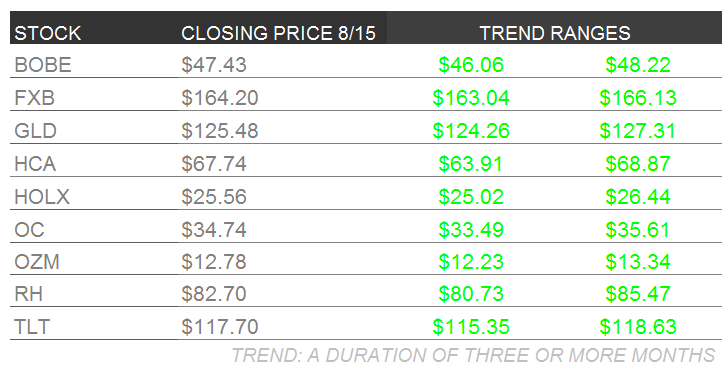

Below are Hedgeye analysts’ latest updates on our nine current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

We also feature three recent institutional research notes that offer valuable insight into the markets and the global economy.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

BOBE: This week Bob Evans Restaurants (BOBE) released an investor presentation providing their take on a series of (what they characterized as) "misleading" statements made by Sandell Asset Management, an activist investor in the restaurant company.

The level of activism in the restaurant industry has never been more rampant.

In the past year alone, we’ve seen CBRL, DAVE, DRI, BJRI and BOBE attract largely uninvited attention from these investors. BOBE has a long history of mismanagement, evidenced by flawed strategic rationale, an excessively bloated cost structure and severe underperformance relative to peers. Fortunately, its poor operating performance presents a tremendous opportunity.

Our analyst team believes activist investor Sandell has correctly identified significant and largely feasible opportunities to enhance shareholder value. Particularly, we see tremendous upside value in selling the foods business, transitioning to an asset light model and refocusing capital allocation.

FXB: We added the British Pound to Investing Ideas earlier this week. Click here to read the full report.

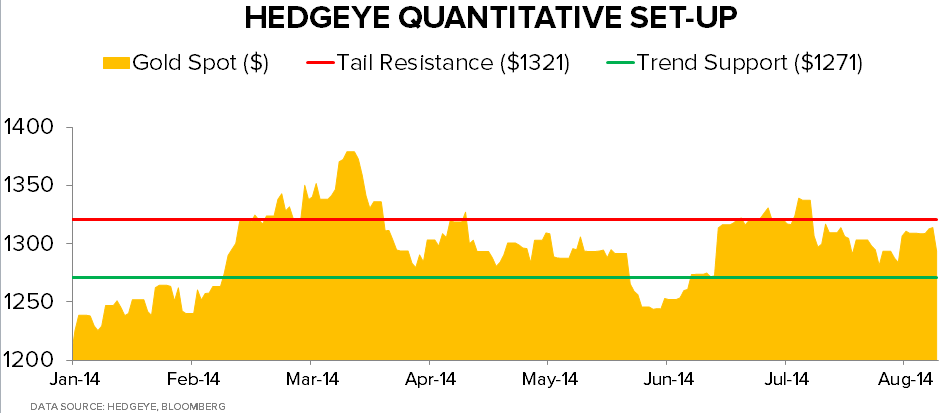

GLD: Gold continues holding its range in the face of expectations for a more dovish Mario Draghi as European economic data continues to decelerate and surprise to the downside. From a quantitative perspective, we are looking for:

- a breakout ABOVE @Hedgeye Long-Term TAIL line of resistance at $1321= bullish signal

- a breakdown BELOW @Hedgeye Intermediate-term TREND support at $1271 = bearish signal

European economic data continues its deceleration and European equities are broken down in our model from a TREND perspective. Equity indices got a bounce Friday but a weaker Euro and record-low sovereign yields are likely front-running a marginally more dovish move from Draghi:

1-month changes:

- EUR/USD: -1.4%

- German 10-year Bund Yields: -19 bps to 1.0%

- French 10-year yields: -23bps to 1.39%

- Italian 10-year yields: -21 bps to 2.61%

- Gold: +55bps

In the face of a breakdown in European equities and a sharp decline in Eurozone economic strength (Q2 sequential GDP comped a goose egg yesterdayà 0.0%!), the market believes in a similar response from Yellen. The 10-year hit new YTD lows this week (2.39%) as the centrally-planned currency war heats up. Both the United states and European growth has not slowed simultaneously since Q3 2011. The outlook for the USD will continue to be the driving force.

The Euro has devalued 1.4% against the USD over the last month.

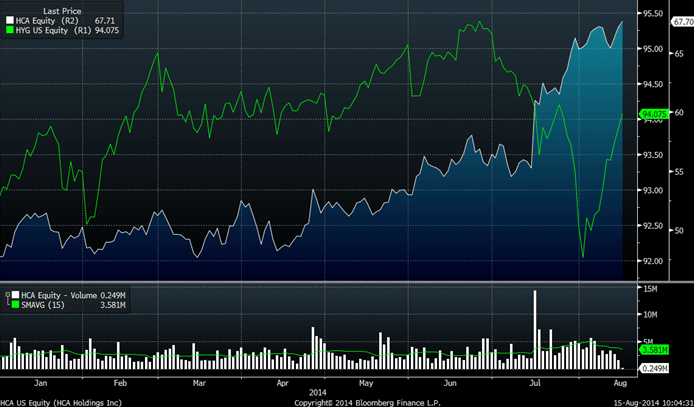

HCA: The high yield debt market was hit hard recently as signs of slowing global economic growth accelerated and military hot spots appeared to deteriorate. At least, that was the narrative put to actual negative fund flows (client withdrawals) from high yield bond funds.

