Conclusion: ‘Better than expected’ does not equate to a good quarter. Yes, we liked the 3.2% comp, 96% new store productivity, and $100mm repo – the second highest ever for DKS in a single quarter. It’s rare that DKS beats a quarter – we’ll give a golf clap when it’s due. But when all is said and done, depending on how you adjust for special charges, earnings were down between 5-10% on +10% sales growth. Not exactly a good quality number. On top of that, inventories remain elevated, margins are under pressure, and e-commerce grew at its lowest rate in 11 quarters. None of these factors get us particularly excited about owning this name – over any duration. Most importantly, to us at least, while people will obviously be talking about Golf due to the horrible trends and restructuring, we think there are bigger takeaways; a) looked at over a longer time period, this Golf Galaxy deal was simply horrendous. DKS bought at the top of a golf cycle, and is downsizing at the bottom of one. Textbook example of how not to deploy capital. B) we think that there’s a bifurcation in the golf market that is making it structurally unable for DKS/Golf Galaxy to compete. The company is taking its presence from 20% of sales to 15% and ultimately to 10%. Maybe the right answer is zero. The bigger question is whether or not this is an example that might apply to the rest of the Dick’s business as well. We’re modeling mid-single digit EPS growth – 200-300bp below the rate of store growth – over the next 5 years. We think that this stock is flat-out expensive.

GOLF: BUY HIGH, SELL LOW

There are a few things that don’t sit right with us about the Golf business, and the downsizing effort that the company is taking. Clearly, the golf equipment business is under severe pressure. That’s nothing new. This started six quarters ago for Dick’s, and has manifested itself in financial results for virtually every other retailer and brand that participates heavily in the Golf business. But what we don’t understand is that Dick’s bought Golf Galaxy in 2006 – right at the top of a golf cycle -- as a way to strategically double down on a category that it viewed as a long-term value creator. Now we’re sitting here at what is arguably the bottom of the golf cycle, DKS is cutting costs from the model outright, and it’s even talking about how 63% of its Golf Galaxy leases come up within 3-years and will be candidates for closure. We’re not necessarily saying that golf is a good investment now. But with retailers under pressure and OEM’s cutting capital allocation to golf equipment, this strikes us as an opportunity to take share and reposition for the next upturn, if nothing else. Buying High, and Selling Low is rarely a winning strategy. Unless of course, the company has reason to think that it simply won’t be a part of any upturn in the market.

