"I believe in focusing on what you do best, instead of a lot of things." -Irwin Simon CEO HAIN

We recently added HAIN to the Hedgeye best Ideas list as a SHORT.

Irwin Simon was quoted saying the above quote at the time he bought Celestial Seasonings. Given HAIN has acquired 33 companies over the ten years I’m not sure the old management style still applies.

Yesterday we published a 70 page slide deck outlining our thesis on HAIN (if you would like a copy please email me.) The thesis centers on three key points:

ACQUISITION FATIGUE - HAIN has been a serial acquirer over the past ten years, acquiring over 33 companies. Although the company owns 50 brands, the 80/20 rule applies. Management is compensated to grow revenues and earnings, incentivizing them to acquire complementary companies. Not all the companies they buy, however, are complementary including a few recent ones that have been margin dilutive. We believe the core-business, ex-acquisitions, is slowing – a fact that management is doing their best to mask.

INCREASING COMPETITIVE LANDSCAPE -April 10, 2014, the day WMT announced it would carry Wild Oats, was the day organic food went mainstream. This move by WMT won’t be ignored by other retailers and will likely force gross margins lower for a number of organic companies. The current pricing umbrella in the organic space will create significant demand for private label products at traditional grocery chains. Can HAIN sustain its current business model in light of the new industry headwinds?

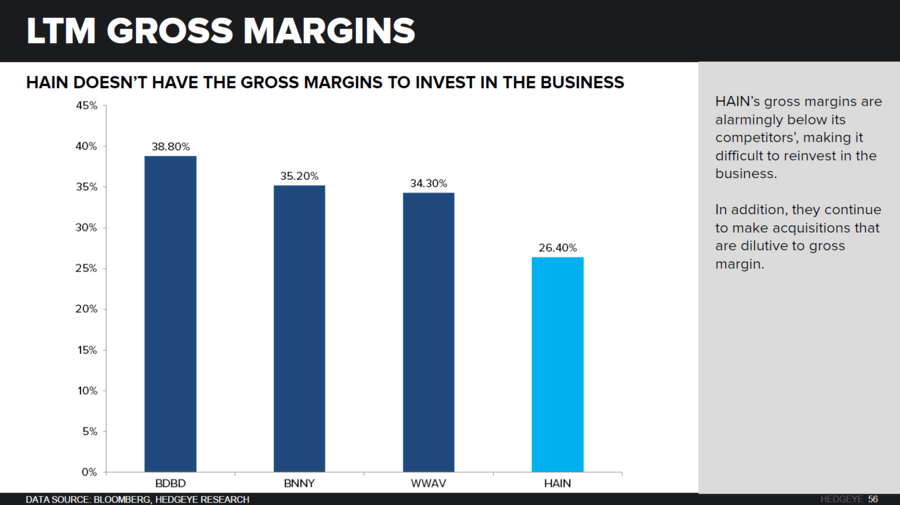

SLOWING TRENDS, MARGIN PRESSURE - HAIN’s absolute gross margins are significantly below its peer group, making it difficult for the company to compete in a more competitive marketplace. The increased competitive headwinds will slow organic growth and keep pressure on gross margins, forcing the company to cut SG&A at a faster rate than anticipated. This increases the likelihood that street expectations are too aggressive. Under such a scenario, the company’s multiple would likely contract.

The last bullet point is critical. At 26%, HIAN’s gross margins are below a typically strong organic company and put the company in a difficult spot to defend against increased competition. As we said on page 55 of the slide deck the following are the characteristics of a strong organic company:

- Notable competitive advantage; highly differentiated product giving the company a strong reason to be in the market.

- Sustainable gross margin, typically above 40%, which allows the company to reinvest in its brands.

- Resonates with consumers and helps engender loyalty.

- Validation across multiple channels.

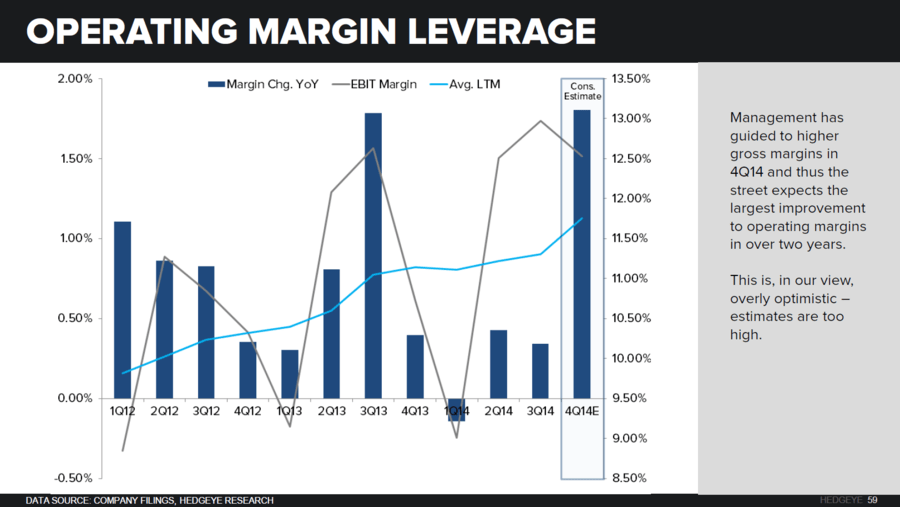

In addition, HAIN has significantly cut SG&A to levels that are also below its competitors’ making it difficult to support the business.

This has resulted in a significant improvement in operating margins.

How long can management rely on SG&A cuts to make the numbers?

Are they underinvesting in many of their brands?

We believe there will come a time when management must reinvest in their business and will be hard pressed to lever SG&A to the same degree.

If you would like to discuss HAIN further please call any time.

Howard Penney

Managing Director

Fred Masotta

Analyst