Conclusion: Here’s a detailed financial look at athlete endorsement trends between Nike and UnderArmour. These are long-term trends that don’t serve as a smoking gun for a given quarter. That said, it is fascinating to see how the portfolio of sponsorship deals is both growing and maturing at an accelerating rate. Furthermore, we can see the costs that are coming down the pike. For example, next year NKE is looking at an incremental $82mm (or $991mm in total) in endorsements. To justify that without being margin-dilutive, NKE needs to generate an extra $585mm in revenue. That’s 2.1% growth, which it can pretty much do in its sleep. UA, on the other hand, is looking at a 39% jump in minimum sponsorship payments to $81mm, its biggest jump ever. UA can cover that with a 9% incremental sales boost, or $210mm – not a problem for UA. But keep in mind that this past year it only needed $45mm to cover a measly $5mm incremental bump in endorsements. If there’s any real takeaway here it’s that as UA grows and succeeds in its own right, it is competing increasingly against the big boys (NKE, Adidas, Reebok, Puma) for marketable talent. It has a great advantage in that the brand is so hot, authentic and relevant. But those factors do not trump the economics associated with a higher ante-chip for sponsorship deals. We can see what’s coming on the cost side, now we just need the revenue to follow. It’ll probably come. But anyone looking for margins to go up might be in for a surprise. The revenue growth did not matter as much over the past year – but now it matters materially, especially with the stock trading at 70x+ earnings.

DETAILS

When people think of the biggest costs associated with competing in the athletic footwear and apparel business, they usually talk about raw materials, labor, distribution and physical infrastructure. All those things matter. But one of the biggest costs is athlete endorsements. This line item is so big, in fact, that the companies are required to file all minimum required payments in almost exactly the same way that retailers are obligated to outline future minimum lease payments under operating lease agreements.

We think that the comparisons are particularly interesting between NKE and UA. Obviously, there is a huge difference in aggregate sponsorship amounts, but in looking through the numbers we can pull away some interesting trends as to how each company’s portfolio is structured and evolving. Here are some key takeaways:

