Mania & Myopia: Historical data investigating the strength and intertemporal dynamics of recoveries following financial crises suggests it takes ~8 years to return to pre-crisis income levels/economic activity.

With the great recession officially ending in June of 2009 we are now 62 months into the current expansion and have traversed most of the expected period of subdued growth.

As we’ve noted, the frustration and impatience on the pace of the recovery that pervades media reports and pundit commentary offers an interesting juxtaposition against the almost universal acknowledgement that balance sheet recessions and the back end of long-term credit cycles invariably augur protracted periods of sub-trend growth

Imagine if all the spurious activity, all the sunken search and opportunity costs, all the manic speculation around the monthly NFP number were, instead, diverted towards infrastructure development or figuring out how to effectively teach our kids applied math. Anyway…..

The chart below remains unnerving, but not particularly surprising.

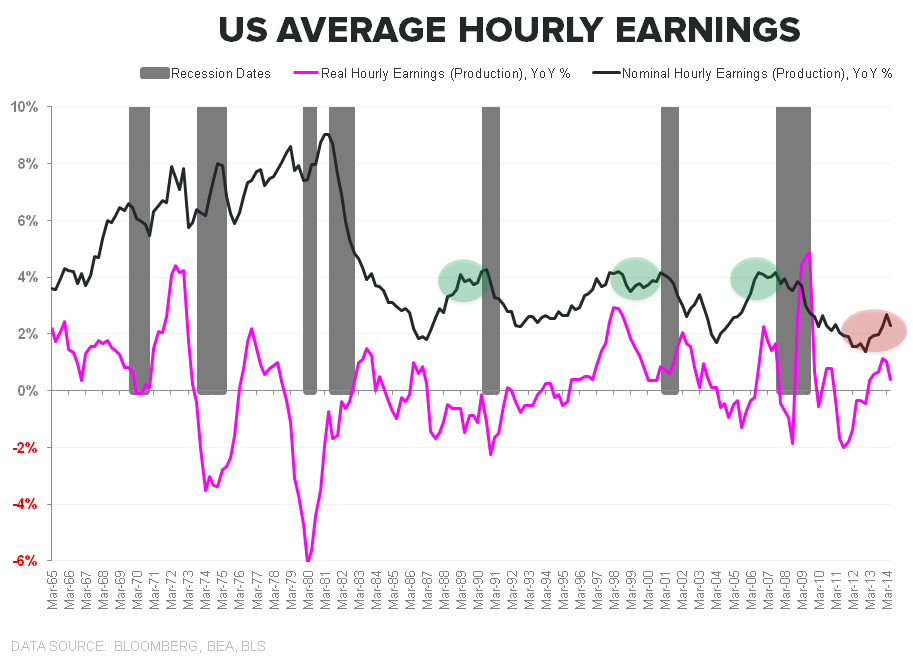

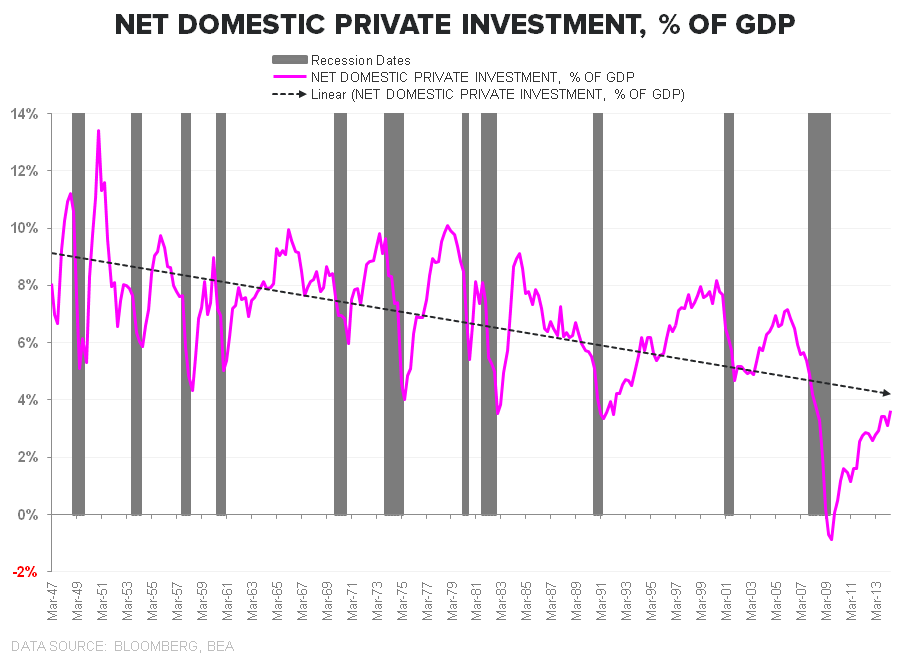

The Jobless, Wage-less, Investment-less Recovery?

The chart trifecta below shows earnings growth and the employment and investment level over prior economic cycles. The fact that employment, investment and earnings have all failed to return to prior levels underpins the emergent secular stagnation and employment hysteresis theories.

