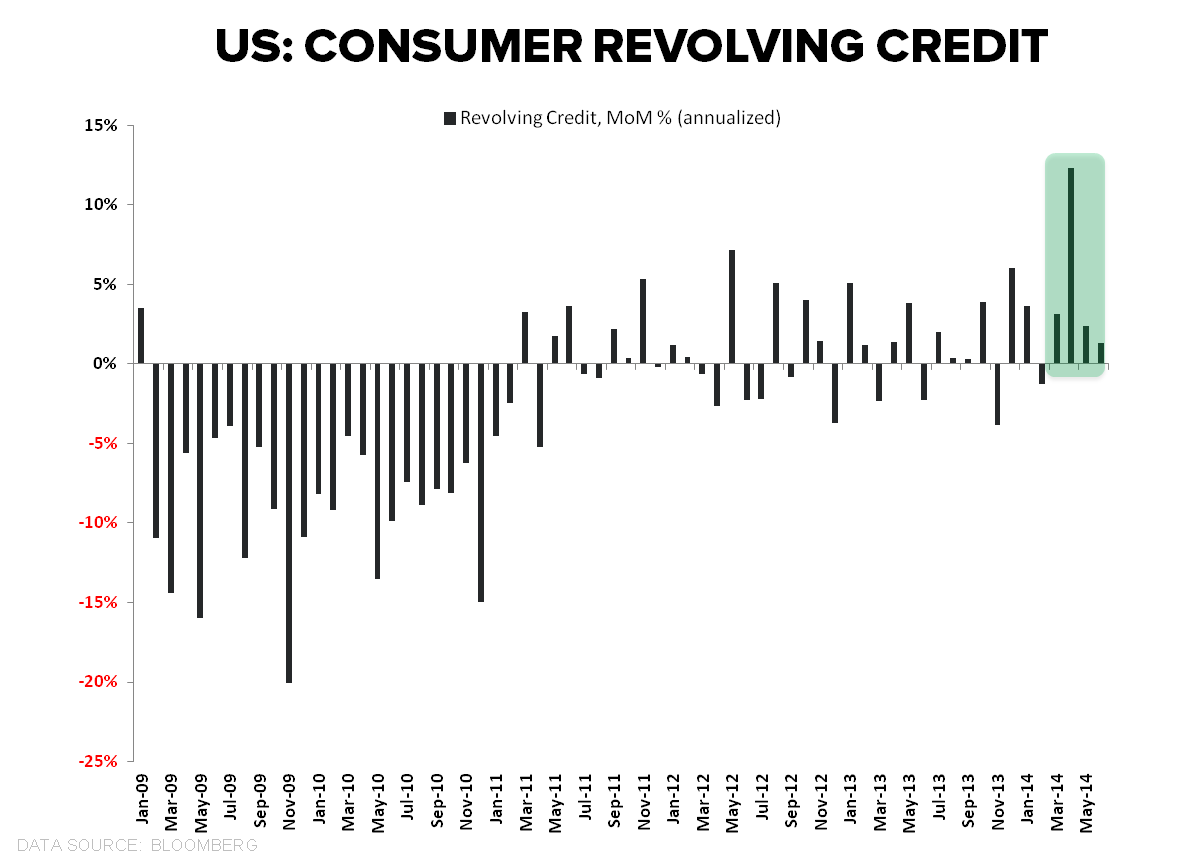

We’ve highlighted the Fed G.19 data the last couple months after the April figures showed the first positive inflection in ~3 yrs as revolving consumer credit balances rose at a month-over-month annualized rate of +12.3%, the fastest rate of growth since 2001.

The May numbers subsequently rose at a +2.1% annualized rate, and the June figures released this afternoon showed a more subdued, but still positive, 1.3% MoM annualized increase in credit card loan growth.

Inclusive of the June data, this is the first 4-month streak of significant, positive MoM loan growth since 2008.

The monthly revolving consumer credit data rhymes with the broader cross-category trends in the weekly Fed H.8 release where the slope of growth across total loans, C&I, CRE, and residential real estate all remain positive.

So, as it stands currently, credit trends continue to improve and aggregate personal & disposable income growth is accelerating as the employment base grows alongside some favorable payroll mix and a return to positive growth in government employment (~17% of the NFP labor force).

Whether the conflation of positive labor and credit market trends, the fledgling breakout in the dollar and the fledgling breakdown in commodity inflation can drive a sustainable, late-cycle acceleration in domestic consumerism in the face of negative real wage growth, a discrete slowdown in housing, and an EU/ROW growth deceleration remains to be seen.

Also, with auto loan growth again a principal driver of the gain in non-revolving consumer credit, the ongoing inflation of the emergent bubble that is subprime auto lending deserves another highlight as something to keep on your radar.

Christian B. Drake

@HedgeyeUSA