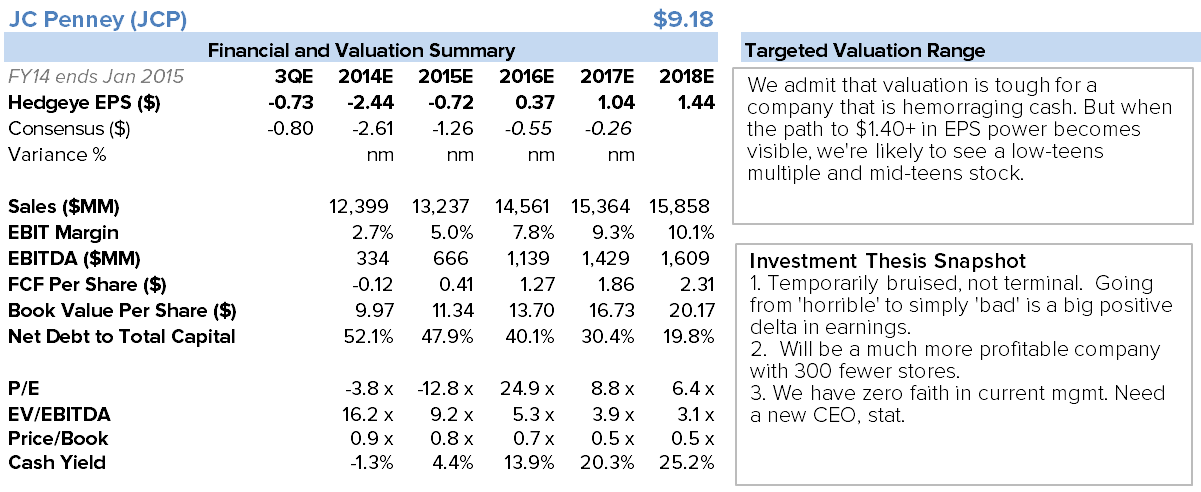

Conclusion: Even the biggest JCP bears have to give credit to Ullman’s team for executing this quarter. That said, it’s a little scary that key P&L and balance sheet levers were so jacked this quarter and yet JCP still lost $0.75 per share. We think it’s critical to bifurcate duration on the JCP call. The near-term call that will likely take it into the first half of next year is all about revenue and margin momentum, with little valuation support. We have a tough time making that call, even though the reality is that it will probably take this stock to $12 within another two quarters. Then there’s the long-term call where the stock looks outrageously cheap (6x p/e, 3x EBITDA, and 25% FCF yield) on our $1.45 in EPS. But our confidence in those numbers is in the bottom quartile of every name we track. Discounting back by 20% suggests that JCP is trading at 13x today – which is about right for a department store on steady-state earnings. The x-factor for us is JCP stepping up its store closures. We think there’s 300 that should be shuttered. Not just bad locations, but also some good ones where the lease could be bought at a premium. In the end, we think the stock is probably headed higher given momentum, and are not averse to owning it so long as it’s on a short leash. But we’d rather hold out for when the research gives us a higher degree of confidence in the longer-term model.

Full Details

Even JCP bears will have to give some credit to the company for putting up a 6% comp, 640bps Gross Margin improvement, and a 10% inventory reduction. It’s pretty rare to hit that kind of trifecta in retail – especially for a department store. On the flip side of that, it’s scary to see such tremendous metrics on the P&L – growth of 5% on the top line, 28% gross profit, 6% decline in SG&A, and yet have it still result in a loss of $0.75 per share.

This quarter is the best example yet of the two distinct calls that exist here, based largely on duration.

1) There’s the near-term momentum call. That’s the one that’s playing out now. We hate this call. Not because it doesn’t have merit. The reality is that it absolutely does. It’s the call that will likely take this stock to the low teens over the next 12 months as JCP continues to regain market share (which we firmly believe will happen based on our survey work), take margins higher, and improve its balance sheet. As it relates to market share, our work suggests that the two retailers most exposed to a revived JCP are KSS and M. Collectively they picked up over $1.5bil of the $5.9bil in sales that JCP coughed up over the past three years. That’s a lot more meaningful for KSS in percentage terms, and we don’t think KSS sees JCP coming.That said, this momentum in business recovery has so little valuation support because the company will continue to lose money for at least another two years.

2) That takes us to the longer-term (Tail) call. This is one that makes more sense to us, as we can model even a partial productivity rebound with a sub-peak margin, and we build up to $1.45 in EPS by the end of our model (’18). Keep in mind that all JCP needs to do is go from being ‘the worst apparel retailer’ to being just plain bad. While bad isn’t what we typically aim for in scouting out good long candidates, the math checks out. Going from trough sales per sq. ft. productivity levels in 2013 at $110 to $145 in 2018 would mean an incremental $4bil in revenue. As the chart below shows, that would put JCP’s productivity just ahead of where Dillard’s stands today, 22% below Kohl’s and its Agenda of Excellence, and 25% below JCP’s own peak – something it will likely never see again (but doesn’t have to).

One key consideration is that we can model these changes til we’re blue in the face, but if management does not have a plan to get there, then it’s a wasted exercise. That’s been our concern over the past year with Ullman at the helm. But on today’s conference call, we heard management make the first mention of a strategic plan that we’ve heard since Johnson was given the boot last year. They didn’t say what the plan is, and we have no idea if it will be a good one until we hear it live at the October analyst meeting. But even a mediocre plan is better than no plan.

If we use $1.45 in earnings, $1.6bn in EBITDA, and $2.30 in free cash flow in 2018, the stock at $9 is flat-out cheap across the board (6.4x earnings, 3.1x EBITDA, 25% FCF yield). But the problem is that we’re talking 5-years away. There are some companies where we can build a highly quantified and extremely defendable 5-year model. But our confidence level in our JCP 5-year numbers is low relative to where we stand with other companies. If we simply take up our risk premium on $1.45 in EPS and discount it back by 20% annually, then it suggests that today JCP is trading at about 13x normalized earnings. Maybe 20% is too steep, but we’ll take a conservative stance given that we have no clue what management intends to accomplish after the next two quarters.

What will get us really excited?

If they articulate a plan to close stores – a lot of them. Our analysis shows that there’s about 300 stores that should be closed. The company has not agreed with us in the past. But we think that changing dynamics in the real estate landscape is creating opportunities for JCP to jettison its less profitable stores, and get out of malls where it simply does not belong. Here’s a hypothetical example we whipped up for the Cherry Hill Mall in NJ. Currently JCP is one of three anchor tenants in an A mall. It’s likely doing only $165/ft, which is far too low for that property. The problem is that JCP’s customers don’t shop there. The property owner is generating $10mm in income today based on the existing productivity, but if it buys out the JCP lease, and converts to higher productivity concepts (such as Restoration Hardware, Cheesecake Factory, and Whole Foods, for example) the implied REIT income goes up to $24mm per year. Clearly, there’s enough to buy out JCP at a steep premium and still have money left over to build some walls to subdivide the store. As a frame of reference, JCP has about 140 ‘A’ mall locations.