This note was originally published at 8am on August 07, 2014 for Hedgeye subscribers.

“We are taking a greater chance of having another crash at a time when the world is less capable of bearing the cost.”

-Raghuram Rajan

Crash? Yep. My man Dr. Raj doesn’t consider it improbable. Do you? The aforementioned quote comes from an interview the former Chief Economist of the IMF (2003-2006) and now Governor of the Reserve Bank of India just gave to the Central Banking Journal.

“Investors are counting on easy money – they put the trades on even though they know what will happen as everyone attempts to exit positions at the same time… there will be major market volatility if that occurs.”

I can assure you that “everyone” has not attempted to get out of the US stock market, yet. Just think, all we needed was a 2% down day (and a -3.5% correction from the all-time bubble highs), and volatility (VIX) ripped +65%! That’s called some wicked asymmetry.

Back to the Global Macro Grind…

I have no love lost for those who think that they can centrally plan things like gravity, economic cycles, etc. But if I had to pick one modern central planner to help me run money, it would be Dr. Raj. When it comes to real-time interconnected market risk, sorry Janet, but you wouldn’t make it past the first interview at a performance based fund.

Not only did Rajan tell linear-economist Larry Summers to go flower himself circa 2006 (Summers called Rajan’s views of market risks “misguided”), but he’s taken India on a path that American, European, and Japanese bureaucrats seemingly do not have the spine to traverse – that of raising interest rates in order to tone down the real cost of living (inflation).

India’s stock market (one of our favorite long ideas in 2014 – the Wisdom Tree India Earnings Fund (EPI) in Real-Time Alerts) not only took the rate hikes and inflation fighting policy from Dr. Raj in stride, they celebrated them. India’s BSE Sensex is up another +0.4% this morning to +23.2% for the YTD as these wacky things called investment and capex cycle expectations in India take hold.

Raising rates?

Sadly, if we’re right on both US Housing and GDP continuing to slow here in Q3, there isn’t a chance on this side of central planning hell that Janet Yellen is going to raise interest rates in the 1st half of 2015.

Being the bear on both US growth and rates this year, I get a lot of questions on Fed timing. I spent all of yesterday seeing Institutional Investors in NYC (8 meetings) and by the end of the day I came to the realization that the biggest risks to our current views are:

- We aren’t bearish enough on US growth

- We aren’t bullish enough on long-term Treasuries

Sounds a little crashy, but just fyi, markets do crash after making all-time bubble highs on no-volume.

Again, what I just wrote is that the risk to our current view is that we’re not bearish enough on the US stock market. Since we don’t do the “year-end bonus-target” thing for stock and bond market levels, here’s that current view:

- US Treasury 10yr Yield tests 2.21-2.41%

- SP500 corrects towards 1829

Yeah, on that 2.41% level for the 10yr, I know. What a leap that forecast is with the 10yr at 2.45% this morning! As my friends from Thunder Bay would say though, “the thing of it is” we’ve been looking for 2.41% since the 10yr was at 3%.

On the SP500 though, my current views are finally shifting to the bear side.

As most of you who have been following my team and my levels know, I have been more focused on having you sell the Russell 2000 than the SP500 YTD, primarily because the SP500 has many more slow-growth #YieldChasing components that I like(d).

Provided that the SP500 remains bearish on my intermediate-term TREND signal (1930 resistance), I see my long-term TAIL risk line of 1829 support as probable. What does probable mean in risk management speak? Well, it doesn’t mean improbable.

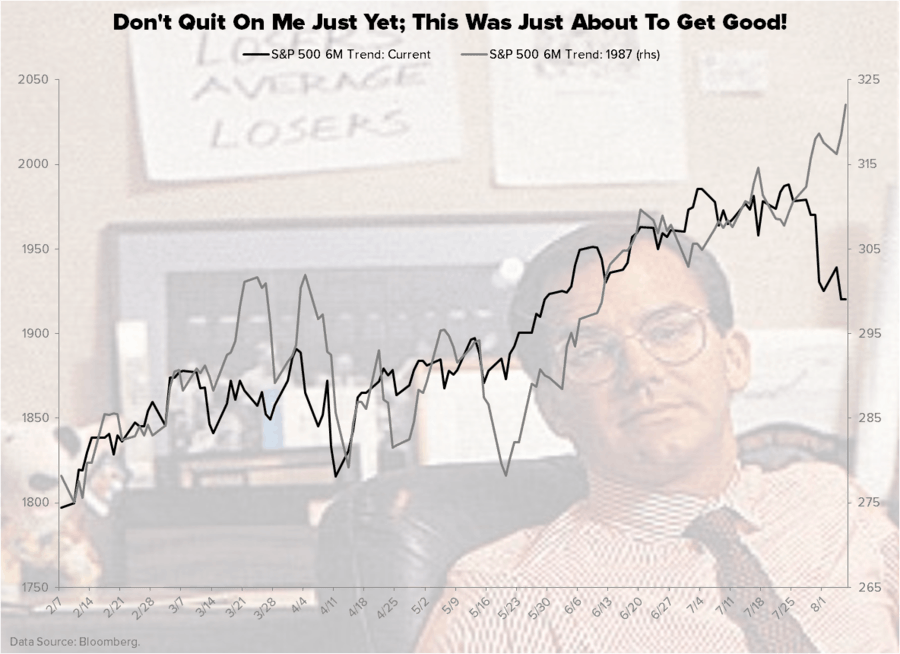

Other than a certified train wreck for whoever bought SPX 1987, what would 1829 look like?

- A -4.7% correction from yesterday’s closing price of 1920

- A -8% correction from the all-time high (1987) – the Russell 2000 has corrected -7% since July 7th

Oh, and about 1987… if you want to go all crashy in your investment meeting today, how ominous of a date/level is that?

If I am right in that I am not bearish enough on the SP500 (yet), and my long-term TAIL risk line of 1829 snaps. Oh snap, they will. That’s the point about my definition of TAIL risk – once it’s on, the only support strategy (level) I’ll be recommending is prayer.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.43-2.53%

SPX 1899-1929

RUT 1107-1131

India’s BSE Sensex 25236-26311

VIX 14.92-18.59

Gold 1281-1314

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer