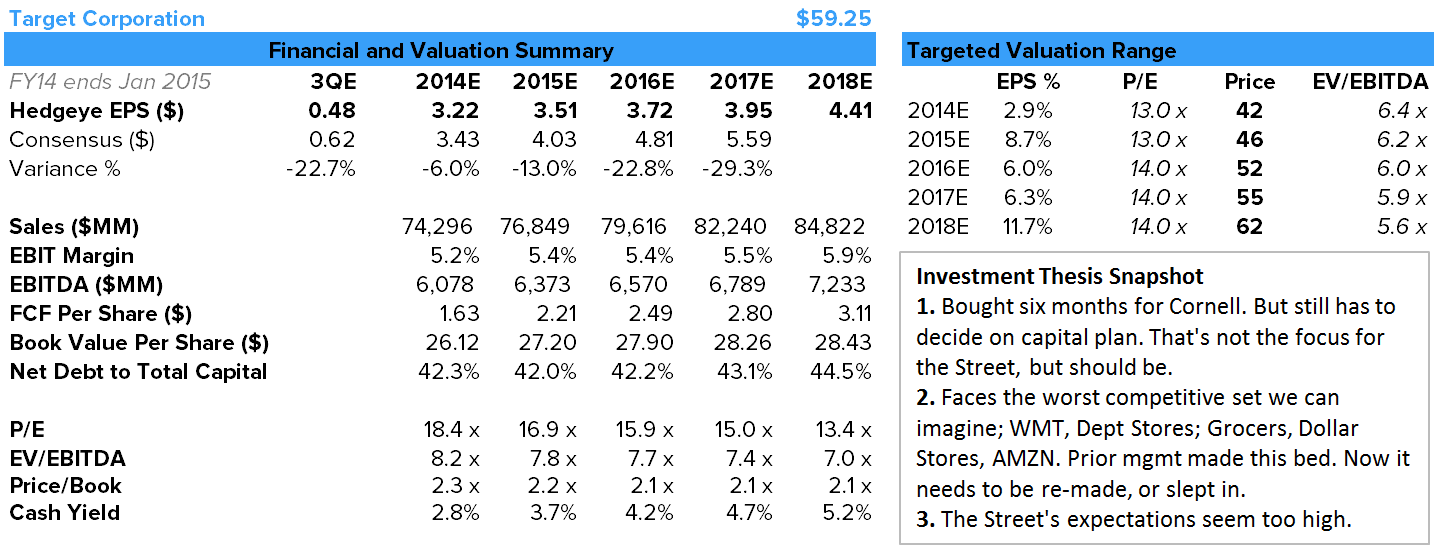

Conclusion: TGT just bought itself six months. New CEO Cornell said the right things on the call and expressed a sense of urgency to fix the company – but without getting out over his skis. Overall, good first impression. The way we see it, only $0.30 of the $0.50 guide down is accounted for operationally. That leaves Cornell a pad while he decides what to do to fix a company in dire need of a turnaround. No wonder the stock is up, especially with the highest short interest since the last recession. Keep in mind that a turnaround of this magnitude does not come solely through better management, better processes, or best practices. It costs money, and potentially quite a bit. The key here – until we hear Cornell’s plan – will be where the Street shakes out for 2015. Based on the size of the capital plan, it’s quite possible that TGT does not earn $4.00 for another 3-years. If there’s no capital plan, then it will be easy for us to remain flat-out bearish. In the meantime, if expectations come down to the $3.50 range for 2015, it will be tough to stay short Target – despite valuation. Otherwise, valuation is lofty enough for us to stick with our bearish positioning pending a roadmap as to what Cornell will do (as compared to what he should do).

Full Details

The fact that TGT did not trade down on a $0.50 (14%) guide-down in earnings for a year that is already half over is pretty amazing. That begs the question, if the stock is down only 5% year-to-date on a 29% cumulative earnings guide-down, what will take it lower? The answer is another guide down. That seems ridiculous at face value for two reasons; 1) we just saw the biggest guide down ever for TGT, and 2) the way we see it, only $0.30 of the $0.50 earnings reduction can be accounted for operationally. The remainder gives Cornell a lot of breathing room as he develops a plan for Target to escape from inadequacy. Yes, TGT just bought time, and by the stock’s reaction it got a great deal. But this says nothing about the earnings power for the company in 2015 and 2016. We think that we could be looking at sub $4.00 EPS for each of the next 3-years.

The key near-term factor is where consensus numbers shake out for 2015. If they’re as low as $3.50, it will be tough to stay short Target. Looking 1-2 quarters out, we need to know Cornell’s plan. We can rant all we want about what we think the right capital plan is for this company, but the one he chooses is what matters.

Keep in mind that the guy has been on the job for just 8 days. No one (including us) has a clue as to what he is going to do to fix this company. We’ve been of the camp that he can either stick with Target1.0 and make tweaks to the model that will grow earnings at an accelerated clip near-term (good for stock today, not 2-3 years out), or he can go for Target2.0 and make the major investment needed to restore Target to its former glory (bad for near-term earnings, good for long term stock). Cornell did a perfectly fine job in his debut. He said all the things a new CEO at a mega cap company should say, but did not get too far out over his skis. No promises on when we’ll see an action plan, but he did appear to have a sense of urgency in getting something done.

From where we sit, today’s stock action is solely a manifestation of the fact that the big earnings whiff has happened, and why would anyone be short it from here otherwise. But the fact of the matter is that the earnings draw down really has nothing to do with the capital allocation it will take to fix this company and meaningfully accelerate growth across categories. Keep in mind that we heard the Chief Merchant talk on the conference call for 27 minutes about all of the ‘amazing’ product initiatives like Andrew Zimmern Home line (solid), Honest Company by Jessica Alba (A+), Skechers partnership (very good) to Beaver Canoe (huh). But despite all this, Target can’t comp. e-commerce was ok, because of mobile – traffic on the core site was down. Even mediocre brands are growing web traffic. Why should TGT’s be down? Our point here is that there’s more to do than just blocking and tackling, which will end up being expensive. It might be the best capital Target ever spends, but it could be a lot.