Investment Company Institute Mutual Fund Data and ETF Money Flow:

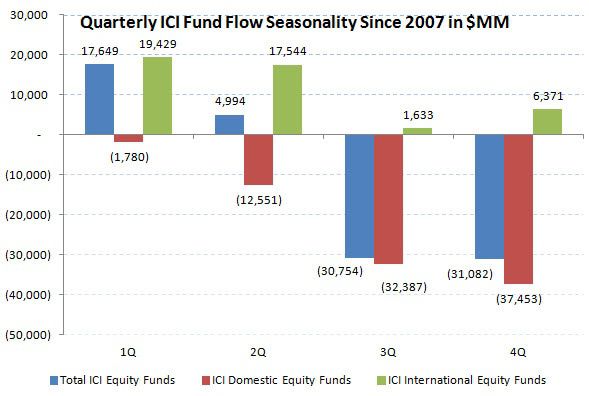

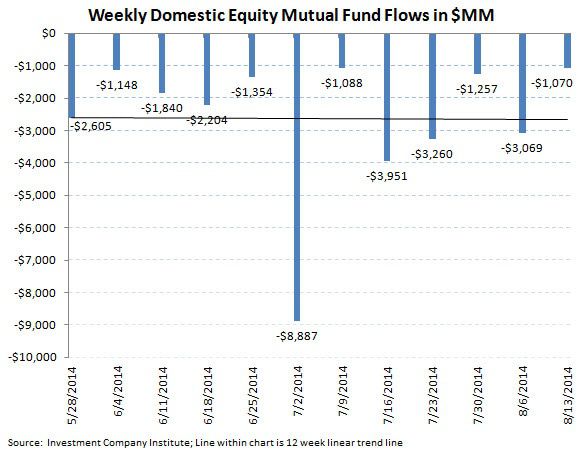

In the most recent 5 day period ending August 13th, taxable fixed income flows snapped back to positive territory, eking out a slight inflow of $519 million after the substantial panic outflow of over $8.0 billion the week prior. Intermediate term trends are still intact for taxable bonds with inflow in 25 of the past 27 weeks. Domestic stock funds conversely continue to struggle with another $1.0 billion being withdrawn by investors last week which make it 16 consecutive weeks of outflows with now over $40 billion lost in the category. We remind investors that looking back to 2007, that the average outflow sequence in domestic stock funds has averaged 40 weeks with over $113 billion on average drawn down, so the initial weakness in domestic stock funds could easily run through the rest of 2014 (and into 2015). The equity mutual fund channel is also entering the seasonally weakest part of the year (the fourth quarter), and we recommend that investors avoid Janus Capital (JNS) and T Rowe Price (TROW) with the most exposure to the U.S. stock funds (see our report on why TROW should underperform).

Total equity mutual funds put up a slight inflow in the most recent 5 day period ending August 13th with $225 million coming into the all stock category as reported by the Investment Company Institute. The composition of the inflow continued to be weighted towards International stock funds with $1.2 billion coming into the category offset by the ongoing 16 week redemption in domestic equity funds which totaled a $1.0 billion outflow last week. This draw down in domestic equity funds has now totaled a $40 billion outflow over the past 4 months. The running year-to-date weekly average for equity fund flow is now a $1.5 billion inflow, which is now well below the $3.0 billion weekly average inflow from 2013.

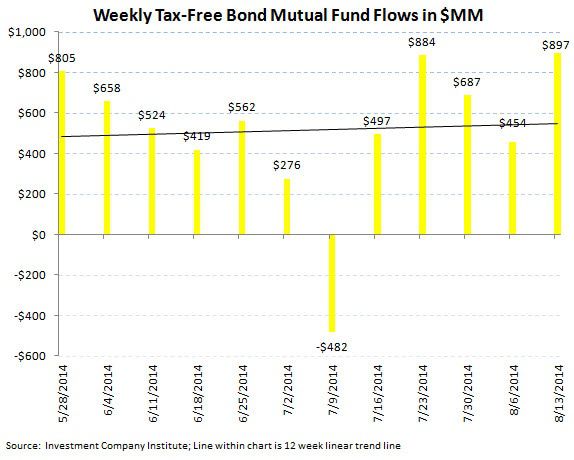

Fixed income mutual funds had another positive week of production with $1.8 billion coming into the asset class. The inflow into taxable products of $519 million made it 25 of 27 weeks with positive flow. Municipal or tax-free bond funds put up a $897 million inflow, making it 30 of 31 weeks with positive subscriptions. The 2014 weekly average for fixed income mutual funds now stands at a $1.8 billion weekly inflow, an improvement from 2013's weekly average outflow of $1.5 billion, but still a far cry from the $5.8 billion weekly average inflow from 2012 (our view of the blow off top in bond fund inflow).

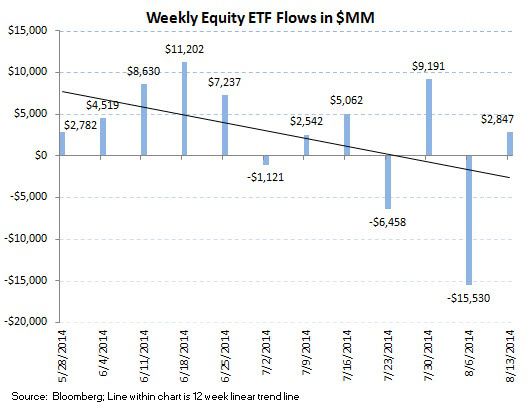

ETF results were broadly positive during the week with inflows into both equity funds and fixed income products. Equity ETFs put up a $2.8 billion subscription while fixed income ETFs put up a $2.6 billion inflow. The 2014 weekly averages are now a $1.2 billion weekly inflow for equity ETFs and a $939 million weekly inflow for fixed income ETFs.

The net of total equity mutual fund and ETF trends against total bond mutual fund and ETF flows totaled a negative $1.0 billion spread for the week ($3.0 billion of total equity inflow versus the $4.1 billion inflow within fixed income; positive numbers imply greater money flow to stocks; negative numbers imply greater money flow to bonds). The 52 week moving average has been $4.0 billion (more positive money flow to equities), with a 52 week high of $31.0 billion (more positive money flow to equities) and a 52 week low of -$37.5 billion (negative numbers imply more positive money flow to bonds for the week). The 52 week moving average chart displays the declining demand for all equity products (funds and ETFs) for the safety and security of fixed income.

Mutual fund flow data is collected weekly from the Investment Company Institute (ICI) and represents a survey of 95% of the investment management industry's mutual fund assets. Mutual fund data largely reflects the actions of retail investors. Exchange traded fund (ETF) information is extracted from Bloomberg and is matched to the same weekly reporting schedule as the ICI mutual fund data. According to industry leader Blackrock (BLK), U.S. ETF participation is 60% institutional investors and 40% retail investors.

Most Recent 12 Week Flow in Millions by Mutual Fund Product:

Most Recent 12 Week Flow Within Equity and Fixed Income Exchange Traded Funds:

Net Results:

The net of total equity mutual fund and ETF trends against total bond mutual fund and ETF flows totaled a negative $1.0 billion spread for the week ($3.0 billion of total equity inflow versus the $4.1 billion inflow within fixed income; positive numbers imply greater money flow to stocks; negative numbers imply greater money flow to bonds). The 52 week moving average has been $4.0 billion (more positive money flow to equities), with a 52 week high of $31.0 billion (more positive money flow to equities) and a 52 week low of -$37.5 billion (negative numbers imply more positive money flow to bonds for the week). The 52 week moving average chart displays the declining demand for all equity products (funds and ETFs) for the safety and security of fixed income.

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA