TODAY’S S&P 500 SET-UP – August 25, 2014

As we look at today's setup for the S&P 500, the range is 30 points or 1.08% downside to 1967 and 0.43% upside to 1997.

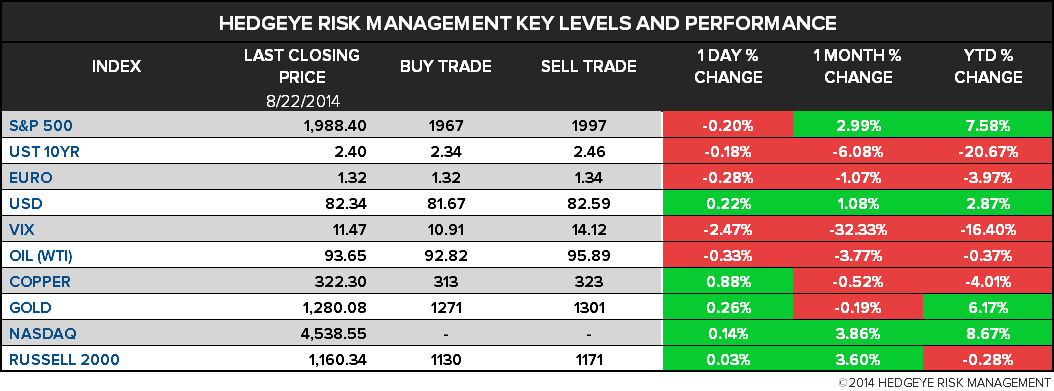

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.89 from 1.91

- VIX closed at 11.47 1 day percent change of -2.47%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Chicago Fed Natl, July, est. 0.20 (prior 0.12)

- 9:45am: Markit U.S. Composite PMI, Aug. prelim (prior 60.6)

- 9:45am: Markit U.S. Services PMI, est. 58.0 (prior 60.8)

- 10am: New Home Sales, July, est. 429k (prior 406k)

- 10:30am: Dallas Fed Mfg, Aug., est. 12.8 (prior 12.7)

- 11am: U.S. to announce plans for auction of 4W bills

- 11:30am: U.S. to sell $29b 3M bills, $24b 6M bills

GOVERNMENT:

- Senate, House out on August recess

- FCC deadline for comments on proposed Comcast-Time Warner Cable merger

- 1pm: Atlantic Council briefing on “Mexico’s Energy Reform: Ready to Launch” report

WHAT TO WATCH:

- Roche to buy InterMune for $8.3b, adding lung drug

- Roche said to have decided against bidding for rest of Chugai

- CME opens electronic futures trading after 4-hour delay

- Burger King mulls Tim Hortons deal in tax-saving Canada move

- Occidental talks to Mubadala on $3b asset, PIW reports

- Jackson Hole theme is labor markets can’t take higher rates

- Pershing, Valeant say Allergan investors demand mtg on deal

- Wal-Mart said to move India COO Mediratta to U.S. ops

- Advaxis, Merck enter clinical trial pact for cancer treatment

- Goldman’s new partner class unlikely to grow from 2012: WSJ

- California quake to cost insurers up to $1b, Eqecat says

- German business confidence drops for 4th month as risks rise

- China urges U.S. to halt close air surveillance

- Friends Life said to hire Goldman for sale of intl unit

EARNINGS:

- OSI Systems (OSIS) 8:30am, $1.17

- Prospect Capital (PSEC) 4pm, $0.32

- Qihoo 360 (QIHU) 5pm, $0.67

- Renren (RENN) 6pm, ($0.08)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Brent, WTI Oil Prices Reverse Decline as Libya Tensions Persist

- China Gold Imports Drop for Fifth Month on Weak Consumer Demand

- Speculators Lower Gold Bull Wagers on Rate Outlook: Commodities

- Soybeans Slump to Lowest Since 2010 as U.S. Crop Seen at Record

- CME Opens Electronic Trading on Futures After Four-Hour Delay

- Copper in New York Swings Near 3-Week High After Trading Delay

- Palm Oil Prices Seen Rebounding in 4Q on Demand, CIMB’s Ng Says

- Hedge Fund Crude Bets Tumble Amid Surging Global Supply: Energy

- Kurdish Oil Shipments From Turkey Said to Resume as Tanker Loads

- TOP Oil Market News: Brent Rebounds on Libya to Iraq; WTI Steady

- Rhodium Rally Pushes Price Past Platinum, Gold: Chart of the Day

- BNP Paribas Recommends Selling Oct. Singapore Fuel Oil Crack

- California Quake Crumples Buildings With Scores Injured in Napa

- Gold Falls as Dollar Advances on Fed Outlook; Silver Halts Drop

CURRENCIES

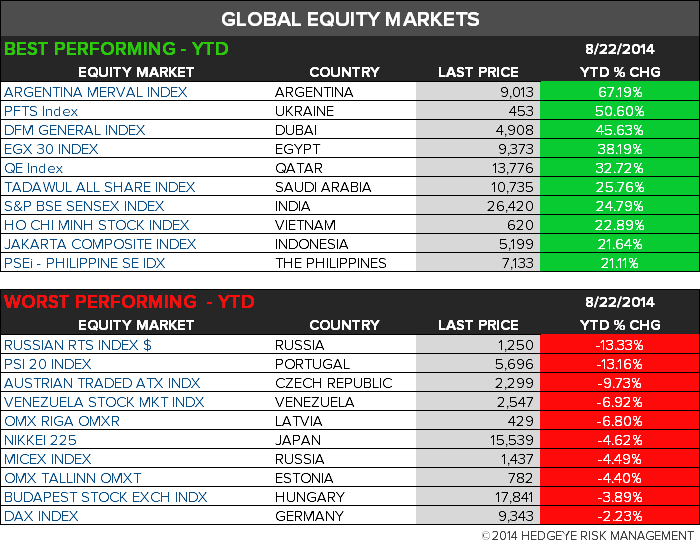

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

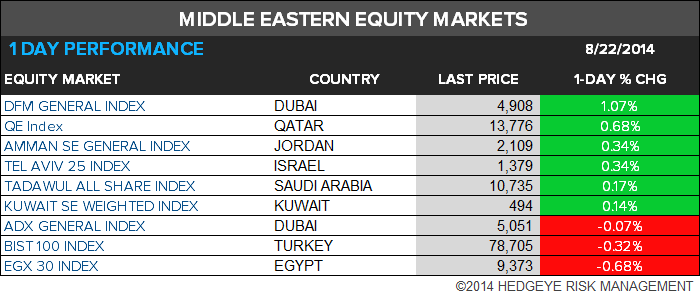

MIDDLE EAST

The Hedgeye Macro Team