The USD appears to be breaking out while both the EUR/USD and European equities are sending bearish signals. Both of these moves, should they continue, would be a headwind for Gold.

Last week we released an extensive report outlining the implications of a QUAD #4 (inflation and growth decelerating) GIP set-up through Q3. A link to that slide deck is included below:

What's Next For Global Financial Markets?

We are waiting and watching closely for confirmation on this potential inflection point. Our current view that domestic growth is slowing remains intact. Although with commodity disinflation from the first half of the year and recent weakness in Europe, we are watching this re-tracement closely. Recent data has opened up an internal discussion about the strength of our #ConsumerSlowing theme:

- Commodity Disinflation

- Marginally better consumer spending and credit growth combating the absence of a positive trend in real wage growth:

- Household debt growth has increased from Q3 2013

- Trailing 12-month nominal consumer spending slightly outpacing nominal incomes (re-leveraging a potential tailwind to consumer spending capacity)

We highlighted developing credit trends in a note last Friday:

SANGRE VITAL: A QUICK TOUR OF CREDIT TRENDS

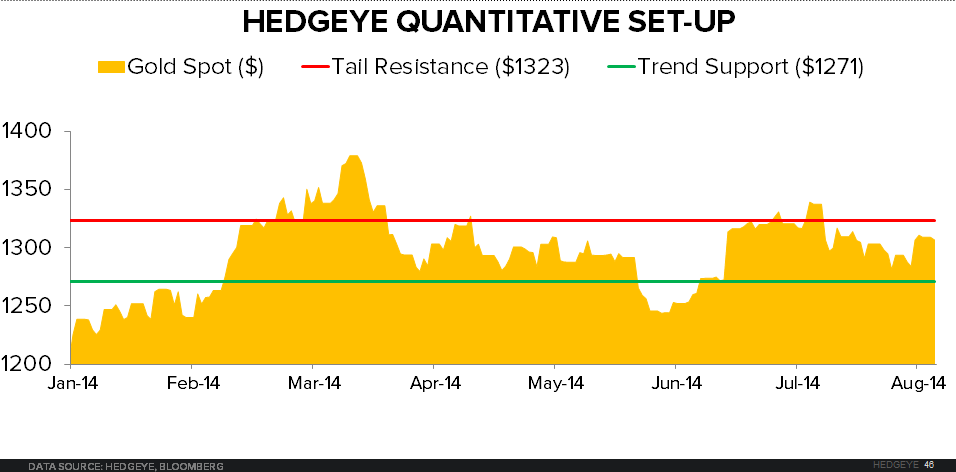

Gold currently stands right in the middle of key @Hedgeye TREND/TAIL levels after trading in a tight range last week (with the exception of a big rally Wednesday front-running Draghi’s speech.) The move suggests the market expected him to announce an asset purchase program. Gold ended the week up over +1%.

@Hedgeye intermediate-term TREND support is at $1271. The long-term TAIL Line of resistance sits at $1323. We would become louder on the long-side if Gold penetrates and holds this TAIL line. The narrative remains the same:

1. Growth expectations slow

2. U.S. interest rates fall

3. Both Gold and Long-term Treasury Bonds rise (holding the monetary policy of other reserve currencies constant over the more intermediate-term a very important factor to our gold thesis that we are watching intently right now).

Ten-year yields touched YTD lows Friday reflecting skepticism around a sustainable recovery despite the +4.1% initial Q2 GDP bounce. After breaking @Hedgeye long-term TAIL support, 1.70% is the next line of defense. The ten-yr yield is down over 20% from the beginning of the year and currently sits near the lows at 2.43% (2.36% YTD low late last week). Our risk management signals suggest the momentum embedded in this trend makes further downside to 1.70% a more probable scenario than the consensus 3%+ expectation.

Although this narrative for the USD outlook works both for and against the price of gold under certain scenarios, we continue to believe real growth expectations in the U.S. for the second half of 2014 remain too high. About a month ago we published a note outlining the thesis on Gold’s interaction with monetary policy by walking through its performance vs. other asset classes under different economic scenarios:

Right now there are two big headwinds to our position that will have implications for Gold’s direction:

- The quantitative signals suggest upside for the dollar and downside for the Euro: An apparent breakout in the dollar to the upside coupled with an incrementally more dovish Draghi is a headwind for Gold. The Euro is at a nine month low currently after topping in March of this year. European data is slowing (magnified in the countries which outperformed in the first half), and a majority of European equity indices are breaking down.

Our recommendation is short:

- EUR/USD

- European Equities (ETF: EZU)

- Weak Europe, Dovish Draghi: The expectation for economic weakness has been somewhat priced-in with expectations that some form of easing from the ECB is right around the corner. The outlook in the U.S. is more uncertain. If growth does miss in the U.S., the fed may get more dovish.. SO MAY THE ECB.

Two comments in particular from Draghi last week caught our attention:

- Readiness to pull the trigger on an asset purchase program.

His tone this past week reflected his willingness to stand ready for an ABS purchase program. In fact, he more or less said that he would implement an asset-backed purchase program (QE without the government bond and public asset purchase program). Not a single economist surveyed by Bloomberg expected a change in interest rates from Draghi last week, but the bounce in Gold suggests the market may have expected some kind of easing out of Draghi Thursday.

- Allusion to divergent policies in the U.K. and U.S. moving forward

The president more or less said the ECB Monetary Policy Committee cannot be outdone with regards to easy-money policy implementation. We interpreted his comments as a confident gesture that the Euro will continue to weaken against the USD and Pound over the intermediate to long-term.

European equity performance ugly last week:

- Greece led the losers (-9.9%)

- Portugal retreated another -6.7% to -17.5% YTD

- The German DAX fell -2.2% to -5.7% YTD

Both the quant signals and our GIP model suggest Europe may slow for the next three consecutive quarters which could potentially warrant a surprisingly more dovish ECB policy. CAN DRAGHI CONVINCE THE MARKET HE’LL BE MORE DOVISH FROM HERE? Unfortunately don’t possess a crystal ball, but the recent weakness is concerning…

We DO believe growth estimates for the full year in the U.S. remain too high, and a more dovish tone will likely be received as bullish for gold on the margin. Please feel free to ping us with any comments or questions.

Ben Ryan

Analyst