We won’t explore the principal demographic (population growth/LFPR), credit cycle (demand amplification), and productivity (slower output growth = slower growth in compensation for that output) arguments driving secular trends in each – here, it’s sufficient to simply re-highlight where we are currently vs cycle precedents.

As can be seen, the reality isn’t particularly surprising and the collective economist concern not unfounded.

Late Mid-Cycle Slowdown or Late Cycle Roll-over?

The logical question born out of the dour macro realities highlighted above, together with a bond market pricing in slower growth and smaller cap/consumer facing/early cycle equities significantly underperforming is this:

Does the market/macro roll-over with improvement in the chief labor and economic aggregates never materializing or is there still some runway in the current cycle?

We approached that question from a fundamental perspective in the table below by profiling the economic cycles of the last half century and the surrounding labor market dynamics.

Across each of the lead labor measures, we remain below average levels observed over the prior seven cycles. Of the six employment measures profiled, Initial claims sits as the best leading indicator of the economy with claims troughing approximately 7 months before the official peak in the economic cycle on average (note that we are using rolling 3-month averages in the labor/market data). With headline (& NSA) rolling claims making lower lows at present, at face value, it suggests the current cycle hasn’t fully crested.

The data is always good until it isn’t, the market is not the economy and the current cycle is unique in many respects (financial crisis, magnitude of central bank intervention, demographic inflection, reversal in LT interest rate cycle, etc) but the data mosaic is suggestive:

Historical financial crises analysis suggests a more subdued, but more protracted recovery (vs typical business cycle oscillations) and a parsing of the historical labor data suggests the next economic peak isn’t yet imminent.

#TIGHT?

Much of the debate of the last half year has centered on the underlying tightness of the labor market and read through for inflation and prospective policy. Conventionally, wages are viewed as a lagging indicator, with wage inflationary pressure building as the labor supply declines and the economy moves towards constrained capacity.

This canonical view of wage inflation certainly makes conceptual sense, but the empirical data is somewhat equivocal.

The best (& only) LT data set on real wage growth – which focuses on production and nonsupervisory workers - shows real wage growth has been flat/negative for most of the last 4 decades with the current post-recessionary trend in real wage growth comparing favorably with those observed over the last half century.

Further, whether we can return to the historical 3-4.5% level of nominal wage growth in the face of an aging workforce, declining labor supply, lower productivity and lower credit growth remains a bigger “If” now than ever before.

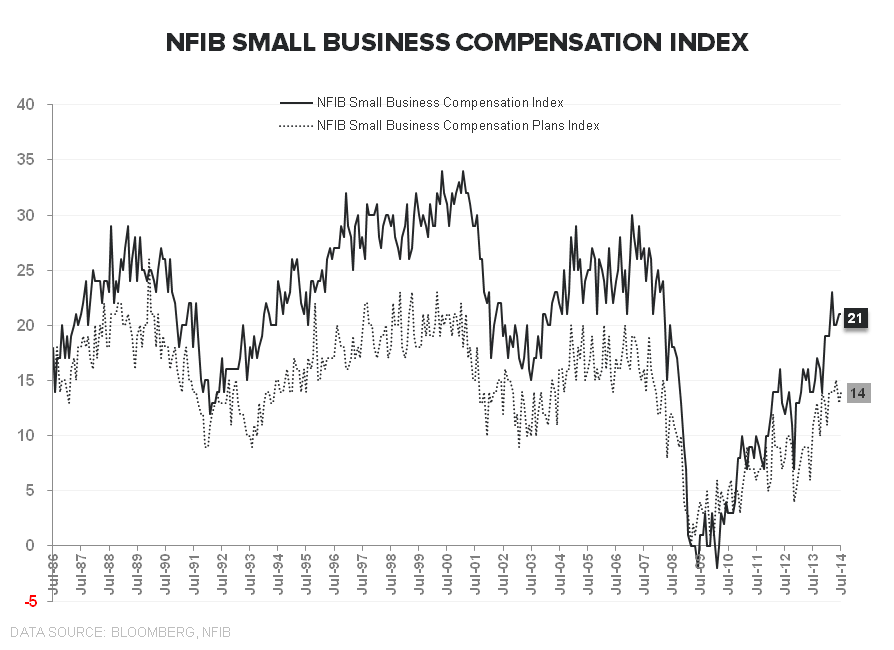

Surveying Slack & Common Sense Q&A:

Ultimately, whether a return to prior cycle levels in wage growth is an accurate barometer of the underlying health of the labor market is probably less important than the fact that the Fed has anchored on wage inflation as a key gauge of labor market slack and key driver in reaching/overshooting its stated inflation target.

Below we survey the current trends in measures of existing labor slack. In short, all the charts look the same with the prevailing trend remaining one of ongoing, albeit painstakingly slow, improvement.

Is the labor market probably tighter than the FOMC gives lip service to? Yes.

Would they rather overshoot target (particularly with ROW disinflation likely to continue prevailing) and play catch up? Yes, probably.

Is patience probably still a better prescription than panic and manic punditry with regard to the current labor market trends and the prospects for the current cycle? It would appear so.

Christian B. Drake

@HedgeyeUSA