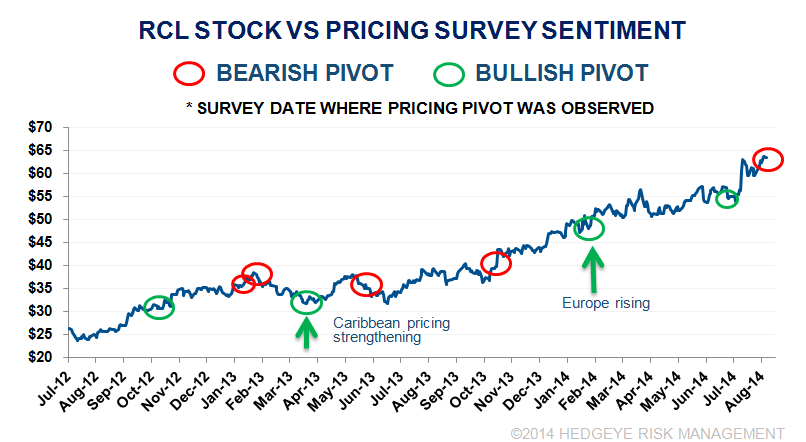

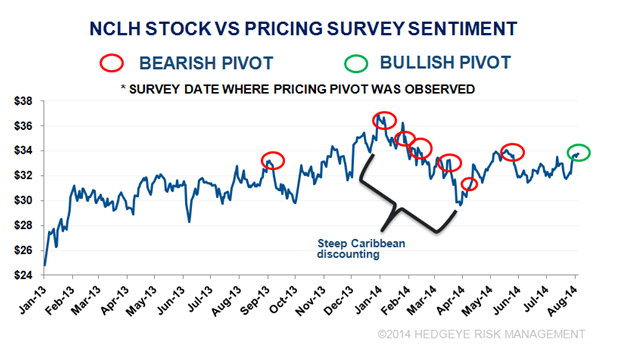

Some cracks in the RCL bullish thesis while more positive pivots for CCL and NCLH on the margin

CALL TO ACTION

Wall street darling RCL has seen little resistance this year. Quantum pricing looks good and up until now the RCL thesis looked bullet proof. However, our August survey revealed some discounting in the RC Caribbean itineraries. Stocks trade on the margin and the pivot here looks negative for RCL despite unabated strength in Europe.

On the other hand, the CCL and NCLH pivots look positive, on the margin. The August survey indicated slightly higher pricing for the Carnival brand pricing for FQ4 2014 and FQ1 2015. For NCLH, the Norwegian brand (through mostly Getaway) seems to be reflecting CEO Sheenan's promise of a 3% price increase.

We've been negative on NCLH, neutral on CCL, and positive on RCL. Given the survey results versus current sentiment, we could see the relative performance of the stocks reverse somewhat over the coming weeks.

SURVEY vs SENTIMENT

- CCL: Positive

- RCL: Negative

- NCLH: Positive

SURVEY METHODOLOGY

We track YoY and sequential pricing for 13,000 ship itineraries spanning across 8 geographic regions. We rely on sequential pricing trends (defined as how pricing has changed relative to pricing seen at the last time the company provided guidance) for price pivot signals.

SURVEY RESULTS

SUMMARY

Our pricing survey for mid-August suggests the RC brand underperformed in the Caribbean and for some Asia itineraries. Meanwhile, we saw a slight improvement for CCL and NCLH due to stronger pricing for the Carnival and Norwegian brands. European pricing, which is Q3 heavy, remained steady.

CCL

Caribbean pricing continues to be volatile but in mid-August, the Carnival brand showed higher pricing. In stark contrast, the other brands in the Caribbean fared poorly, particularly Princess.

Caribbean

- Carnival brand

- Sequential pricing rose slightly for FQ4 as well as for FQ1/FQ2 2015.

- On a YoY basis, FQ4 pricing is trending up in the mid-teens for the Eastern Caribbean itineraries and mid-single digit growth for the Western/Southern Caribbean itineraries.

- Princess/Holland America

- Pricing is significantly lagging behind. Princess, in particular, has been discounting aggressively for Caribbean and Western US itineraries for FQ4 2014 and FQ1 2015. Holland America pricing was a tad lower.

Europe

- Costa continues to be the shining light for CCL’s European business thanks to very easy comps. FQ4 pricing growth remains comfortably near 20%. 1H 2015 pricing comparisons will be a challenge if Costa does not raise prices. Pricing for the other brands were either flat or slightly higher.

Asia/Australia

- Pricing ticked up for Holland America and Princess itineraries.

South America

- Costa pricing for FQ4 moved modestly lower while 1H 2015 pricing was a tad higher

- Holland America/Princess pricing was unchanged for early 2015

RCL

Royal Caribbean brand pricing receded somewhat in mid-August in the Caribbean. However, that was offset by its pricing leadership in Europe.

Caribbean

- RC brand

- A bit of a surprise as sequential pricing turned south for many of the Royal Caribbean brand itineraries for FQ3 and FQ4. The discounting extends to Allure of the Seas and Oasis of the Seas.

- Excluding Quantum of the Seas, on a YoY basis, FQ3 pricing is trending down mid-single digits, while FQ4 pricing is down slightly.

- Quantum of the Seas pricing was steady as a rock

- Celebrity

- FQ4/FQ1 sequential pricing was steady but due to hard comps, YoY pricing is lower by high single digits.

- Pullmantur

- Pricing was steady for Q4 2014 but a challenging start to Q1 2015 due to more difficult comps

Europe

- August sustained the pricing momentum seen earlier in 2014. For the RC brand, FQ3 pricing is trending 20% YoY and slightly above 10% YoY for FQ4.

- Celebrity pricing increased sequentially for 2H 2014 with YoY pricing in the low double digits.

- After creeping higher for the previous two months, Anthem of the Seas pricing rose modestly in mid-August for May-October 2015 sailings.

- Pullmantur pricing slightly increased sequentially

Asia/Australia

- Pricing was generally weak for the RC brand while Celebrity is seeing pricing growth.

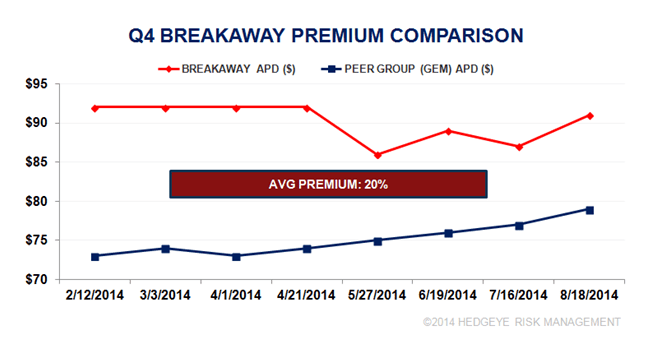

NCLH

NCL has been slumping for much of 2014 due to Caribbean overcapacity. But do pricing signals from mid-August suggest the beginning of an inflection point or a head fake?

Caribbean

- Still discounting in the Caribbean for FQ3 but the sequential cutting has tapered.

- Breakaway cut FQ3 prices to a new low of $91 per diem

- FQ4 pricing showed a 3% sequential price increased led by Getaway in the Nov/Dec months

- This is the 1st sequential price increase since we started tracking the data for FQ4

- FQ4 ship premiums rose for Breakaway and Getaway

- Q1 2015 pricing lower - as expected, due to difficult comps

- Q2 2015 up slightly

Europe

- Pricing was stable; few itineraries available

Hawaii

- Continues to be a struggle for the rest of the year

conclusion

CCL/NCLH outperformed while RCL was the laggard in August, at least relative to recent trends. The Caribbean has been a roller-coaster ride for the cruisers this summer as mixed brand pricing trends are the norm and we may see more volatility ahead. A trend or an outlier, only time will tell.

The good news is that Europe pricing remains quite robust for the rest of 2014 despite the significant global geopolitical turmoil. The question is whether it can be sustained into 2015. While it is super early, we're seeing mixed pricing there as well.

The Carnival brand is making strides in pricing thanks to ridiculously easy comps but it is not translating into higher prices for CCL's other brands. With earnings in one month, we look to September's survey for confirmation of these trends.

Though NCLH performed better in mid-August, we wait to see if it is indeed an inflection point. Remember, CEO Sheehan promised investors a 3% price increase across its fleet during its Q2 conference call. Among the big 3 operators, NCLH is most sensitive to the Caribbean/Bermuda market, and faces harder pricing headwinds in 1H 2015 along with no yield boost from a new ship until FQ4 2015.