Back in late November, I wrote a post titled “Building A Case for Casual Dining in Early 2009” in which I highlighted the following catalysts/themes that would work their way into the market in the early part of 2009:

(1) Currently gas prices are nearly 40% below last year’s level and likely to stay there for some time.

(2) There is a broadly accepted and recognized need for massive fiscal stimulus in early 2009.

(3) Reductions in restaurant capacity in 2009, especially in the bar and grill segment.

(4) The decline in commodity prices provides a backdrop that can help mitigate the decline in margins.

(5) Valuation

Outside of top-line trends, which have retreated to 4Q08 levels, these five catalysts remain the primary drivers of the casual dining group’s stock performance. The only differences now are prices and the fact that these catalysts for the most part will become industry headwinds.

(1) Gas Prices

As I said earlier this week (please see post titled “Gas Prices – Q4 Inflation”), gas prices have been extremely favorable on a YOY basis for restaurant companies this year (down 38% on average in 1H09). Looking at the chart below, this YOY cost benefit will start to moderate and could go away in the fourth quarter. If gas prices stay at their current level (though they typically decline after the peak summer season), they will be up on a YOY basis come early November.

(2) Fiscal Stimulus and Casual Dining Demand

The bullish case for Casual Dining and Restaurants in general is that easy same-store sales comparisons going into 4Q09 will help the stocks. Casual dining same-store sales growth became less bad in 1Q09, but July levels are not much better than what we saw in December on a 2-year average basis. We still need to see a pick-up in job creation before we will see a real turnaround in dining out trends, and the visibility on that happening anytime soon is murky. And, yesterday’s job news supports this thesis. Yesterday, initial claims rose 15K to 576K in the week-ended August 15th, marking the second straight increase and ahead of consensus expectations of 550K. In addition, the four-week moving average rose to 570K from 566K in the prior week, the highest level since mid-July.

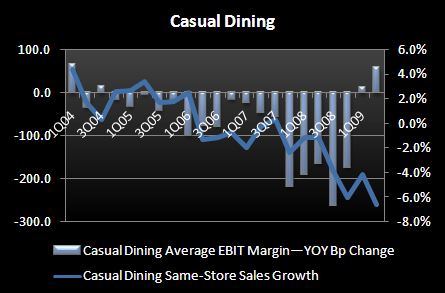

(3) Capacity Reductions

New unit growth has come down in 2009 and development related costs have come out of the P&L. By focusing more on in-store unit economics, the casual dining restaurants as an industry have created much leaner and more efficient business models, which have helped to sustain margins in this challenging sales environment. The majority of the casual dining operators will not re-accelerate growth in 2010 so development related costs should remain low, but as they lap the implementation of these cost saving initiatives, it will become increasingly more difficult to grow margins with negative same-store sales growth.

The YOY margin growth trend we saw in 1H09 is not sustainable with continuing declines in comparable sales growth, particularly 7%-plus declines as we experienced in June and July, as measured by Malcolm Knapp.

(4) Commodity Prices

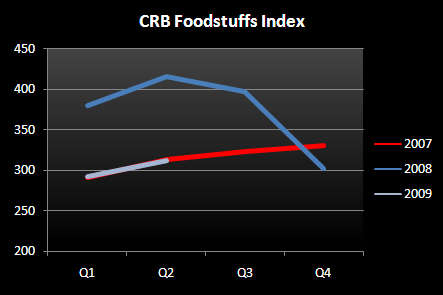

Looking at the chart below, lower food costs helped to mitigate casual dining margin declines during the first half of 2009. Like gas prices, the YOY food cost benefit will moderate in Q3 and most likely go away in Q4. The second chart below shows 2007, 2008 and 2009 food prices as measured by the Commodity Research Bureau (CRB) Foodstuffs index, an index based on the prices of hogs, steers, lard, butter, soybean oil, cocoa, corn, Kansas City wheat, Minneapolis wheat and sugar. Food prices initially turned favorable in 4Q08 on YOY basis and remained so in 1H09. At current levels, food prices will be up on a YOY basis come 4Q09. Of course, not every company will be impacted immediately, due to the fact that many restaurant companies have long-term contracts. That being said, as we head into the third and fourth quarter earnings seasons the commentary from most management teams will be to not expect the same benefits in 2010 as there were in 2009.

(5) Valuation

The biggest delta between now and late November when I wrote “Building a Case for Casual Dining in Early 2009,” however, is price. Year-to-date, casual dining stocks on average are up 80%. The group on average is trading at 6.6x on an EV/NTM EBITDA basis relative to 4.4x on November 30, 2008. The casual dining industry is not going away. It is a cash rich business, but sales trends will remain soft in the near-term, putting increased pressure on margins. The group's trading performance on average is flat in the last 3 months, but relative to upcoming catalysts, the risk/reward associated with these casual dining names seems to lean to the downside.

One more difference between now and then is my competitors’ ratings of the casual dining companies. Overall, analysts are still more bearish than bullish, but they are marginally more bullish today than they were then.

Today

November 30, 2008