Monday (Here) we profiled the special QM related questions included in the Fed’s 3Q14 Senior Loan officer Survey and the negative impact on housing demand.

Yesterday (HERE) we highlighted the G.19 consumer credit data and the continued acceleration in revolving credit growth.

Below we summarily highlight the balance of the 3Q Senior Loan Officer Survey data and a selection of domestic credit metrics.

CREDIT INTUITION: Credit is typically pro-cyclical with banks loosening standards and extending credit in response to rising demand and improved credit risk.

The reason for the pro-cyclicality is rather straightforward - Household capacity for credit increases as incomes rise alongside positive employment growth and as net wealth rises alongside the rise in real and financial assets that typically accompanies an expansionary economic phase.

Cash flows to service debt and the collateral values backing the debt both support incremental capacity for credit and serve to drive an upswing in the credit cycle.

Thus, credit sits as the Sangre Vital of modern macroeconomies in expansion, serving to jumpstart and/or amplify the economic cycle.

Of course, leverage works both ways and amplifies the impacts of a contractionary phase as well.

3Q14 Senior Loan Officer Survey: Rising Demand, Stable-to-Easing Standards

- Demand: Loan demand was broadly higher across C&I, CRE, and Consumer Loan categories.

- Credit Standards: Loan spreads were largely static sequentially while Credit standards were flat-to-down

In short, loan demand continues to rise (particularly across the C&I category), on balance, while credit standards continue to trend favorably alongside that increase in demand and the moderate, ongoing improvement in the labor market.

The Senior Loan Officer Survey data mirror the broader trends in the high frequency H.8 data which currently shows a positive slope of improvement across all major loan categories. Unless the labor data inflects negatively, it’s probable both loan demand and ease of credit access continue to follow their current, pro-cyclical trend.

CREDIT FLOW: The idea of the “Credit Impulse”, popularized by Biggs, Meyer & Pick (2010), centers on the idea that it’s the flow, not the stock, of credit that matters relative to economic growth

The first chart below illustrates the Credit Impulse (Household and Non-Financial Corporate Debt, Flow of Funds data) vs. the Y/Y change in consumer and business demand (represented by the y/y change for the Consumption and Investment components of GDP) along with the Y/Y change in total household and Non-financial corporate debt.

As can be seen, the trend in private sector demand growth tracks the credit impulse closely and leads the positive inflection in y/y debt growth.

The second chart shows the Credit impulse vs. the ‘Banks Willingness to Lend’ measure from the Senior Loan Officer Survey.

Again, the Trend relationship is strong and with Willingness to Lend accelerating in 3Q14 the read through for credit catalyzed private consumption remains favorable

In short, the “credit impulse” tends to lead private demand for credit and “banks willingness to Lend” tends to front-run the credit impulse.

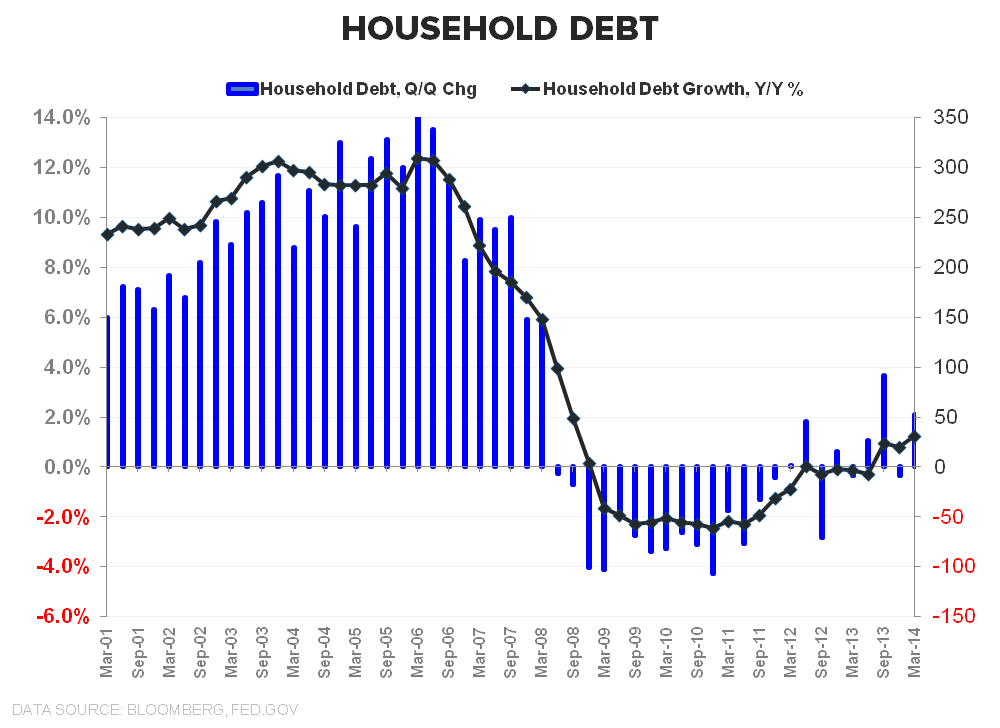

HOUSEHOLD DEBT: After running negative for 18 consecutive quarter beginning in 1Q09, household debt growth returned to positive YoY growth in 3Q13.

Given improving mortgage, auto, and consumer loan trends YTD, credit growth should remain positive thru 2Q/3Q as well when the official Fed data is released. With rates largely static, the closing of the delta between income and debt growth represent the principal upside to credit driven consumption.

The PCE data tells an expectedly similar story. While disposable income grew at a premium to consumption during the acute deleveraging, peri-recession period, that trend has reversed over the TTM with nominal household spending running on par to slightly ahead of nominal aggregate income.

After a 19-quarter, -18.1% decline from peak, Household debt-to-GDP troughed at 77% in 4Q13 and ticked up to 77.4% in 1Q14 alongside the worst post-war, expansionary period GDP print ever.

BIG PICTURE/THE CYCLE: Credit trends are improving and, in a reflexive macroeconomy, can serve to drive incremental spending in the immediate/intermediate term.

Bigger picture, we remain on the wrong end of a credit/interest rate and demographic cycle and haven’t delevered enough to allow debt growth (alongside a rising cost of debt) to run ahead of income growth for any sustainable LT period.

Policy remains a blunt (and now exhausted) tool and exorbitant privilege and dollar hegemony can only defy the gravity of long-term budget constraints for so long.

Christian B. Drake

@HedgeyeUSA