BNNY remains on the Hedgeye Best Ideas list as a Short.

Annie’s is reporting 1QF15 earnings on August 7th AMC.

Trading at 33x P/E (NTM), BNNY continues to be overvalued and is likely to contract further as we believe the company will disappoint on Thursday and guide lower for the remainder of the fiscal year.

Over the long run, the Annie’s brand and continued growth of organics should power above average sales growth, but earnings will remain elusive. Importantly, BNNY will not generate any operating profit this quarter. The competitive pressures in the organic space, specifically in the Mac ‘N’ Cheese segment, will not abate anytime soon.

Earnings estimates have moved slightly lower during the quarter, as the organic segment continues to see slower trends. Depending on how well the company is able to manage SG&A, we believe earnings will come in around ($0.05) for the quarter. This is $0.02 below consensus, but it wouldn’t surprise us if the company is able to manage expenses to limit the damage in the quarter.

Our model generates lower sales than the Street, as well as lower gross margins and SG&A margins. We’re expecting sales growth of +3% in the Meals segment, which would imply a slowdown from recent trends in the category, reflecting the recent deceleration in consumption and the UNFI deloading.

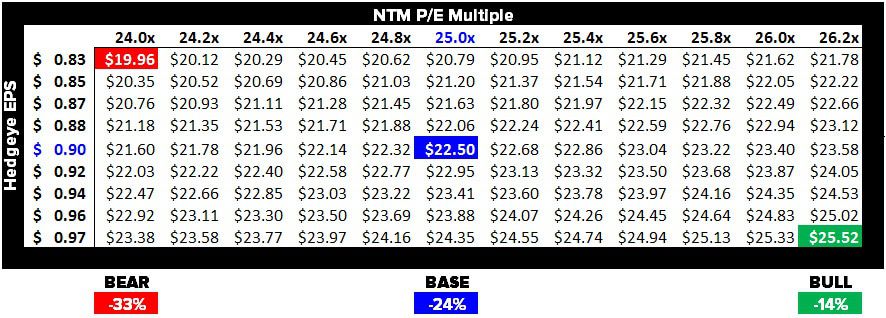

Following the release, we expect the FY15 consensus EPS estimate of $0.90 to be revised lower by $0.10-0.20.

The risk to staying short is an outright sale of the company, but we don’t see this happening any time soon!

The table below outlines our risk/reward profile for the company.

Howard Penney

Managing Director

Matt Hedrick

Associate

Fred Masotta

Analyst