Investment Recommendations: short Eurozone equities (EZU) and EUR/USD (FXE)

Key Take-Aways:

- Draghi policy outlook remains dovish and accommodative - QE remains dangled like a carrot

- Hedgeye reiterates our bearish recommendation on European equities (EZU); quantit. broken TRADE and TREND

- Hedgeye’s bearish outlook on the EUR/USD persists; quantit. broken TREND and TAIL

- European fundamental weakness to persist over (at least) intermediate term; geopolitical tensions heightens

I encourage you to review my colleague Darius Dale’s 50 page deck titled What’s Next For Global Financial Markets? for a comprehensive overview of our investment playbook across global asset classes, including a shift in our thinking on a US dollar breakout.

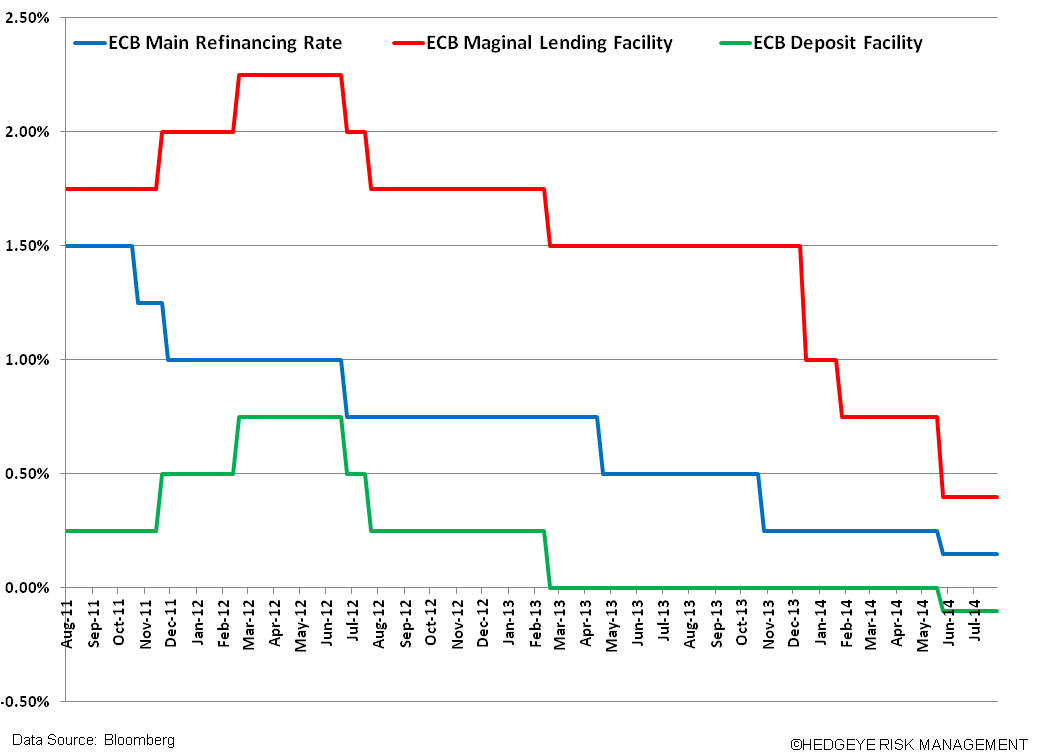

Today’s ECB statement: the bank remains on hold since its big move in its June meeting when it:

- Cut interest rates, and

- Issued the Targeted Longer Term Refinancing Operations (TLTRO), a new lending program intended to reach the “real” economy (see second chart on stalled lending), due to take place in September and December.

New commentary from today’s conference: Draghi offered a bearish outlook on the EUR in suggesting that rates will remain low in the Eurozone for an extended period of time, whereas he sees divergent monetary policies in the US and UK (suggesting US will taper and may hike rates while the UK continues strong Pound policy).

