Conclusion: This story is not broken -- far from it. This selloff is a perfect storm that could have easily been avoided by the company. Say what you want about uncharacteristically sloppy investor communication. It’s justified. With a 75x multiple, they have zero room for error. But the growth story here is intact as it relates to a) retail expansion, b) same store sales growth, c) category expansion, d) geographic diversification, and e) channel growth. Are there questions about how much capital Kate Spade Saturday needs to grow? Yes, and that’s perfectly normal. But if Saturday went away entirely our model would not miss a beat. The story is still 100% on track. People don’t seem to want to buy ahead of an ‘official’ rebasing of long-term guidance w Saturday-related costs. So it may be dicey for a quarter. We’ll pick our spots to add. But longer term, if you believe in our numbers, it’s not tough to get to a $70 stock.

Whenever a stock collapses like KATE just did – giving away $1.7bn in market cap (or 32%) in the course of about 90 minutes – it’s usually a punch in the jaw to let the market know that something has radically changed with the fundamental story. In KATE’s case, however, that’s simply not the case. The way we see it, this stock action was overwhelmingly driven by some very poorly chosen words by management on the conference call. The stock started to give up some early gains as CEO Leavitt spoke about the quarter being promotional, but absolutely collapsed after 52 minutes of prepped remarks when COO Carrera said something that sounded like…

[We gave you long term targets at the analyst meeting last year. Based on investment in Kate Spade Saturday, we may or may not push those targets out by a year. We’ll let you know in the fall.]

Ok, let’s put this into perspective. There are few companies that can make a statement like this – a very JV error -- and not get dinged materially. Mind you, as good as Leavitt and Carrera are operationally, both have little experience speaking to/through capital markets. But a 32% hit to market cap is more than a ding. It’s a high-speed collision. Take those comments, and now combine with a high-expectation stock that trades at 75x current-year earnings and is comping 30% -- then it gets a lot more dicey. The icing on the cake is that not only has Coach blown up, but the mighty KORS, which has served as a halo for KATE, has also started breaking down. Note good in combination with weaker gross margins due to clearance and investment in Kate Spade Saturday (a brand that is immaterial to the story today). On top of all that, KATE just restated its financials into a format with better forward disclosure, but did not give 2H13 restated numbers -- making it extremely difficult for the Street to build financial models in line with new reporting structure over the next two quarters.

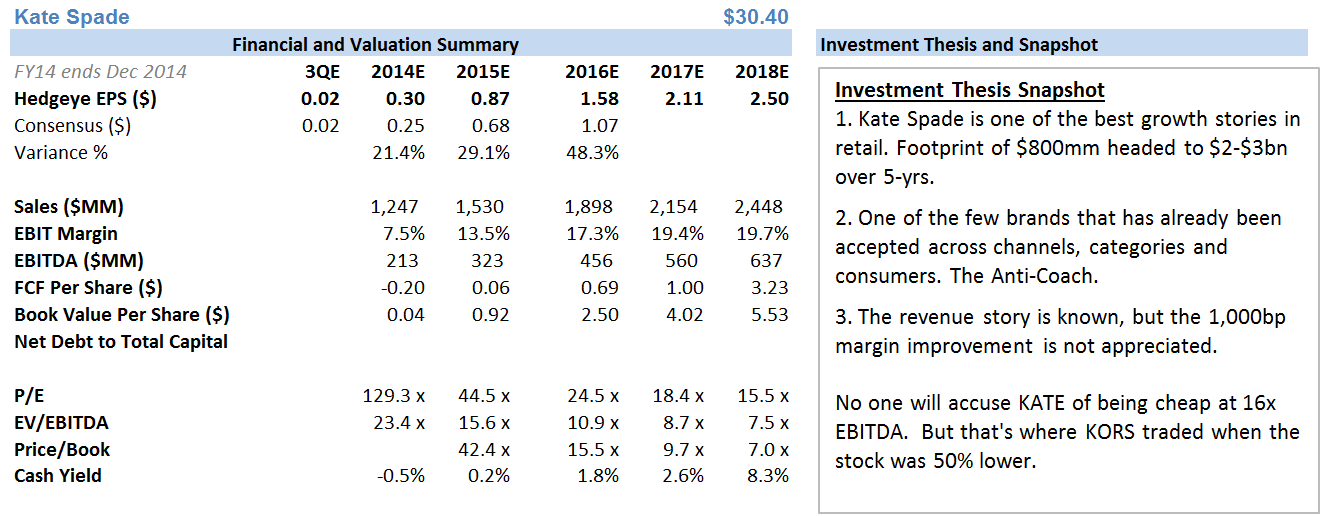

Combining all these factors, it makes sense to us that the stock got hit on this conference call. Note that we did not say ‘get hit on the print’, because that was otherwise solid. This was almost all about perception instead of financial factors. The company comped 30%, grew revenue at 49%, expanded margins by 658bps, and earned money for the first time in a 2Q since 2008. Something else to keep in mind… while the 30% comp was easy to get excited about (until management lost control of the call), the the fact of the matter is that upside to the SSS comp is finite. It won’t end next quarter, or next year. But it will ultimately moderate as KATE hits its steady-state store productivity rate, which we model at $2,000 in 2018. But keep in mind that KATE only reported $266mm in revenue this quarter. That compares to KORS at $919mm and COH at $1,136. There’s a lot of growth here that is not comp-related.