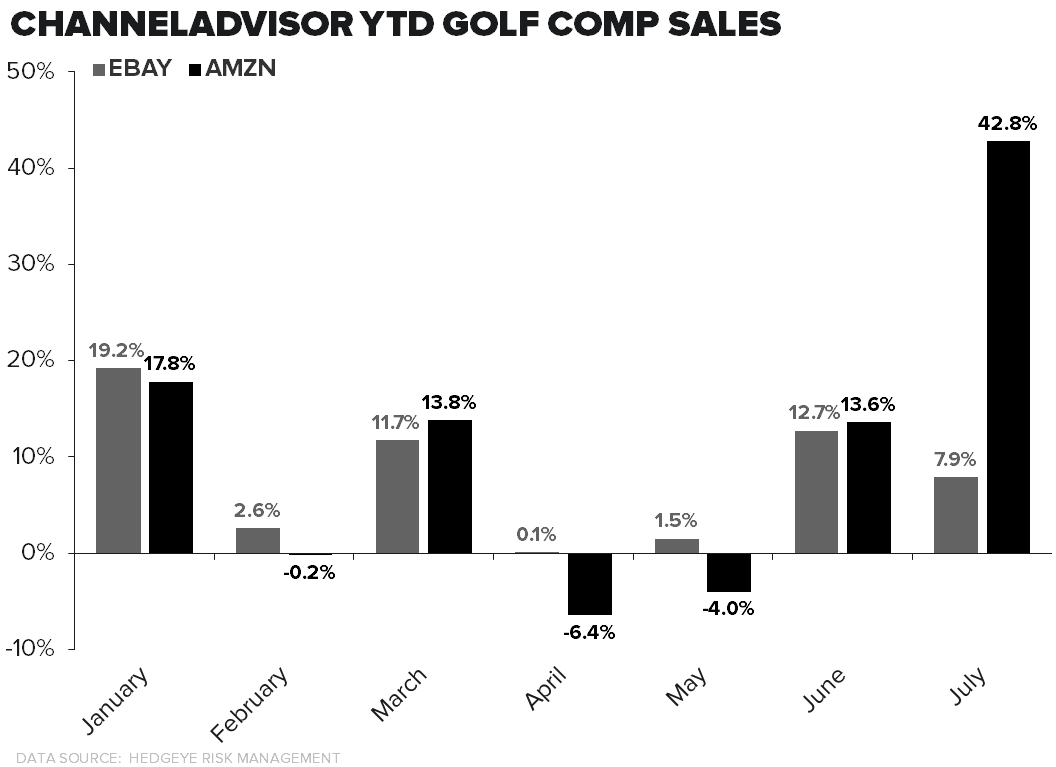

Based on the monthly sales trends for Amazon and eBay, we’re inclined to think that DKS is right in that it will simply not participate in any eventual upside in the golf space. In other words, we can simply write this off as a deal gone bad. Consider this. The time of year where most golf equipment is bought at full price is in April and May. Then discounts pick up in June, and accelerate meaningfully as the Summer progresses. Amazon’s numbers, in particular, show a simply staggering acceleration from -5% in April/May to 43% as we entered the key discounting period in July.

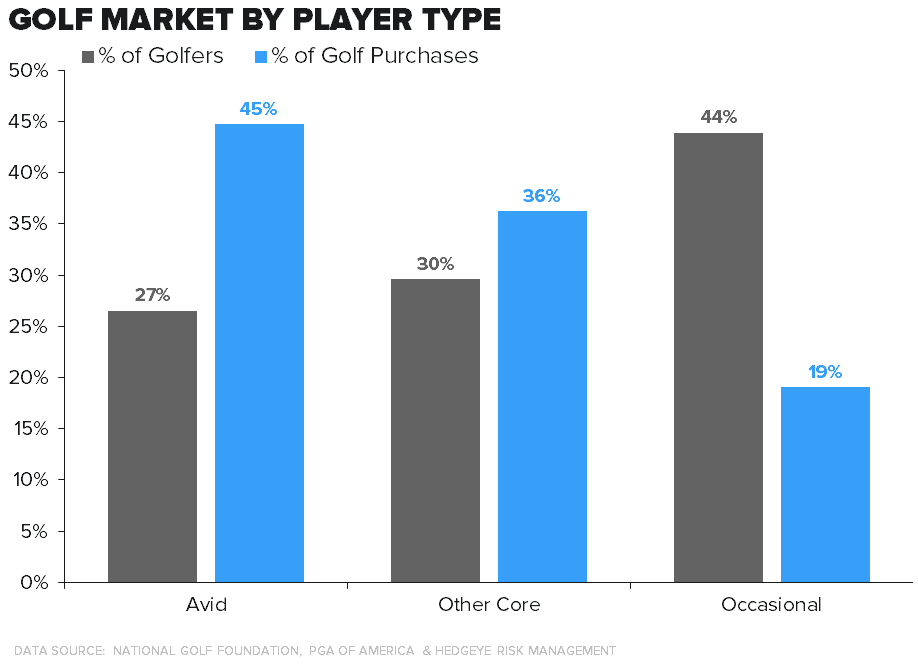

What we think is happening is that there’s an increasing bifurcation in the golf market. Dick’s sells primarily to the ‘Occasional’ golfer, which accounts for about 44% of the golfing population. ‘Avid’ and ‘Core’ golfers are about 26% and 30%, respectively, and tend to shop in much higher-end golf specialty stores. One might think that this is not too bad, as it leaves 44% of the market for Dick’s. But that ‘Occasional’ player is also the lightest spender, and only accounts for about 19% of the market. That’s the same consumer that is more inclined to shop on Amazon or eBay for equipment at a heavy discount. An Avid golfer (45% of total spending) is not buying new gear on Amazon in August because it’s cheaper. They don’t care about price – and they have a favorite local store with high-end service where they buy equipment. Dick’s attempted to fill that void by hiring 400 Golf Pros to work in its Golf Galaxy stores. But they were all fired last month. Dick’s can’t compete with the golf specialty shops at the high end, and it’s proving that it can’t compete online with Amazon at the low-end.