Mass stalled for the 2nd straight month with July Mass segment growth at least 1,000bps below consensus growth estimates. Our Mass Decelerating thesis is occurring faster than we thought.

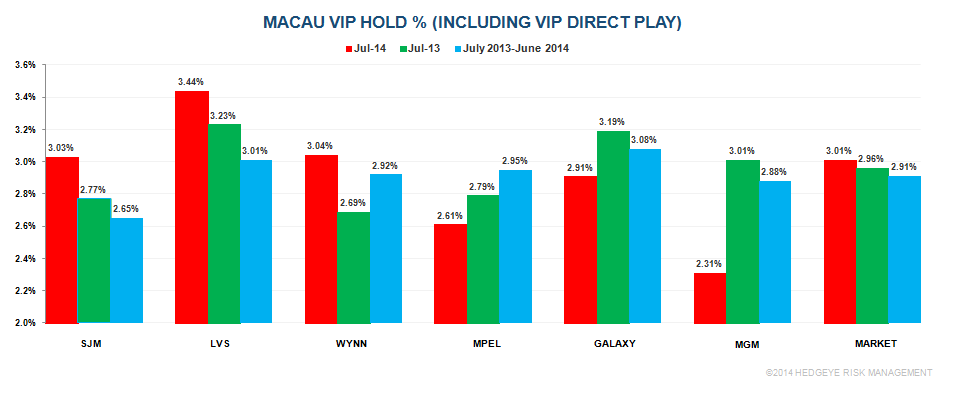

The Street’s bullish thesis of Mass in overdrive has grinded to a halt with the release of the July Macau detail. Mass revenue grew only 17% YoY, well below our projection of +24% and consensus of +30%. The disappointing Mass performance is in line with our Mass Decelerating theme for 2H 2014 but the slowdown is occurring faster than even we thought. As we highlighted in our 06/13/14 note “MACAU: HANDICAPPING MASS DECELERATION”, July 2013 was the month where the concessionaries jacked up the table minimums on most of their Mass tables. Turning to VIP, hold percentage for the market was normal, not low as we had anticipated – so the VIP downturn was entirely volume driven.

Looking ahead to August, we see sequential improvement to flat to low single digit YoY GGR growth. The calendar is actually favorable with one extra Saturday in August 2014 (DICJ reports data with a 1 day lag). For that reason, Mass should look slightly better than July, potentially up high teens to low 20s%.

LVS, WYNN, and Galaxy were the market share winners in July relative to trend

but in the case of LVS, the market share gain was entirely hold driven as the company lost share in both Mass and VIP Rolling Chip. Galaxy remains the only operator we like from a stock perspective. LVS looks vulnerable given our Decelerating Mass theme coupled with the macro issues in Singapore.

Here are some takeaways:

Market:

- Mass revenue grew only 17% YoY, well below expectations, following June’s disappointing 27% gain.

- July’s Mass growth was the lowest since July of 2009

- Adjusting for direct play, VIP hold percentage was normal in both July of 2014 and July 2013

- Rolling Chip (RC) volume fell 13%, the worst performance since March of 2009

LVS:

- What looked like a solid month for the Sands China properties now looks disappointing

- The properties held high on VIP (including Direct) at an estimated 3.44% versus 3.23% last year and average hold of 3.01%

- Despite GGR share in July above recent trend, Mass and RC volume share both fell below recent trend

- GGR actually fell for the 1st time since September 2011

- YoY Mass revenue growth of 15% was the worst performance for LVS since January 2011

- RC volume fell 19% YoY on top of June’s 27% decline

WYNN:

- On a relative basis, Wynn Macau actually had a decent month

- The property gained share relative to recent trend in all segments

- GGR growth of 6% led the market driven by a 36% increase in Mass

- VIP hold percentage was slightly above normal but well above July 2013

MGM:

- MGM’s relative performance was hindered by low VIP hold estimated at 2.31% versus an average of 2.88%

- Market share improved versus recent trend only in RC volume but fell sequentially in VIP and Mass revs

- YoY Mass growth of 40% led the market while the RC volume decline of 9% was 2nd best

MPEL:

- Another disappointing month

- GGR share fell below recent trend driven by RC volume and lower relative hold %

- Hold percentage was an estimated 2.61% versus average hold of 2.95%

- Mass revenue grew in line with the market at 17% but RC volume fell 21%

Galaxy Entertainment:

- On a relative basis, July was a strong month for the Galaxy properties

- GGR share was slightly above trend but Mass share grew sequentially and so did RC share

- GGR was flat YoY but held back by a low VIP hold percentage

- Mass growth was in line with the market but Galaxy was the only company to post YoY growth in Rolling Chip volume