TODAY’S S&P 500 SET-UP – August 26, 2014

As we look at today's setup for the S&P 500, the range is 35 points or 1.15% downside to 1975 and 0.60% upside to 2010.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.88 from 1.88

- VIX closed at 11.7 1 day percent change of 2.01%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: ICSC weekly sales

- 8:30am: Durable Goods, July, est. 8% (pr 0.7%, rev 1.7%)

- 8:55am: Redbook weekly sales

- 9am: FHFA House Price Index m/m, June, est. 0.3% (prior 0.4%)

- 9am: S&P/Case Shiller 20-City m/m SA, June, est. 0.0% (pr -0.31%)

- 10am: Consumer Confidence Index, Aug., est. 89 (prior 90.9)

- 10am: Richmond Fed Manufacturing Index, Aug., est. 6 (prior 7)

- 11:30am: U.S. to sell $50b 4W bills

- 1:00pm: U.S. to sell $29b 2Y notes

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- President Obama at American Legion convention, Charlotte, N.C.

- Senate, House out on August recess

- U.S. ELECTION WRAP: Primaries in Ariz., Fla.; Curtis Diary

WHAT TO WATCH:

- Buffett said to help finance Burger King’s tax-saving deal

- Ackman gains 30% in 2014 with Burger King, Herbalife wagers

- Muni assets said to be excluded for U.S. bank liquidity rule

- GM’s Chevrolet, Buick achieve sole gains in annual auto survey

- GMO crop curbs overturned by judge in Hawaii: WSJ

- Telefonica board said to discuss improving GVT bid this week

- U.S. surveillance planes fly over Syria: AP sources

- Putin set to meet Poroshenko as Ukraine border tension grows

AM EARNS

- Bank of Montreal (BMO CN) 7am, C$1.66 - Preview

- Bank of Nova Scotia (BNS CN) 6am, C$1.41 - Preview

- Best Buy (BBY) 7am, $0.31 - Preview

- DSW (DSW) 7am, $0.32

- Movado (MOV) 7am, $0.54

- Sanderson Farms (SAFM) 6:30am, $3.80

- Tech Data (TECD) 6am, $0.77

PM EARNS

- Analog Devices (ADI) 4:04pm, $0.63

- Aruba Networks (ARUN) 4:05pm, $0.23

- Bob Evans Farms (BOBE) 4:01pm, $0.10

- Heico (HEI) 4:23pm, $0.44

- Nimble Storage (NMBL) 4:05pm, $(0.16)

- Smith & Wesson (SWHC) 4:05pm, $0.25

- Solera (SLH) 4:08pm, $0.80

- TiVo (TIVO) 4:01pm, $0.07

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Hedge Fund Citrine Picks Zinc, Nickel as Best Base Metal Wagers

- Iron Ore Risks Extending Drop as Price Falls to Lowest Since ‘12

- Brazil Coffee Output Set for Worst Slump Since 1965: Commodities

- Gold Climbs Most in Almost Three Weeks as Decline Spurs Buying

- WTI Trades Near Seven-Month Low Before Supply Data; Brent Steady

- China’s 2014 Copper Imports to Sustain Last Yr’s Pace: Antaike

- Sanderson Profit Disappoints After It Misses Poultry Forecast

- Turkey to Belarus Gold Reserves Said by IMF to Decrease in July

- Raw Sugar Imports Rising 29% in Indonesia as Drinks Demand Booms

- Soybean Futures Drop for Second Day to Lowest Since Sept. 2010

- China Requires U.S. Govt GMO Certification for DDGS: Cngrain.com

- Corn Futures Seen Extending Decline to Year-End, UBS Says

- Wells Fargo Sees Energy Rebound as Crude, Gas Weakness Temporary

- Billionaires Lose Wealth as India Mine Permits Ruled Illegal

- Nexen’s Buzzard Field Said Not to Have Restarted as Planned

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

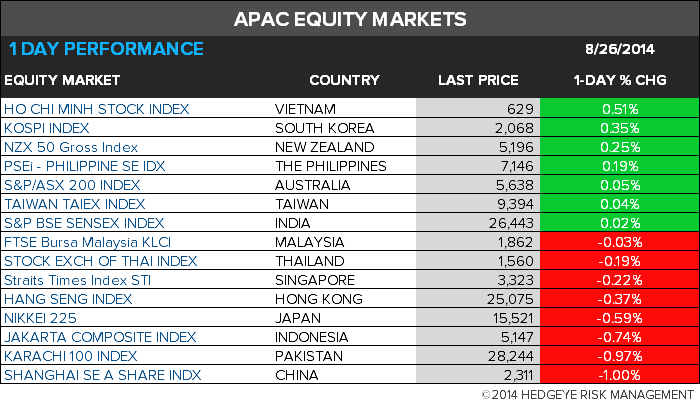

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team