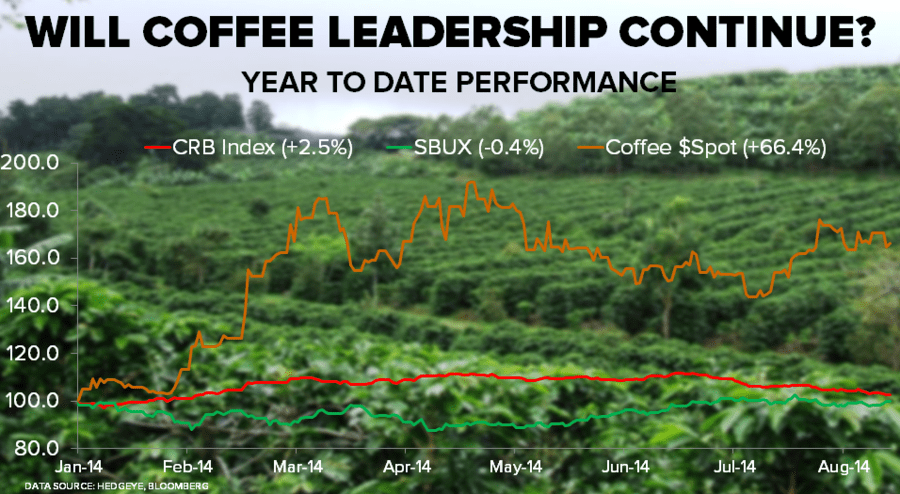

In terms of asset price leadership this year, one of the more outstanding performers has been coffee, which is up more than 64% on the year-to-date. Tomorrow, August 21st at 11am, our commodities macro analyst Ben Ryan is hosting a conference call on the outlook for coffee, which postulates, “Coffee Prices May Move Much Higher From Here” with expert Judith Ganes-Chase.

The call is obviously relevant for a lot of different equities, including CAFE, JO, SBUX, DNKN, MCD, MDLZ, GMCR, THI.

Contact sales@hedgeye.com to learn how to get access.