So, what does this have to do with HCA? If we wind the clock back to 2009, high yield markets were the single most important factor to hospital stock prices.

In 2009, yields spiked, the HYG price collapsed, and doubt set in about the ability for highly indebted hospital companies to refinance or add new debt for acquisitions. What we have witnessed in the last few weeks has been the complete opposite of 2009. In other words, as high yield was getting hit, HCA and other hospital stocks rose.

We think this potentially means a few things:

- The high yield debt market prefers domestic US consumption over global exposure

- The Affordable Care Act is a bigger driver than the potential yield headwinds

- Medical consumption is recovering in the US, again offsetting concerns over yield pressure.

The Hedgeye Macro Team has us vigilant for signs of stress and slowing growth, so we’ll stay vigilant. But for now, it appears good fundamentals are taking a back seat to bad market trends.

HOLX: Healthcare sector head Tom Tobin has no update on Hologic this week.

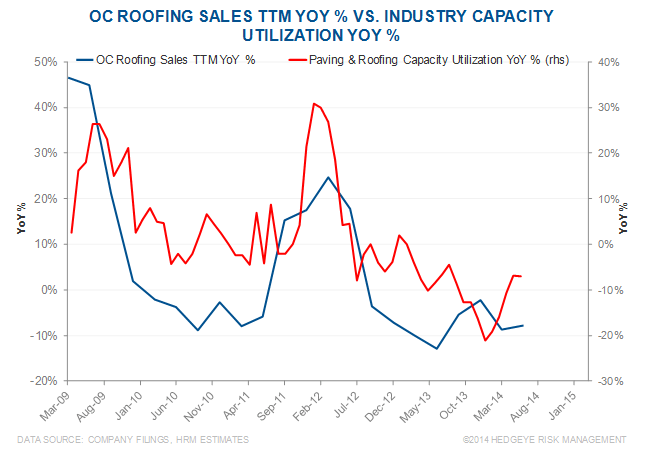

OC: Last month, the largest competitor, GAF/ELK, announced a price increase of 4% to 7% for its roofing products beginning in September. Owens Corning followed with a price increase of 6% to 9%. These price increases signal a more stable environment for the remainder of 2014. A price increase in its roofing segment may help margins, while improving roofing capacity utilization may help OC’s roofing sales (see chart below). OC’s management expects to take back market share it lost in 1H 2014 for 3Q and 4Q as a result of these price increases and a more favorable industry environment.

OZM: Shares of Och Ziff were down marginally this week on misplaced fears about insider selling. Dubai International, one of the original investors in the company, along with publishing magnates the Ziff brothers, filed a new institutional 13F filing showing a slightly reduced position in the leading hedge fund manager. Essentially over the course of last quarter Dubai International sold 3 million of OZM or just a 10% reduction of its original position of 33 million shares.

The Street and several media outlets viewed this as projecting a negative outlook for OZM because of Dubai potentially cooling on its forecasts for its holding. However, we view the modest reduction of the OZM holding as a reasonable way for a large institutional holder to diversify and that it lowers the future potential of a large amount of OZM stock to come to market with this dribble out selling strategy in effect.

Over time, we expect that a more diversified shareholder base and less concentrated large holders of OZM shares to be a more healthy aspect for the company.

RH: Market share trumps store productivity. For the most part, people are underestimating the ramp in Restoration Hardware’s addressable market as the company continues to expand into new categories. Over the next five years, there should be $45bn upside in market opportunity for RH simply by expanding its presence into new categories at retail, including kitchens.

An important note: we analyzed every market of the US, and isolated only consumers making over $100k annually. The government’s aggregate numbers include every income level. But the fact of the matter is that the average American spends $857 annually on home furnishings, while those making over $100k spend $1,779.

This bodes well for our favorite name in retail.

TLT: It was a great week to be long the Long Bond. The 10-year US Treasury yield slid to another fresh 2014 low, slipping six basis points to 2.34%.The TLT (iShares 20+ Year Treasury Bond ETF) which we added to our high conviction list last week is up 2%.

Our bullish view remains counter to macro consensus expectations. Incidentally, on January 1, the consensus forecast of the 66 most senior economists for the year end 10-year US Treasury yield was (drumroll...) 3.44%.

* * * * * * * * * *

Click on each title below to unlock the content.

Botched communication ≠ a broken story. This story is fundamentally on track. Could be dicey for a qtr. But the roadmap to $70 is there.

We Think Fed Will Surprise to the Dovish Side

All told, we remain the bears on US interest rates/bulls on long-term Treasuries as growth is likely to slow throughout 2H14.

ICI Fund Flows: Tantrum and Struggle

In the most recent ICI survey, taxable bond funds experienced a substantial snap outflow joining domestic stock funds with dour trends