Below are Hedgeye analysts’ latest updates on our nine current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

We also feature three recent institutional research notes that offer valuable insight into the markets and the global economy.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

BOBE: More of the same at Bob Evans Restaurants. The company and activist Sandell Asset Management continue to trade blows through the likes of presentations and letters to shareholders. While both sides have made credible points, we’d argue that Sandell has the upper hand. The reality is, Bob Evans’ Board, as it stands, doesn’t appear open to any of the suggestions Sandell has made to improve shareholder value. It is precisely this stubbornness, and inflexibility, that has led to the current disastrous state of the company.

To be clear, Sandell’s “economic agenda” is not unsustainable, as there are vast operational improvements to be made. In our view, the Board nominees put forth by the activist have more experience in the restaurant industry and are far better equipped to lead a turnaround at the company. For this reason, among others, we’re willing to bet they successfully get majority control of the Board. Bob Evans’ will hold its Annual General Meeting on August 20.

GLD: After a pullback last week, we are sticking with Gold on the long-side. As of now it remains in a bullish @Hedgeye intermediate-term TREND with support at $1271. The long-term TAIL Line remains $1323. You guessed it. The narrative remains the same:

- Growth expectations slow

- US interest rates will fall

- Both Gold and Long-term Treasury Bonds will rise (holding the monetary policy of other reserve currencies constantà a very important factor to our gold thesis that we are watching intently right now).

Ten-year yields touched YTD lows Friday reflecting skepticism around a real recovery despite an initial +4.1% Q2 GDP bounce off the -2.1% Q1 print. After breaking @Hedgeye long-term TAIL support, there is no support for the ten-year yield to 1.70%. Our risk management signals suggest the momentum embedded in this trend makes further downside to 1.70% a more probable scenario than the consensus 3%+ expectation.

Although this narrative for the USD outlook works both for and against the price of gold under certain scenarios, we continue to believe real growth expectations in the U.S. for the second half of 2014 remain too high. Right now there are two big headwinds to our theme regardless of how domestic growth materializes:

- The quant signals suggest upside for the dollar and downside for the Euro (Gold is bought with, and priced in dollars): The @Hedgeye quantitative breakout in the dollar to the upside coupled with an incrementally more dovish Draghi is a headwind for Gold. The Euro is at nine month lows currently after topping in March of this year. Also the USD is breaking out, European data is slowing, and a majority of European equity indices are breaking down.

- Weak Europe, Dovish Draghi: European economic data has slowed. This expectation from the market has been somewhat priced-in with expectations that some form of easing from the ECB is right around the corner. The outlook in the U.S. is more uncertain. If growth does miss in the U.S., the fed may get more dovish but so may the ECB. There were two comments in particular that caught our attention yesterday in Draghi’s address:

- Readiness to pull the trigger on an asset purchase program. Mario Draghi’s tone this week reflected his willingness to stand ready for an ABS purchase program. In fact, he more or less said that he would implement an asset-backed purchase program (QE without the government bond and public asset purchase program). Not a single economist surveyed by Bloomberg expected a change in interest rates from Draghi this week, but the Gold bounce this week suggests the market may have expected some kind of easing out of Draghi Thursday.

- Allusion to divergent policies in the U.K. and U.S. moving forward: by more or less saying the ECB cannot be outdone with regards to implementing easy-money policy. We interpreted his comments as a confident gesture that the Euro will continue to weaken against the USD and Pound over the intermediate to long-term.

HCA: HCA strength continues on the heels of an excellent quarter despite the recent market decline and increase in volatility. HCA is up approximately +5% over the last two weeks versus the S&P 500 which has declined by approximately -3% as we write this note on Friday afternoon. We continue to believe that stock has upside into $71-81 range as 2015 consensus estimates move higher and more in line with our model.

July results of our monthly Physician survey are in, and the results show that maternity trends appear to be in a sustainable recovery. Over the last several months, both deliveries and pregnancies are accelerating among our surveyed physicians. Commercially insured, higher income, as well as Western states show the greatest improvement while low income and the Northeast remain weak. The Current Population Survey (US Census) supports the survey work through data supplied through June with the next update arriving for July by the end of the month.

Improving birth trends is a major tailwind for HCA.

Sustainable Recovery in Birth Trends

HOLX:

Our 3D Tomo Facility Tracker update shows that placements accelerated in July 2014 (35) versus a soft June (22). Prior to seeing the July Tomo Facility count, we were having trouble modelling revenue much above the low end of Hologic’s F4Q14 guidance range of $ million using only data from the 10-Q and from the earnings call. However, if July pace holds throughout the rest of the quarter, it will be a new placement record, providing adequate 3D system revenue to drive total revenue toward the high end of the guidance range, or better.