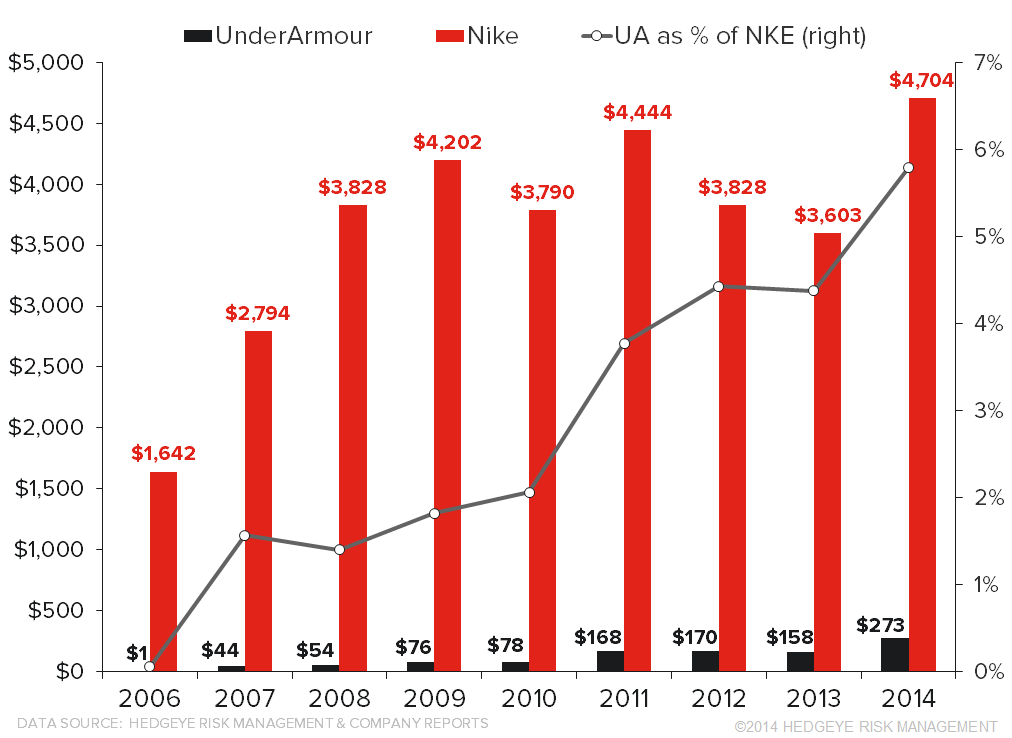

1. Gap is Huge, But Closing: Nike has $4.7bn in forward obligations to pay its athletes and teams, while UnderArmour is sitting at $273mm. That’s a huge difference, but keep in mind that UA was only 2% as large as Nike four years ago, and is 6% today. That far outpaced UA’s revenue growth.

2. Both Follow The Same Trend. We’d go to the mat with anyone who claims that UA and NKE don’t compete against one another for talent (yes, many people make this case to us). The reality is that when we chart sponsorship obligations over time as a percent of sales, the trends are unmistakable for these two companies. Nike operates on a higher (more expensive) plane than UA. But in each of the past seven years, they have moved in exactly the same direction. Nike’s not worried about this. UA probably should be at some level.

3. As a % of Demand Creation Spend, UA has become Nike. This chart is fascinating to us, as it shows how sponsorships went from 15% UA’s Demand Creation budget in its earlier years, and has more than doubled to a level that sits just higher than Nike. This is neither good nor bad. It simply tells us that sponsorships and endorsements are a key part of the UA model. Unfortunately, we’d point out that Nike has 4x more sponsorship obligations globally today ($4.7bn) than UnderArmour has generated in Operating Profit since the brand’s inception in 1996. UA is going to have to get more active with some bigger name athletes, and Nike won’t be too keen to lose that battle.

