TODAY’S S&P 500 SET-UP – August 20, 2014

As we look at today's setup for the S&P 500, the range is 35 points or 1.49% downside to 1952 and 0.27% upside to 1987.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.97 from 1.97

- VIX closed at 12.21 1 day percent change of -0.89%

MACRO DATA POINTS (Bloomberg Estimates):

WHAT TO WATCH:

• Argentina to pay foreign-currency bonds locally

• GE to invest $3.5b in aircraft engine operations: Nikkei

• Samsung developing smartphone chip to replace Qualcomm: Maeil

• Chinese hackers use Heartbleed to enter Community Health

• Apple rises to record amid optimism around new products

• Citigroup said to weigh sale of Japan consumer bank unit

• U.K. FCA seen unlikely to cap fund manager pay

• AT&T seeks to offer faster high-speed Internet vs Google

• Walgreens CFO pressured to exit after forecast error: WSJ

• Dodgers TV blackout fuels unease over Comcast-Time Warner

• Elon Musk’s SpaceX says not raising private capital

• Softbank’s Son says considering next move after T-Mobile

• Amazon may start drone delivery in India: Economic Times

• Petsmart exploring options including possible sale

• U.S. Coast Guard responds to Duke Energy diesel spill in Ohio

ECONOMY:

• 7am: MBA Mortgage Applications, Aug. 15 (prior -2.7%)

• 10:30am: DOE Energy Inventories

• 2pm: Fed releases July FOMC minutes

GOVERNMENT:

- President Obama on vacation on Martha’s Vineyard

- Senate, House out on August recess

- 2pm: Brookings Institution discussion “Ukraine Crisis and Russia’s Place in the Intl Order”

- U.S. ELECTION WRAP: Reid on Mont., S.D.; Alaska; Obamacare

AM EARNINGS:

• Lowe’s (LOW) 6am, $1.03 - Preview

• Staples (SPLS) 6am, $0.12

• GasLog (GLOG) 6:02am, $0.11

• JM Smucker (SJM) 7am, $1.37

• Madison Square Garden (MSG) 7:30am, $0.18

• Target (TGT) 7:30am, $0.78 - Preview

• American Eagle Outfitters (AEO) 8am, $0.00 - Preview

• Eaton Vance (EV) 8:45am, $0.62

• Raven Industries (RAVN) 9am, $0.26

PM EARNINGS:

• Hain Celestial (HAIN) 4pm, $0.89

• L Brands (LB) 4pm, $0.62 - Preview

• Hewlett-Packard (HPQ) 4:05pm, $0.89

• Synopsys (SNPS) 4:05pm, $0.60

• Semtech (SMTC) 4:30pm, $0.39

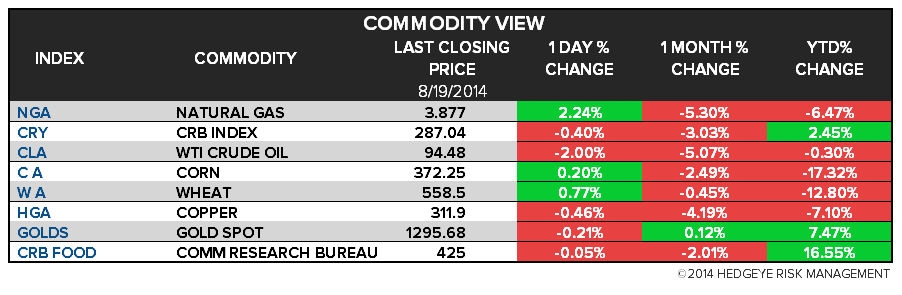

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- India Seen Passing China as World’s Biggest Cotton Producer

- European Gas Reverses Biggest Drop Since 2009 on Ukraine: Energy

- Putin Turns Poles Into Cider Lovers as Russia Food Ban Bites

- 3-D Printed Jets and Bicycles Spur Demand for Metal: Commodities

- Gold Little Changed Near 2-Week Low on Dollar as Platinum Falls

- China Port Seen as Economic Barometer Set for Record Supply

- Glencore Says Commodities Outlook from Copper to Zinc Improving

- Zinc Paces Metals Advance as Glencore Cites Tightening Market

- Cotton Crop in India Estimated at Near Record 39.6 Million Bales

- Operations at Mongolia’s Tavan Tolgoi Mine Halted, Macmahon Says

- Steel Rebar Falls to Record Low Before China PMI as Output Gains

- Fortescue CEO Says Co. Expects Iron Ore Price to ’Drift Up’

- Gabelli’s Bryan Tops Gold Funds as Miners Rally: Riskless Return

- Russian Grain Trader Beating Cargill to Olam as Exports Surge

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team