HEDGEYE TV

Q&A: Keith Answers Questions From Subscribers

In this Q&A portion of Tuesday's Morning Macro Call, Hedgeye CEO Keith McCullough discusses the Fed's next move, the U.S. housing market, and his continued bullishness on bonds.

Two Chip Stocks Feeding on the Apple iPhone 6 Frenzy

Hedgeye semi analyst Craig Berger highlights two new chip suppliers riding the coattails of Apple’s highly anticipated iPhone 6.

CARTOON

Sitting Ducks?

Ain't No Hawk!

Think the Fed's going to suddenly strike a hawkish tone? Don't hold your breath.

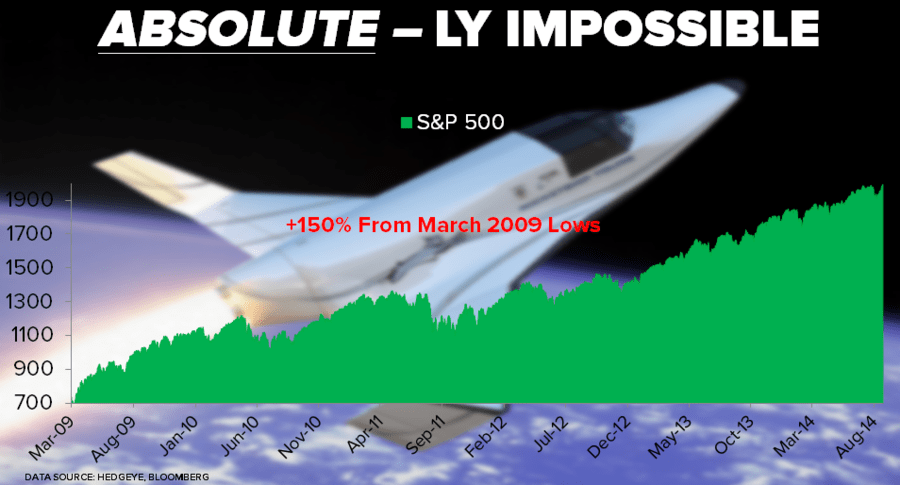

CHART

$SPY Up 150% Since 3/09 Lows

POLL

Buying the iPhone 6?

Shares of Apple are hitting record highs, fueled largely on investor optimism that iPhone 6 sales are going to be blockbuster.