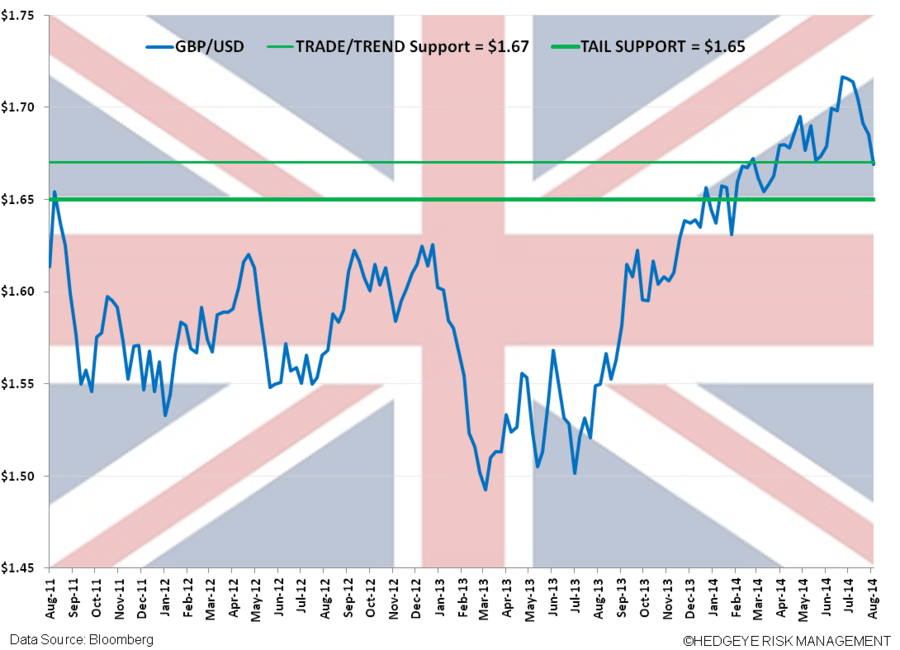

This morning we issued a buy signal on the GBP/USD (via the etf FXB) in our Real-Time Alerts with the cross reaching our immediate-term TRADE oversold level ($1.67) within our bullish long-term TAIL view (support = $1.65).

The GBP/USD has corrected -2.2% M/M and took a leg down this morning (~50bps) following the BoE’s release of its August Inflation Report. We believe today’s weakness reflects:

- UK wage growth that fell -0.2% in Q2 Y/Y (the first decline since 2009)

- BoE Governor Mark Carney rhetorically pushing out expectations for a rate hike to at least late 1H 2015 (though no specific guidance was given)

That said, the GBP/USD is up +12% since it troughed on 7/5/13 and continues to be supported by healthy underlying fundamentals that we expect to persist in 2H (and especially versus the Eurozone – click here for more on our negative outlook on European equities and the EUR/USD):

- UK unemployment rate fell 10bps M/M to 6.4%, the lowest level since 2008, and is now expected to drop below 6.0% by year end

- The Bank revised up its expectation for near-term growth to 3.5% in 2014

- CPI of 1.9% Y/Y is managed toward 2.0% target

Further, we expect a more dovish policy response from the ECB and Fed versus the BoE over the intermediate to longer term that should be supportive of the Pound versus the USD and EUR:

- Janet Yellen’s commentary suggests she remains an uber dove: (See Reuters article yesterday with current and former Fed officials indicating that Yellen and core decision-makers at the U.S. central bank are determined not to raise interest rates too early and risk hurting the fragile U.S. economy). We’ll be watching her Jackson Hole commentary beginning August 21 for a confirming dovish outlook.

- ECB’s Mario Draghi looks poised to issue QE over intermediate term. Following the June announcement of the issuance of the TLTRO programs to unlock lending, come Fall he may begin QE-lite purchases (via ABS). A hike in rates (after cutting in June) appears highly unlikely over the next year plus given underlying weak fundamentals and inflation expectations that are likely to miss on the downside.

Matthew Hedrick

Associate