Draghi and staff are conducting preparatory work on buying ABS (the Bank is even hiring a consulting firm to help augment its work). While Draghi didn’t indicate any timing on a potential ABS program, such a program seems inevitable and portends QE-lite (namely without government bond and public asset purchases).

Draghi tried to focus today’s meeting on optimism around the TLTROs boosting lending to the real economy (that he expects will lead to inflation). We have our doubts on the success of the TLTROs (after the failure of the LTROs to reach the economy), however reading the tea leaves of today’s conference call Draghi looks to be buying time for the Bank to figure out how to counter the declining rate of inflation (currently at 0.4%) and muted to weak growth outlook for the region.

With August largely a month of holiday for the ECB (and much of Europe), it’s likely the ECB will not be in a position to act at its next meeting on 9/4, and will opt to monitor the “waters” (data and markets).

That said, risks can come swiftly, and all at once, with recent examples including sanctions against Russia and contagion flair-up risk over financial issues at Banco Espirito Santo.

We’ll be monitoring developments closely, in particular the Eurozone inflation number for August (initial estimate is out on 8/29) – anything below 0.4% should push Draghi’s hand on issuing QE-lite.

European Equities: bearish recommendation on European equities (EZU) remains intact.

Our quantitative lines of support have been broken across European equities for over a month. The move lower has been driven on such factors as slowing fundament data (more below); EU sanction against Russia; and contagion flair-up risks like the financial issues at Banco Espirito Santo.

From here our propriety GIP model (growth, inflation and policy) for assessing economies suggests the Eurozone economy will land in the ugly quad #3 in 2H, representing growth slowing as inflation accelerates.

In 2H we expect inflation to move higher on easier year-over-year comparisons (after remarkable moves Y/Y shown in the chart below) and heightened prospects for QE-lite.

QE-lite Variable on Intermediate term equity view: should weakness in fundamentals and the markets persist, we’d anticipate expectations for QE-lite (ABS) or a more robust QE program to ramp – this could serve to develop a floor in European equities, and with it we’d shift our positioning. As we note in the chart below, the ECB has reduced its balance sheet (down -14% Y/Y and -33% since it topped in AUG 2012), which affords necessary powder to fund any QE program.

EUR/USD short on strength: the EUR/USD is also broken across our intermediate term TREND and long term TAIL lines (at a near 9 month low). Beyond a continuation in dovish policy that we expect from the ECB, we’re signaling a breakout in the US Dollar above its TRADE and TREND levels. For more please see Darius’ deck What’s Next For Global Financial Markets? )

Charts That Matter

Below is a refresh of charts that demonstrate the recent turn lower in data, and are contributing to the drag in European equities.

- DAX – down -9% since on topping July 3rd and -4.5% ytd, and broken across its TREND and TAIL durations. Every major European equity index is down over the last month ranging from the U.K. down -3% to Russia down -17%. Italy’s MIB is -13% since its June top and its recent Q2 GDP print is far from encouraging: -0.2% Q/Q (vs exp. +0.1%) or -0.3% Y/Y (vs exp. +0.1%).

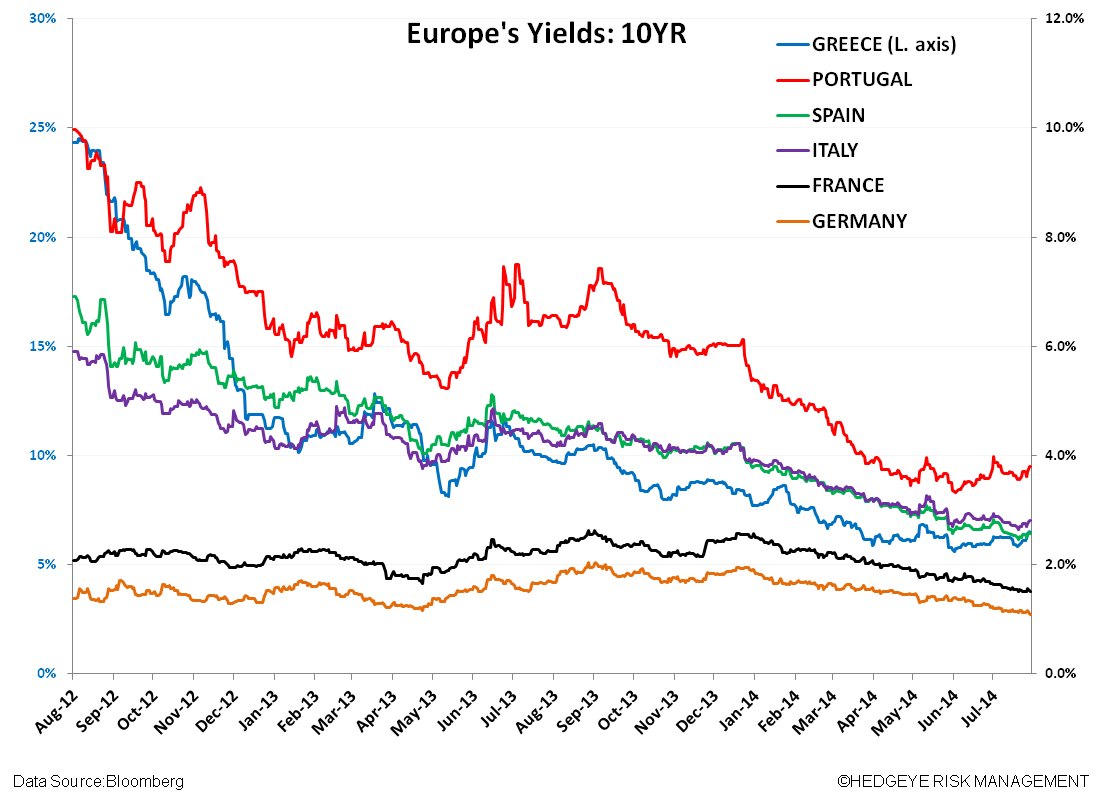

- Sovereign Bond Yields – yields continue to moderate with significant drops on Y/Y comparisons (10YR yields listed below). We expect geopolitical tension like EU sanctions against Russia to encouraging buying in safe haven credit markets like Germany. Of note, this week the 2YR Bund touched down below the 0% bound.

- PMIs – across the major western economies Services got a lift in the most recent print (JUL) M/M, whereas Manufacturing fell off. However the trend clearly suggests a moderation in the improvement seen in the early part of the year. A sideways move of fits and starts is likely over the next months; we expect France to continue to underperform the group.

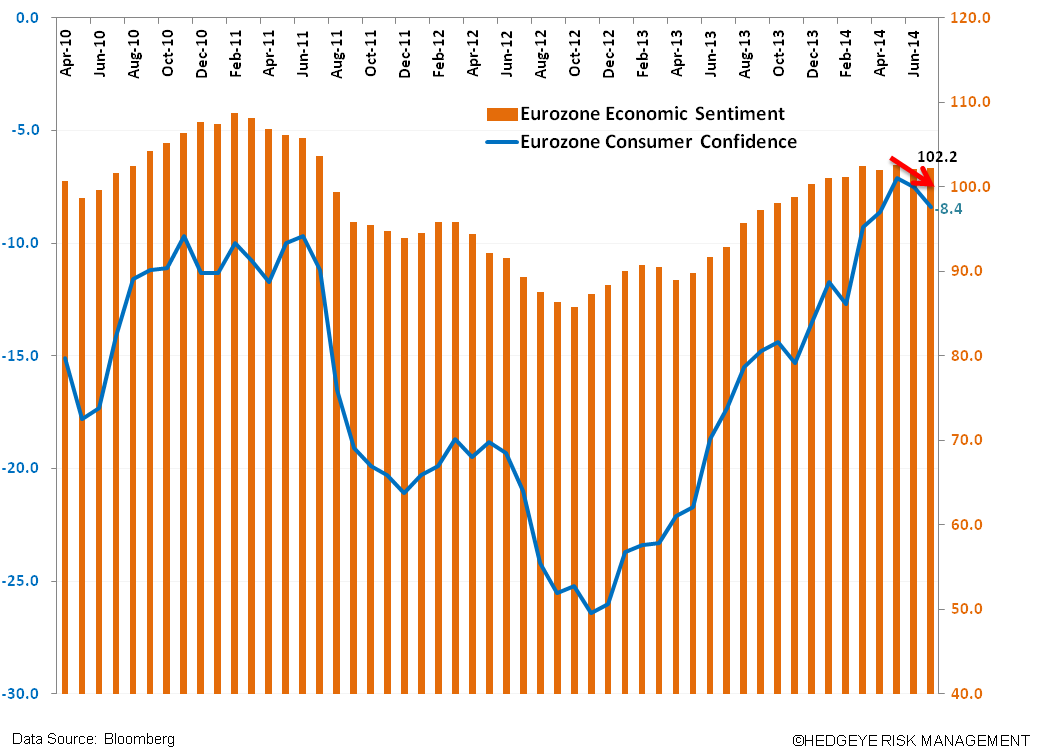

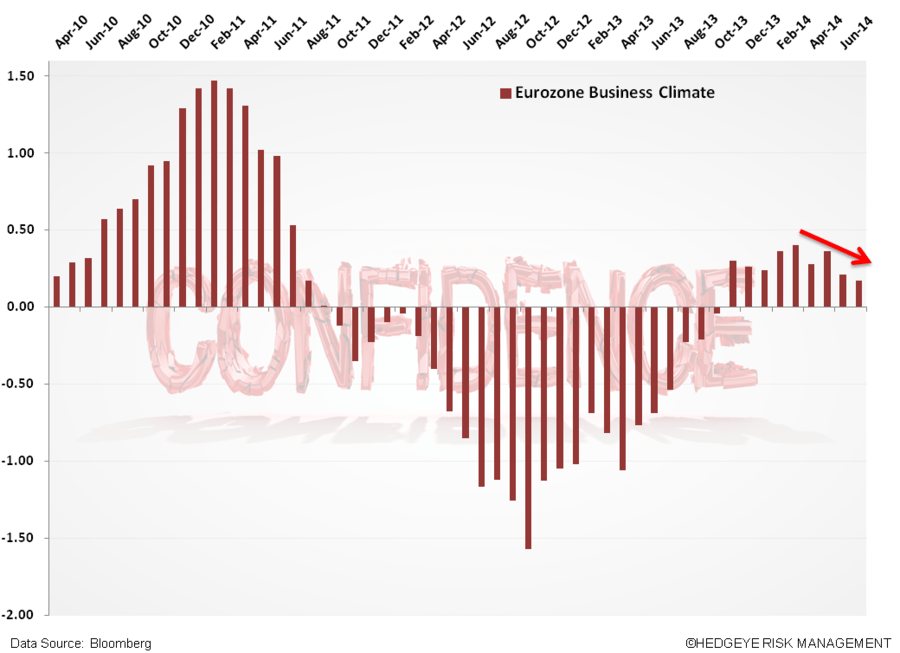

- Eurozone Confidence – follow the red arrows down…

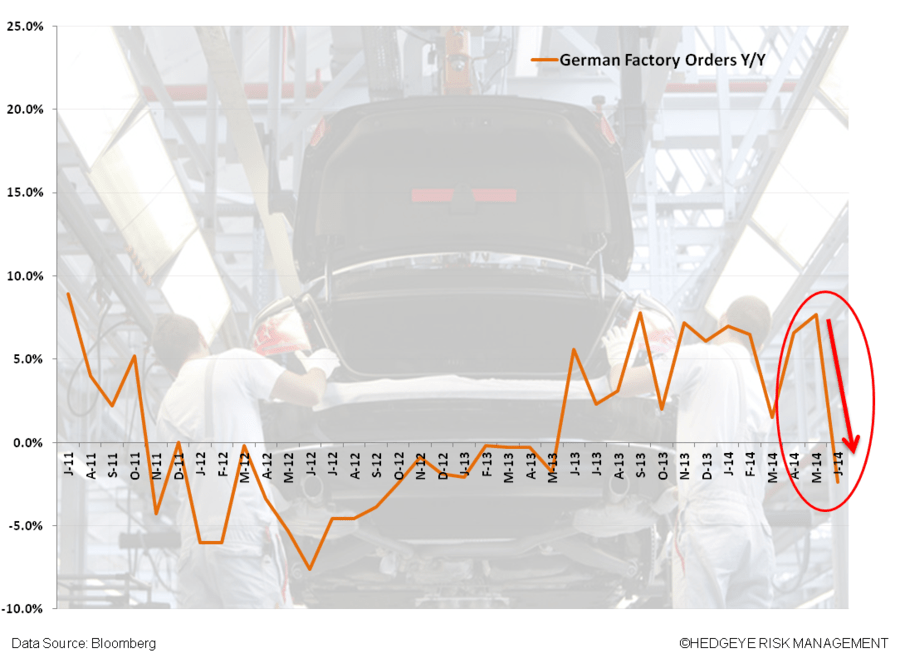

- German Factory Orders – were an unmitigated disaster for June. Consensus expectations for an increase of 0.9% from May and the actual number came in at -3.2%. On a year-over-year basis, the numbers were just as abysmal, down -2.4%. This recent move marks the largest decline since September 2011!

