Investment Recommendations: short Eurozone equities (EZU) and EUR/USD (FXE)

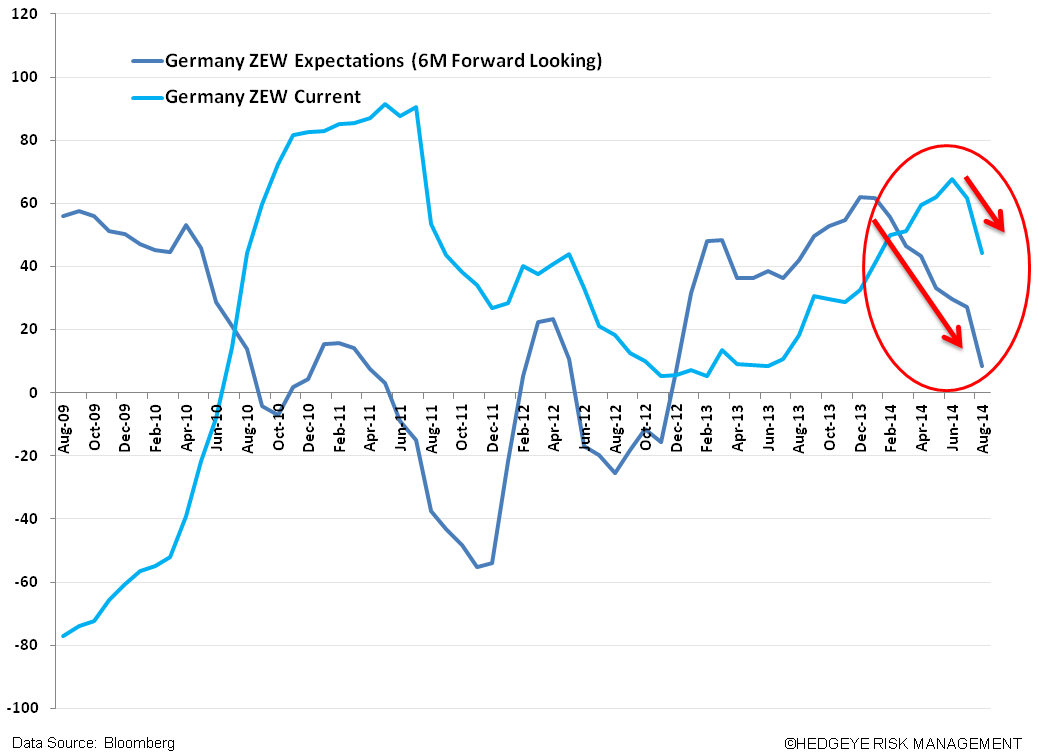

Germany’s Expectations of Economic Growth (as surveyed by ZEW) tanked in today’s release of August data – the 6 month forward looking indicator fell -68% M/M! Similarly, Eurozone Expectations fell -51% M/M. The data further confirms our investment recommendations to be short Eurozone equities (EZU) and EUR/USD (FXE).

