies with improving sell-through rates in the major ad markets vs. the minor ones. Answering this question is the next leg of our analysis; stay tuned.

HEDGEYE PANDORA USER SURVEY

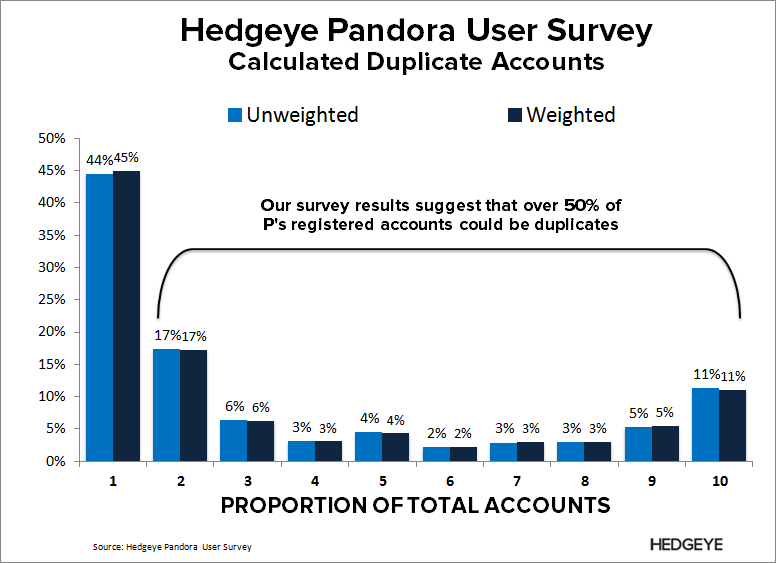

We ran a single-question poll using Google Consumer Surveys: "How many Pandora Internet Radio accounts have you ever created for your own use (Unique Usernames/Log-Ins)”?. The purpose of this question was to determine P's actual penetration levels, and the impact that users with multiple accounts had on P's registered user metrics.

We surveyed 20,000 people in the US; we then filtered the data down to 13,899 responses where demographic data was available (Google inferred). We present the data both as reported (unweighted), and weighted to represent the US Internet population.

At face value, the results are don't appear too surprising. But the total number of duplicate accounts is staggering.

- Penetration skews younger, 76% of 18-34 year olds have P accounts

- Most users only have one Pandora account (75%)

- The remaining 25% of users with multiple accounts are responsible for roughly 55% of P's total registered accounts.

While the duplicate percentage may seem too high to make sense, remember that P has over 250M registered accounts, which by most external estimates is almost the same size of the entire US population accessing the internet.

THE USER GROWTH RUNWAY IS SHORTER THAN WE THOUGHT

After backing out duplicates, and marrying the survey results with Census data, we estimate that Pandora is roughly 54% penetrated into the US Adult Internet Population. While that may sound like a lot of runway, the demographics of its remaining addressable market skew much older, which will make incremental user growth more challenging.

- Roughly half (49%) of the total number of survey respondents that didn't have a Pandora account were over the age of 55; roughly 73% were over 45.

- When comparing our survey against demographic internet data from the Census, we estimate that 66% of P's remaining US TAM among adults are over 45 years old.

We haven't discussed teenagers yet, which are an inherently easier group to penetrate. However, we estimate that P has already penetrated a considerable portion of this segment. The table below details our analysis here. In short, P has likely penetrated over 70% of the non-adult US internet user base.

DECLINING USERS/RUNWAY IN THE INTERMEDIATE FUTURE?

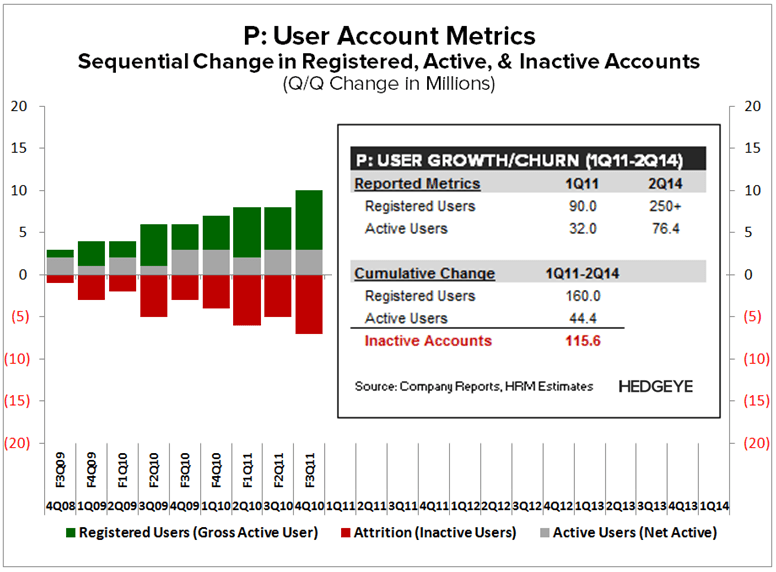

We have previously identified that P has historical retention issues, which we detail in the chart below. Over the last 3.5 years, P has added more than 160M registered accounts, yet only grew active users by 44M, suggesting total churn of at least 116M accounts, or 72% of its gross account gains during this period.

We do not have enough data to explicitly calculate its quarterly churn rate after 1Q11. However, we estimate using a rough back-of-envelope calculation that quarterly attrition over the past 3.5 years has averaged somewhere in the mid to high-teens as a percentage of its active users.

Currently, P has 76.4M active users as of 2Q14. If we a assume mid- to high-teen churn rate, then the company would need to sustain a run-rate of gross new quarterly account adds of 11M-13M to maintain its active user base. Even If that run-rate was possible over the long-run, and P could penetrate every internet user in the US, we estimate that P would exhaust its unpenetrated TAM within 7-10 quarters.

In a more likely scenario, we expect gross new account adds to slow given the high concentration of older users within P's unpenetrated TAM, which should lead to y/y declines in user and/or listener hour growth sometime in 2015.

SELL-THROUGH IS THE BIGGER QUESTION

We want to be extremely clear: Declining users and/or hours does not mean that revenues will decline. Even if users/hours decline, P can still generate revenue growth by improving sell-through rates on its ad inventory, which remains below 50% of total hours according to management.

The question is how much of this opportunity lies with improving sell-through rates in the major advertising markets vs. the minor ones (e.g. New York City vs. Topeka).

Put another way, if users in New York City are already receiving peak ad load (sell-through rate), then losing those users would likely outweigh any benefit of improving sell-through rates in Topeka.

Answering this question is the next leg of our analysis; stay tuned. In the interim, let us know if you have any questions, or would like to discuss in more detail

Hesham Shaaban, CFA

@HedgeyeInternet