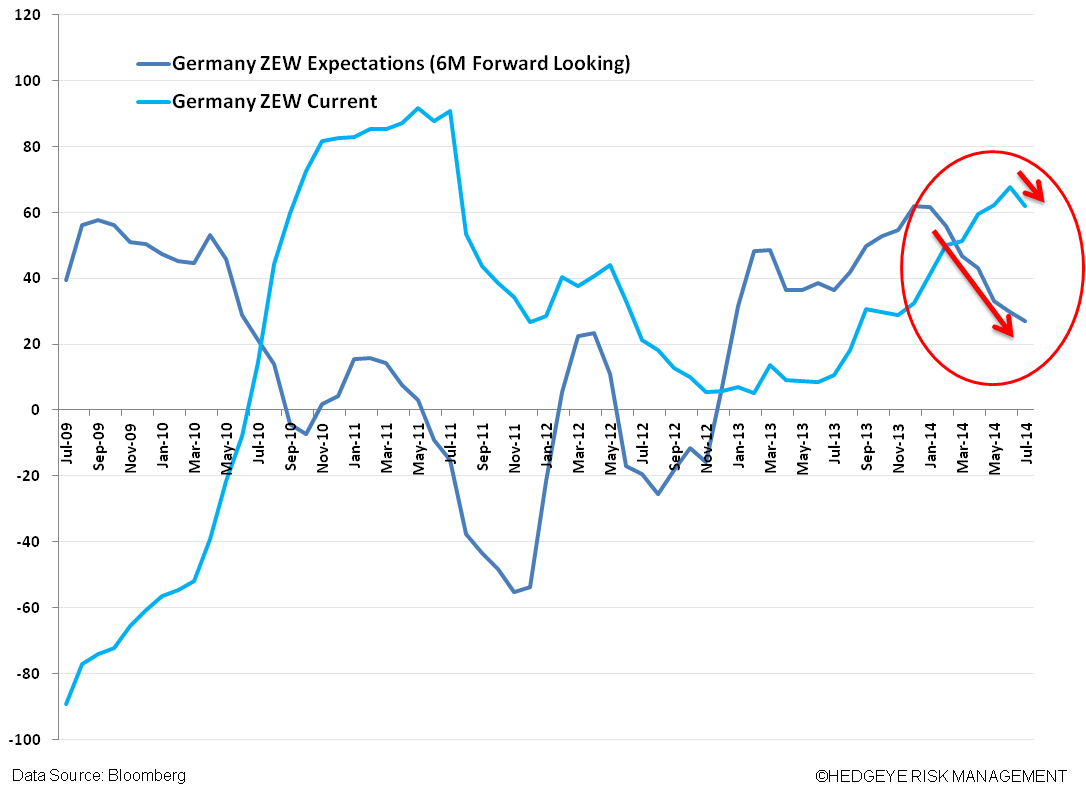

- German Confidence – if Germany is the EU’s economic engine, the more recent turn in these confidence charts are far from encouraging.

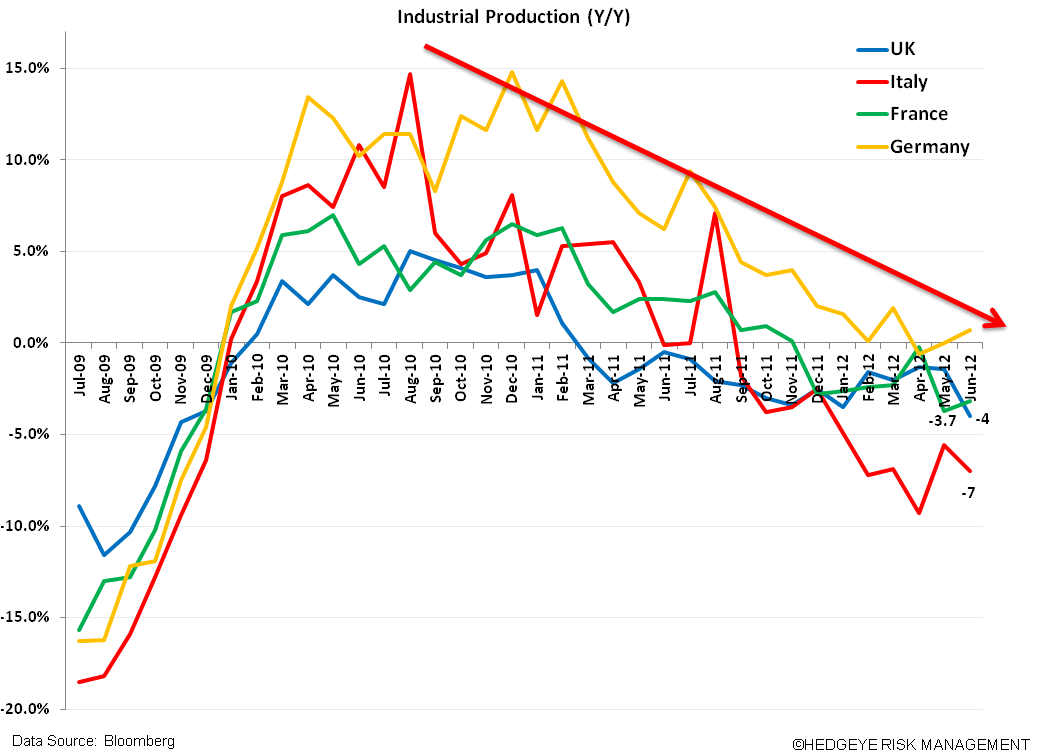

- Industrial Production – an ugly chart, enough said! Today’s print of German Industrial Production was also a disaster: 0.3% JUN M/M (1.2% est.) vs. -1.8% prior (revised -1.7%) or -0.5% JUN Y/Y (0.3% est.) vs. 1.3% prior (1.1% revised)

For those joining Draghi on vacation in August, enjoy!

Matthew Hedrick

Associate