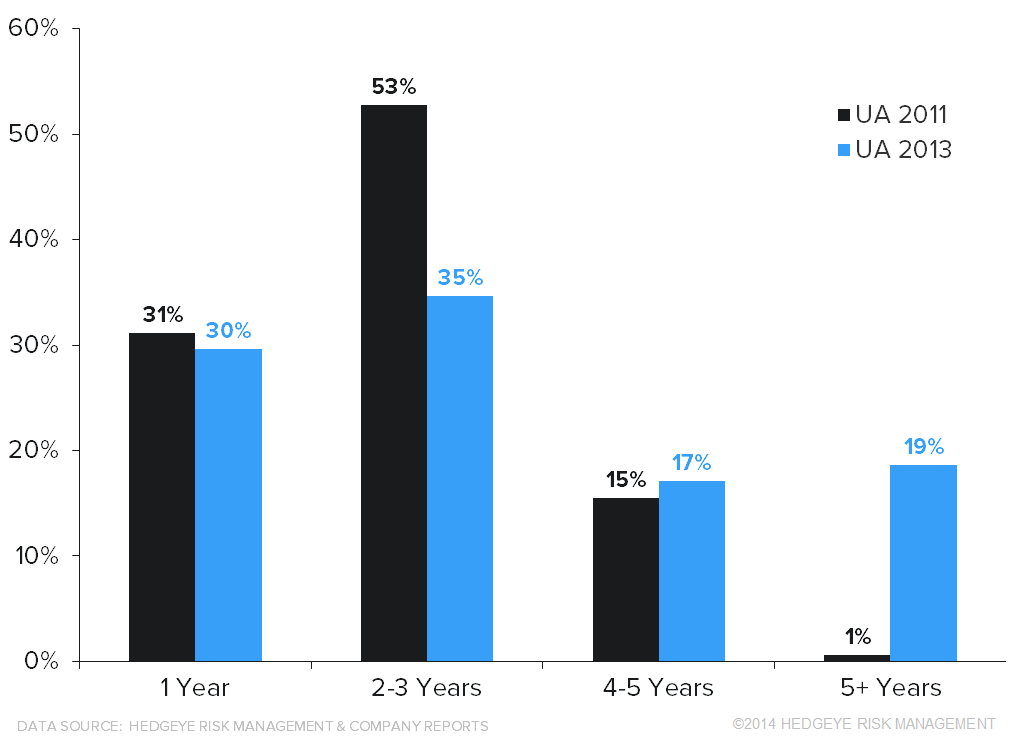

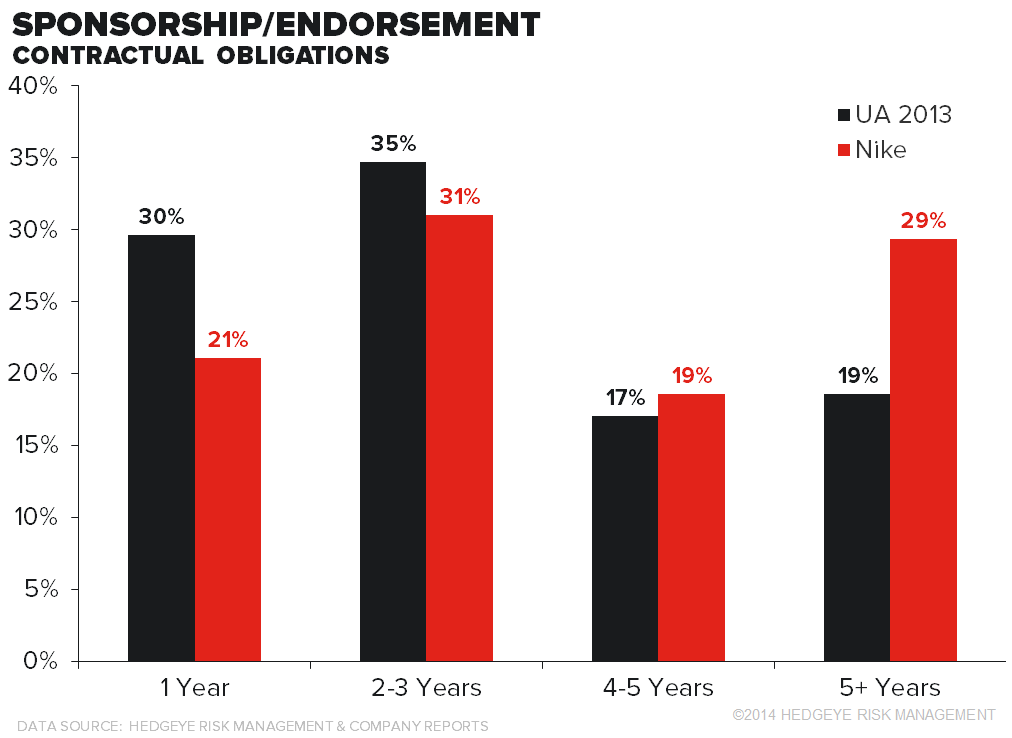

4. Obligation Weighting: UnderArmour generally has an endorsement portfolio with obligations that are more near-term weighted. Today, about 65% of its obligations are due by the end of 2016. Again, that’s neither good nor bad…it’s simply UA’s strategy. Nike is more back-end loaded with almost a third of its deals due after 5-years. This is due to Nike’s long-term deals with the leagues like the NFL and national teams like Brazil. It’s in the process of exiting its 10-year deal with Manchester United, which saves it about $38mm annually.

5. In looking at UA more closely, there’s actually been a fairly dramatic change in its sponsorship duration composition over the past two years alone. UA went from having 84% of deals due within 3-years and only 1% after 5-years, to having 19% due after year 5. This shows that UA is playing in the big leagues - competing for higher profile athletes and teams.