TODAY’S S&P 500 SET-UP – August 14, 2014

As we look at today's setup for the S&P 500, the range is 44 points or 2.09% downside to 1906 and 0.17% upside to 1950.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

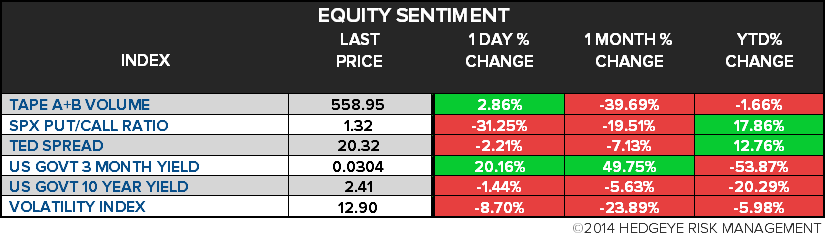

- YIELD CURVE: 2.01 from 2.01

- VIX closed at 12.9 1 day percent change of -8.70%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Initial Jobless Claims, Aug. 9, est. 295k (prior 289k)

- Continuing Claims, Aug. 2, est. 2.507m (prior 2.518m)

- 8:30am: Import Price Index m/m, July, est. -0.3% (prior 0.1%)

- 8:45am: Bloomberg U.S. Economic Survey, Aug.

- 9:45am: Bloomberg Consumer Comfort, Aug. 10 (prior 36.2)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 1pm: U.S. to sell $16b 30-yr bonds

GOVERNMENT:

- Senate, House recess; President Obama on Martha’s Vineyard

- 9am: Organization for International Investment Pres. Nancy McLernon, speaks to Bloomberg reporters, editors

- U.S. ELECTION WRAP: Status of Hawaii’s Primary; NRSC in Mich.

WHAT TO WATCH:

- Euro-region recovery stalls as biggest economies fail to expand

- Germany’s 10-yr yield drops below 1% for first time on record

- U.S. banks said to get enforcement letters in FX-rigging probes

- Cisco cutting 6k jobs, CEO seeks revamp amid stagnant growth

- InterMune said to draw bids from Sanofi to Roche

- Israel, Hamas extend Gaza truce in quest for broader accord

- Ukraine open to compromise on Russia aid as own convoys readied

- Intel agrees to buy Avago networking unit Axxia for $650m

- GE appliance unit said to draw interest from Electrolux, Quirky

- Carlyle’s Axalta is said to tap banks for $1b U.S. IPO

- Barclays index unit said to draw offers from Nasdaq, CME Group

- Pfizer wins panel backing to expand Prevnar vaccine in seniors

- Merck & Co. wins U.S. FDA approval of new type of sleeping pill

- Hilton, Ally, Seibu added to MSCI world indexes

- Puerto Rico’s Prepa faces repayment deadline on $671m in debt

- T-Mobile CFO hints higher Iliad offer OK: WSJ

EARNINGS:

- Advance Auto Parts (AAP) 8:30am, $2.01

- Agilent Technologies (A) 4:05pm, $0.74

- Applied Materials (AMAT) 4:02pm, $0.27 - Preview

- Autodesk (ADSK) 4:01pm, $0.29

- B2Gold (BTO CN) 6:30am, $0.02

- Bally Technologies (BYI) 4:01pm, $1.20

- J.C. Penney (JCP) 4:01pm, ($0.90) - Preview

- Kohl’s (KSS) 7am, $1.07 - Preview

- Nordstrom (JWN) 4:05pm, $0.95 - Preview

- Pacific Rubiales (PRE CN) 6am, $0.41

- Penn West Petroleum (PWT CN) 6:33am, $0.10

- Perrigo (PRGO) 7:42am, $1.55

- Plug Power (PLUG) 7am, ($0.04)

- Sina (SINA) 5pm, $0.09

- Wal-Mart Stores (WMT) 7am, $1.21 - Preview

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Commodities Fall to Six-Month Low as Gains for Year Evaporating

- WTI Oil Falls as U.S. Crude Stockpiles Increase; Brent Declines

- Silver Price Goes Electronic in Transparency Quest: Commodities

- Gold Climbs for Third Day Boosted by Ukraine to Middle East

- Copper Falls to Seven-Week Low on GDP Reports and China Output

- Corn Drops With Soybeans as Rain Seen Boosting U.S. Crop Outlook

- Palm Slumps to Five-Year Low as Bear Market Deepens on Supplies

- No Room at the Bin for U.S. Grain Amid Buffett’s BNSF Rail Jam

- Germany Needs More Coal-Plant Shutdowns as RWE Accelerates Halts

- Gold Consumption in China Shrinks 52% Amid Anti-Graft Campaign

- Gold Demand in India May Decline to Five-Year Low on Curbs

- Rebar Drops as Iron Ore at Record Low on China Financing Concern

- Putin’s Pipeline Bypassing Ukraine at Risk Amid Conflict: Energy

- Europe Airlines Cut Jet Fuel Hedging as Prices Seen Falling

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team