- Germany - ZEW Survey Expectations 8.6 AUG (17.0 est.) vs. 27.1 prior

- Germany - ZEW Current Situation 44.3 AUG (54.0 est.) vs. 61.8 prior

- Eurozone - ZEW Survey Expectations 23.7 AUG vs. 48.1 prior

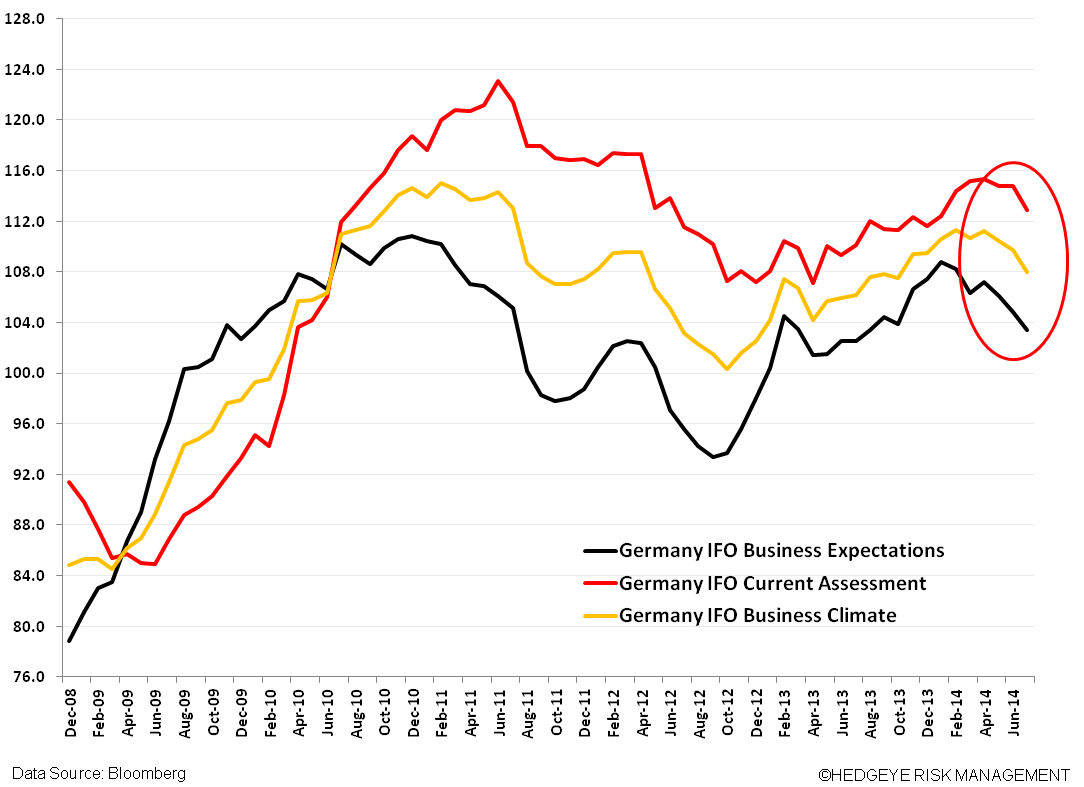

The weakness in the survey mirrors declines/misses in more recent German high frequency data:

- German Factory Orders dropped -3.2% in July M/M (vs expectations of +0.9%) and fell -2.4% Y/Y (vs exp. +1.1%) and +7.7% in June

- German IFO Business Confidence Expectations fell to 103.4 in July versus 104.8 in June

- German Industrial Production rose +0.3% in June M/M (vs exp. +1.2%)

From a quantitative perspective, both the DAX and EUR/USD remain broken across our intermediate term TREND and long term TAIL lines.

We believe our investment recommendations are grounded in a few key points:

- Draghi will be on hold to issue outright QE – in the Fall Draghi may begin issuing QE-lite (ABS buying) to follow on his June announcement of the TLTROs (a new lending program intended to reach the “real” economy). We don’t expect these programs in and of themselves to reverse what’s been slowing economic data and expect the inflation rate will be the big tell – if CPI doesn’t bounce off its current 0.4% Y/Y level, we think market expectations of QE will be put into motion.

- EUR/USD weakness – a more dovish ECB and beginning signs of a quantitative breakout in the US Dollar may continue to drive the cross lower.

- Geopolitical risks clear and present – regionally we expect tensions with Russia over Ukraine and threats of contagion flair-ups (like the financial issues at Banco Espirito Santo) to persist. Further we expect risk premium to remain elevated as conflicts, like the war between Israel and Palestine and US involvement in Iraq, to play into downside risks in equities, globally.

For a more nuanced view of EU regional data and policy dynamics see our note titled Draghi Dangles QE Carrot; On Hold for Now

Matthew Hedrick

Associate