Hedgeye PAP Survey Results

Our monthly physician survey results indicate a pickup in Patient volume in July after a weak May-June period. There appears to have been a spike among Medicaid practices during 1H14 associated with the rollout of the ACA. At least through July, the upswing has abated somewhat. Commercial volume is running flat after a very weak Q1 and subsequent rebound. As it relates more specifically to HOLX, pap trends continued to improve in July. The forecasted decline PAP volume to reach compliance slowed to a CAGR of -7.5% in July from -10.0% in June.

LM: We have no specific update this week on our long recommendation of Legg Mason stock. That said, the largely institutional fixed income manager is a defensive investment in the current volatile, geopolitical sensitive environment and shares should continue to be more steady than the rest of the asset management sector.

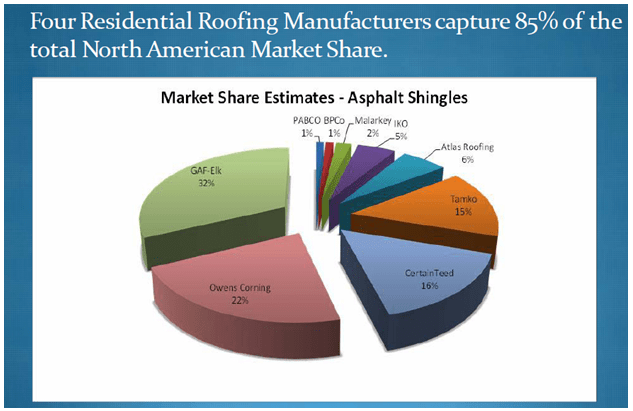

OC: This past Thursday we hosted our expert call with Bill Carlin. Bill spent decades in Owens Corning’s roofing division and now is an industry consultant. The pie chart below is from Bill’s presentation outlining the North American roofing market share by company. Here are a couple of quick takeaways from the call:

- Volumes are hovering around historical lows in part due to lack of storm activity and a weak economic environment.

- Owens Corning has an advantage in controlling its raw material costs. Due to the volatile nature of oil prices, asphalt prices are a significant focus for the roofing industry. Unlike the other competitors, Owens Corning has asphalt plants to buy asphalt volume in advance to help anticipate and control its asphalt costs.

- The industry is intact and has seen the industry leader, GAF/ELK, announce a recent price increase for September. This suggests that a) there is no price war in the industry as the rest of companies will follow and increase prices in response and b) industry margins receive a tailwind from these price increases.

The bottom line is that the roofing industry is cyclically depressed mainly due to volumes versus a dynamic shift in the roofing industry, as we have noted in previous notes. We reiterate the best time to buy cyclicals is when they are depressed and sell when they are high and loved by consensus.

OZM: Och Ziff Capital Management reported in line earnings this week producing $0.18 per share in distributable cash earnings (in line with the Street) and declaring a $0.17 per share dividend (they dividend out over 90% of their distributable cash flow). This distribution alone creates a dividend yield of 4.9% which is partly why we like OZM stock with a much higher yield relative to market averages.

In addition, if Och Ziff ends the year with any performance related gains on the $45.7 billion it manages for clients, 20% of those gains will source another earnings stream which could total up to $0.50 in distributable earnings per share, or another dividend distribution of over 4.0%.

Hence OZM shareholders have the opportunity to collect total annual dividends of up to 9.0% of the current stock price which also has the chance of appreciating with industry leading organic growth rate and very strong performance.

The Barclays Hedge Index is up just 0.60% year-to-date in 2014 versus OZM’s main Multi-Strat fund which is up over 2.0%, displaying the company’s ability to assist investors and shareholders with strong investment management performance.

RH: The prevailing viewpoint with RH is that the company is already in all of the markets it can possibly penetrate, but simply has an opportunity to build larger-format stores. We think that’s wrong. Our analysis suggests that there are 19 new markets in the US and Canada where RH can not only build stores, but build over half of them in the 50,000 square foot range (compared to 9,000 on average today). The bottom line – there’s more square footage growth opportunity here than most people think.

TLT: We added TLT (iShares 20+ Year Treasury Bond ETF) to our high conviction list earlier this week. In conjunction with Hedgeye’s overall #Q3Slowing theme, we think that the slope of domestic economic growth is set to roll over here in the third quarter.

In the context of what might be flat-to-decelerating reported inflation, we think the performance divergences between Treasuries, stocks and commodities may actually be set to widen over the next two to three months.

The view remains counter to consensus expectations, which is additive to our already high conviction in this position.

Click on each title below to unlock the content.

Our Financials team looks at the latest trends in fund flows for both stocks and bonds.

Frothiness in the Semiconductor Sector

Hedgeye Technology sector head Craig Berger dives deep into stocks in the semiconductor sector.

Our Gaming, Lodging and Leisure team tells us why the mass gaming business is pressuring casinos in Macau.