- Store growth should go from 245 stores today to 600 in year 5. For what it’s worth 560 of those stores are Kate Spade NY, while the remainder is Kate Spade Saturday and Jack Spade.

- International: The fact that US revenue was up 55% and International was up 54% is no mistake. The growth by geography is extremely balanced. As it relates to Int’l store growth, we saw recent openings in Macau, Hong Kong, Mexico, Middle East/Abu Dabi, and Malaysia.

- Wholesale vs. Retail: We like how KATE is expanding its wholesale doors. It’s not simply opening up the whole product line, like so many other brands do. But rather it is opening specific product categories at different wholesale accounts. This helps prevent channel conflict, and gives retailers content they believe to be exclusive.

When all is said and done, we’re not changing our earnings estimates. We think that KATE ramps from $0.30 in EPS this year to $1.58 in just two years. It’s next to impossible to find a ramp like that. Key modeling assumptions…

- Store count goes from 245 to 600, as previously noted – with little help from Kate Spade Saturday.

- Comps slow as the company reaches $2,000 per square foot, which we expect will happen in 5-years time.

- EBIT margins top out at 21% at KSNY, and 18% on a consolidated basis (includes 5% in D&A).

- Interest expense goes away entirely in 3-years as internally generated cash flow outstrips capex needs to build stores.

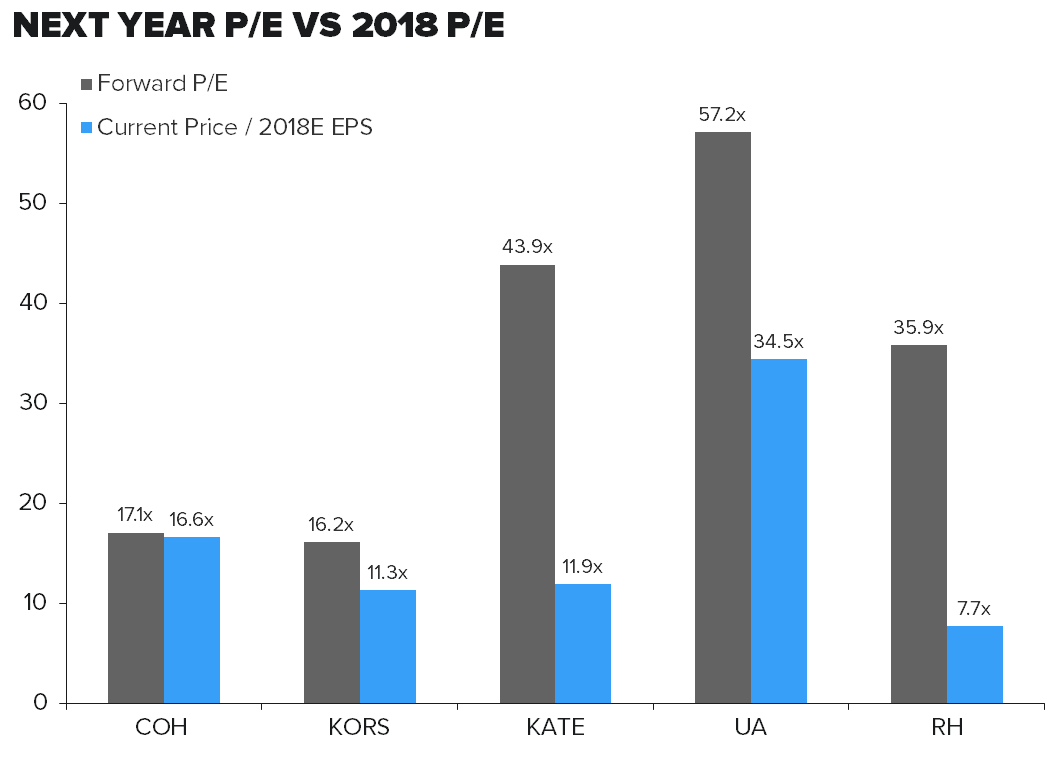

Valuation vs Peers

A quick point on valuation. When we look at earnings today, it’s flat-out expensive. But that’s always been the case. Here are five high-growth (actually 4 high growth + Coach) names where we look at where the stocks are trading on today’s earnings, versus 2018 (if you want to look at 2016, as some people will, the chart looks extremely similar). KATE is expensive today, but right in line with KORS on out-year numbers. The only company that looks meaningfully better is RH.